VIX Futures Close at Lowest Level in Six Months as Fear Vanishes

VIX Futures Close at Lowest Level in Six Months as Fear Vanishes

(Bloomberg) -- After a storm comes the calm...eventually.

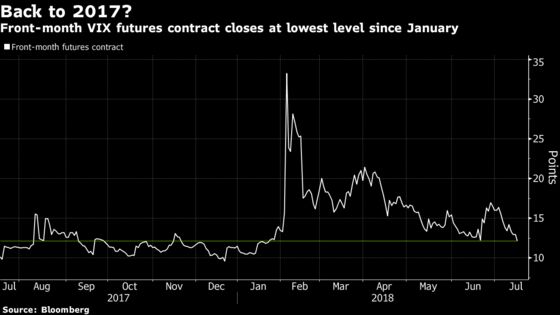

Front-month VIX futures closed at 12.12 on Tuesday, their lowest finish since before the record explosion in volatility in February, which roiled markets and wiped out several exchange-traded products that let investors bet on market tranquility.

VIX futures contracts are tied to the Cboe Volatility Index, a gauge of the one-month implied swings for the S&P 500 Index that’s often called the VIX or Wall Street’s “fear gauge.”

Traders’ renewed faith that U.S. stocks won’t stumble in the near term is buoyed by the start of earnings season. This is a period in which equities usually do well and the implied and realized correlation among members of the benchmark U.S. equity gauge declines, with stocks moving for more company-specific reasons. That helps dampen volatility at the index level.

The spread between August and September VIX futures contracts -- which will become the front and second-month contracts after the July contract expires on Wednesday morning -- currently sits at around 0.8 in early trading. Should this hold, the contango (that is, upward slope) at the front portion of the VIX futures curve would be steeper than it has been on average over the past year.

This curve structure serves as a tailwind to those shorting long-volatility exchange-traded products. Those ETPs typically shift their exposure to the (generally pricier) second-month contract as time passes, which tends to converge downwards to its front-month counterpart. The “rolldown” dynamic benefits volatility sellers, giving them a reason to maintain short positions even when the level of spot VIX and the front-month futures contract seem like they can’t sink lower.

“It’s safer to be short a steep board with a sleepy market than it is with spot higher and a flatter board,” said Dave Roberts, an independent trader of volatility products and associated derivatives based in Washington, D.C.

In early February, the spread between the front and second-month contract had whittled away to nearly nothing before turning into negative steep territory amid market angst, exacerbated by a messy unwind of the short-volatility trade.

For now, however, the VIX curve is cool, calm, and in contango.

To contact the reporter on this story: Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Randall Jensen, Dave Liedtka

©2018 Bloomberg L.P.