As Fed Tightens, Investors Give Up Crisis-Era Rate Protection

As Fed Tightens, Investors Give Up Crisis-Era Rate Protection

(Bloomberg) -- U.S. corporate lenders are giving up safeguards that protect them from short-term interest rates falling close to zero, a step that could haunt them when the economy sours.

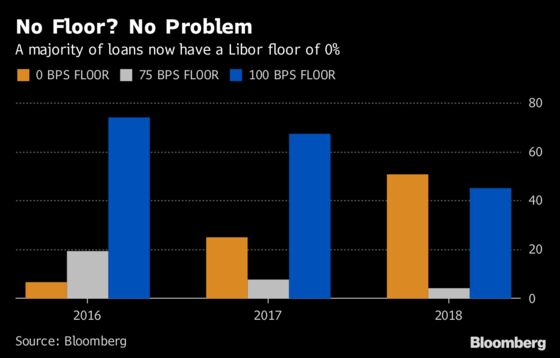

Almost 70 percent of loans to junk-rated companies made in the second quarter were missing a key protection known as a Libor floor, according to data compiled by Bloomberg. The provision is designed to ensure that investors don’t lose too much of their interest income when Libor falls below a pre-defined level, often 1 percent. In the first quarter, around 58 percent of leveraged loans didn’t have that safeguard, while two years earlier, just about all had it.

Investors’ willingness to forego Libor floors in the more than $1 trillion market for leveraged loans underscores how little they fear an economic downturn that brings rates close to zero again, as three-month Libor hovers around 2.35 percent. Other parts of the credit markets reflect similar exuberance: the best performing U.S. corporate bonds this year, for example, are the lowest rated. Lenders are broadly willing to give up protections designed to shield them in downturns.

“It’s another straw on the camel’s back,” said Andy Hunt, co-head of global fixed income and head of liability-driven investing and global credit at Wells Fargo Asset Management, regarding the disappearance of Libor floors. “It’s not that any one of these things is catastrophic, but put it together, you add it up to be a package of more borrower-friendly than investor-friendly characteristics." The firm managed around $500 billion as of June 30.

The bigger concern for most investors now is the Federal Reserve’s plan to continue hiking rates, which tends to translate to higher Libor rates as well. But money managers shouldn’t forget how quickly rates can turn, said Danielle DiMartino Booth, a former adviser to the Federal Reserve Bank of Dallas who founded a research firm and writes for Bloomberg Opinion. The yield curve is flattening and may end up inverting, which typically signals an economic downturn is coming. When the yield curve inverted in February 2000, recession hit just 13 months later. That’s a huge challenge for Fed Chairman Jerome Powell, DiMartino Booth said.

“Investors are in complete and total denial that Powell is going to magically, masterfully raise rates beyond the point of inversion and not disturb the economy at all,” she said. “Chances are growing by the month that the Fed will be lowering rates before they know it.”

Crisis Era

Libor floors became common in the leveraged loan market after rates dropped to near zero in the wake of the financial crisis, pulling down interest payments on floating-rate instruments. A floor sets a minimum level for the benchmark used for interest-rate payments. An investor usually receives a margin on top of the benchmark.

The Fed plans to continue hiking rates, which has helped fuel investor demand for floating-rate debt like leveraged loans. There are now about as many leveraged loans outstanding as there are junk bonds.

Not every investor is alarmed. The average life a loan is only three years, so money managers aren’t likely to need floors again soon, said Gene Tannuzzo, a money manager at Columbia Threadneedle Investments. And Libor is set to be abandoned by the end of 2021, in favor of new benchmarks.

“Why put in a floor if you don’t need to? There are so many buyers right now, you don’t need to do anything to get them,” he said. “Libor floors, at this point in time, you could argue are irrelevant.”

‘Unprecedented Risk’

Libor floors are just one of many protections that lenders have been willing to ease up on in recent years. A measure of loan covenant quality finished 2017 at its weakest level on record, suggesting lenders face “unprecedented risk” from their lack of safeguards, Moody’s Investors Service wrote in a report in April.

After seven rate hikes, Powell is giving some hints that the Fed may start to slow the pace of its tightening, as when this week he added the words "for now" to his description of the central bank’s plan to continue lifting rates. And while the Fed hikes gradually, it tends to cut rates quickly, as when it slashed rates from 4.75 percent in September 2007 to around zero in December 2008. Money managers should be reluctant to give up protections against falling rates, said DiMartino Booth.

“Investors need to wake up and demand their floors,” she said.

--With assistance from Sally Bakewell, Lara Wieczezynski, Lisa Lee and Natasha Rausch.

To contact the reporter on this story: Molly Smith in New York at msmith604@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Dan Wilchins

©2018 Bloomberg L.P.