Barclays Leads European Banks' Pursuit of Risky U.S. Debt

Deutsche Bank, which is giving up much of its Wall Street ambition, is also joining the race with more capital.

(Bloomberg) -- When an indebted infant health-care company in Atlanta wanted to borrow hundreds of millions of dollars to buy a rival in Pasadena, it turned to a lender thousands of miles away in London.

Barclays Plc is helping Aveanna Healthcare LLC get a $221 million loan for its purchase of Premier Healthcare Services LLC, adding to a $900 million debt last year. The deal will push Aveanna’s borrowings to more than 10 times its earnings and leave it with “little room for error,” S&P Global Ratings said.

The proposed loan is among tens of billions of dollars of borrowings that European lenders are arranging for riskier American clients, a business they’re targeting to ease the pain from revenue slumps in other areas. They’re so keen to take market share from their U.S. rivals that even Deutsche Bank AG, the embattled lender that’s giving up much of its Wall Street ambition, has earmarked more funds for such deals.

Now some observers warn that they’re pushing into a borrowing binge that’s spooked some of the world’s biggest money managers and been described by the Bank of England as a risk to financial stability. Increased competition may be enabling companies to borrow more than they should and on increasingly loose terms, say investors and even some inside the banks.

“This gain in market share appears to result from European banks’ willingness to stretch even further on leverage levels, structure and pricing,” said Michael Barnes, co-chief investment officer at Tricadia Capital Management LLC in New York. “As is typical of all credit cycles, it is a race to the bottom.”

Borrowing Spree

The Aveanna deal is a snapshot of the surging U.S. market for leveraged loans, which lenders arrange for highly indebted corporations -- often to fund acquisitions, or allow dividend payments to the private equity investors that own many of them. Banks and other firms structured $494 billion of new debts last year, the most since at least 2011 and roughly the equivalent of the gross domestic product of Poland. After a strong first half, they are on track to create even more in 2018, data compiled by Bloomberg show.

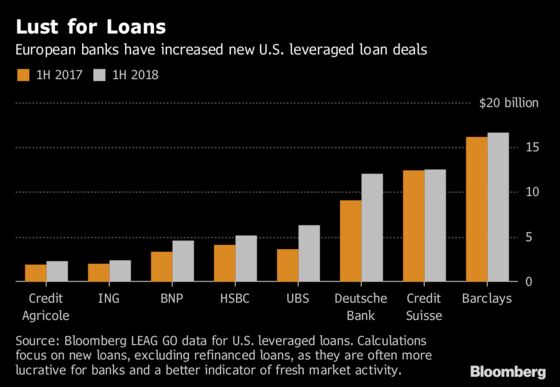

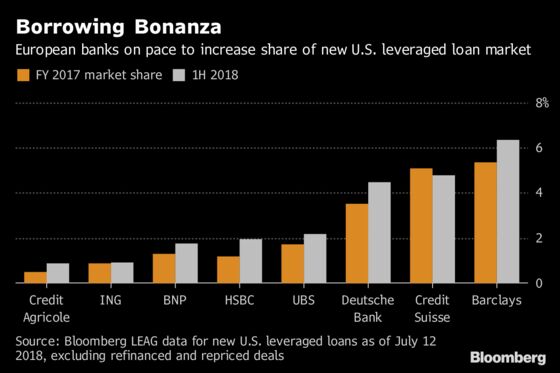

Europe’s biggest lenders are trying to cash in on the borrowing spree. Eight banks from the continent arranged some $62 billion of new U.S. leveraged loans in the first half of this year, compared with $53 billion a year earlier, increasing their combined market share to almost 24 percent, according to data compiled by Bloomberg. The figures include revolving lines of credit that are often part of such deals, and exclude refinancings of old loans.

The Europeans are led by Barclays, where Chief Executive Officer Jes Staley has targeted leveraged finance as an area for growth since taking charge in 2015. The U.K. bank, which bought the U.S. operations of Lehman Brothers Holdings Inc. after its collapse, has more than 6 percent of the market for new loans and is on track to be the third-biggest arranger this year. That would be its highest ranking since 2014, the data show.

“Barclays operates in compliance with the rigorous leverage finance guidance provided by the regulators,” said Jon Laycock, a spokesman for the lender. “In addition, we have a thorough internal credit risk process and we always ensure that we allocate our balance sheet to drive the best outcomes for both our clients and our shareholders.”

