Hate ETFs? Quants Say They Found Anomaly to Profit on Their Flows

Hate ETFs? Quants Say They Found Anomaly to Profit on Their Flows

(Bloomberg) -- Stock managers sick of being steamrolled by the onslaught of passive funds may have a new weapon to wield, one that was born of the very success their enemies had in overrunning the market.

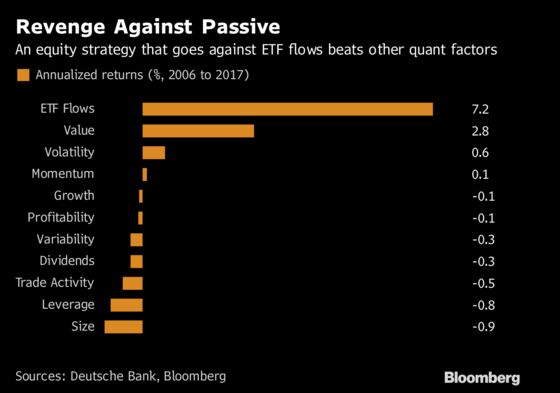

According to quant strategists at Deutsche Bank, investors can beat equity benchmarks by building portfolios out of stocks that get whipped around the most when exchange-traded funds rebalance.

Bet against the ones they buy, and buy the ones they sell, is what they recommend. If all you did was go long stocks with the most negative ETF flows over the last 12 years, you would’ve topped the Russell 3000 Index by 2 percentage points annually. Buying and shorting returned 7.2 percent a year, the firms says. That’s more than double the best-performer among 10 factors tracked by Bloomberg over the period.

So enamored are they with their findings that Deutsche Bank strategists led by Ronnie Shah are treating it as the discovery of a new investment anomaly, a systematic way of profiting from errors in investor thinking.

In this case, they say, the error is when traders sense price trends being created by ETF flows, jump in and make them bigger. Since buying and selling by ETFs doesn’t reflect any company-specific knowledge, the trends later reverse, the study holds.

“The proliferation of passive investments is causing distortions,” said Shah, the firm’s head of U.S. quantitative equity strategy. “It’s a new anomaly associated with ETF flows that active managers can take advantage of.”

His team is among a growing group of market watchers who seek an edge by studying ETF behavior at a time when indexes outnumber stocks and passive vehicles control more than one fifth of the market cap of the S&P 500 and Russell 2000 indexes.

While hedge funds and other speculators have devised any number of strategies to front-run and otherwise exploit passive flows, Shah is among the first to publish a model for doing so over time using rule-based inputs. The success of the strategy relies on the popularity of passive investing, he said.

Lots of trading systems generate big returns on paper and then fail to live up to their promise when let loose in the real world. Shah noted that his model didn’t turn a profit until 2009, when the active-to-passive rotation accelerated. That’s also when the bull market began, leading one analyst to question if it’s a coincidence.

“Seeing anything turn around in 2009, you have to wonder whether it’s just a good, up market strategy,” said Melissa Brown, head of applied research at Axioma Inc., a provider of tools for risk management and portfolio construction.

Returns such as those reported in the study reflect choices about time frames and trading rules that in any researcher’s hands could be tweaked to maximize output, noted Vincent Deluard, a strategist with INTL FCStone Financial. But Shah’s study looks like “a great paper” with little evidence of data snooping, he said.

“The fact that the results are not that amazing actually increases my confidence in their findings, it suggests little over-optimization,” Deluard said. “From what I can tell without replicating the work myself, it looks like they were quite diligent.”

A separate paper published this month by S&P Global’s market intelligence unit found evidence that stocks responded to price pressures created by ETF flows, mainly those created by buying and selling of ETFs in the open market. The effect “is transient and of only modest magnitude," though might also enhance returns if included in a risk model, it said.

Unlike active funds where managers spend months researching fundamentals in the quest to pick winners, an ETF typically tracks an index and only buys and sells when the members change. Rebalancings, which happen on a regular basis, can trigger money flows with only the thinnest connection to a company’s fundamentals.

The source of inflows isn’t always intuitive. Often a stock’s demotion from a large-cap index can spur passive buying. It takes a bigger share of the small-cap pool than its old weight in large caps, and the downgrade forces ETFs to purchase it.

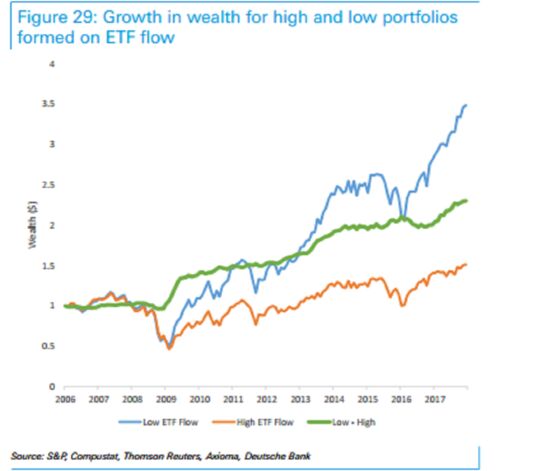

Such blind buying tends to push share prices beyond what’s justified by fundamentals, Deutsche Bank says. But the gains and losses later unwind. To exploit the pattern, the firm developed a quantitative model that tracks ETF flows for Russell 3000 companies, and each month it ranks stocks by their performance over the previous 12 months.

Signals from ETF flows have shown low correlation with traditional quantitative factors such as momentum or value, making them “an enhancement” to existing models, according to Deutsche Bank.

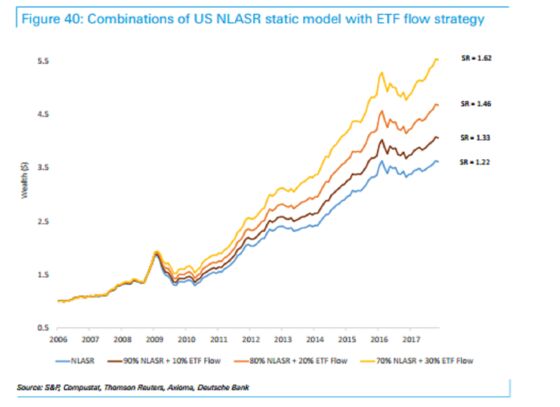

Keeping other factors static in a multi-factor model, the strategists found that incorporating ETF flows led to proportionate improvement in performance. The more ETF flows are considered, the better the returns.

“Whether or not it’s a factor is debatable,” Shah said. “But this is an anomaly that we found and it’s worth exploring further.”

To contact the reporter on this story: Lu Wang in New York at lwang8@bloomberg.net

To contact the editors responsible for this story: Courtney Dentch at cdentch1@bloomberg.net, Chris Nagi, Eric J. Weiner

©2018 Bloomberg L.P.