Credit Suisse Group AG, Barclays’ biggest European rival in the U.S. so far this year, has increased hiring in leveraged finance as it wagers that the market’s explosive growth will continue, Bloomberg has reported.

Deutsche Bank

At eighth-placed Deutsche Bank, which is firing thousands of workers and pulling back from other U.S. businesses, Chief Executive Officer Christian Sewing wants to make more leveraged loans. Senior managers have embarked on a charm offensive in recent weeks with leaders of the U.S. private-equity firms that control many of the non-investment grade borrowers, people familiar with the matter have told Bloomberg. The bank has increased the amount of money available for such deals.

HSBC Holdings Plc, the London-based bank known for its focus on Asia, has quietly been adding U.S. private-equity clients as it builds up its business, a person familiar with its strategy said, and has bolstered its market share along with UBS Group AG, BNP Paribas SA and ING Groep NV. Credit Agricole SA, the lender based in a Parisian suburb, arranged $2.3 billion of new U.S. leveraged loans in the first half of the year, almost as much as its total for all of 2017, the data show.

Credit Agricole’s approach is “driven by our worldwide relationship with leading, global financial sponsors and not on a market-share imperative,” said Mischa Zabotin, who oversees the French bank’s relationships with private-equity funds in the Americas.

To win business, banks compete to offer the most favorable terms -- including lower interest rates, fewer protections for investors and more debt -- and wager that they can then sell on those loans, market participants said.

“That is what is ultimately going to win deals,” said Michael Terwilliger, who oversees $152 million at Resource Alts in New York, including stakes in leveraged loans. “Deal terms, more specifically lower yields, and fewer covenants.”

Leveraged loans generate lucrative fees, but even more enticing may be the relationships with U.S. clients and the potential deals they can lead to in the future, said Tim Hall, head of debt capital markets at Credit Agricole until 2016. Yet the lure of such riches means that lenders sometimes arrange a transaction even if they must “hold their nose” at the terms, Hall said in a phone interview.

“Participating is simply the price of admission to more lucrative and high-profile side business,” said Hall. “It’s a way for European banks to get involved in other more lucrative capital markets and advisory businesses.”

The flood of borrowing has been accompanied by a deterioration in lending standards and now poses a risk to financial stability, the Bank of England has said. Investors in leveraged loans, lured by their higher returns, have accepted fewer protections against default while corporate debt is near levels last seen before the financial crisis, rating firms have said. Heavily-indebted companies may struggle to cope as the Federal Reserve hikes interest rates, which could trigger a U.S. recession, Guggenheim Partners’ Scott Minerd has warned.

Troubling Signs

Even some banks are troubled by the binge. ING, which helped arrange more than $4 billion of new U.S. loans last year, will only do deals where leverage is below a certain threshold, and has begun turning down transactions that don’t generate enough profit, according to Raymond Vermeulen, a spokesman for the Amsterdam-based lender.

“We’ve seen documentation standards deteriorating and leverage levels increasing,” Vermeulen wrote in an email. “We also view the appearance of some new entrants in the arena as a warning signal. Therefore we have imposed a cap on overall leveraged exposure.”

While banks typically sell leveraged loans on to investors, they often keep the debts on their balance sheets as they look for buyers, said the people, leaving them at risk of getting stuck with them, or “hung,” if market sentiment turns in the meantime.

The Europeans have been burned here before. Firms including Credit Suisse and Deutsche Bank lost billions of dollars on leveraged-loan assets during the financial crisis. Lenders now keep a smaller amount of debt on their books, and for a shorter amount of time, in part because regulation is making it more costly to hold such assets. Still, it can take weeks or even months to find a buyer.

‘Shocking’ Leverage

So far, defaults among American corporations remain low, encouraging lenders to underwrite more deals.

Last year, Barclays and other banks helped private-equity firms Bain Capital LP and JH Whitney Capital Partners LLC borrow $900 million to merge two companies and create Aveanna, a provider of pediatric care. The new company has since struggled with integration costs and problems with getting reimbursed in Texas, one of its biggest markets, according to ratings firms.

The latest acquisition will push Aveanna’s borrowings to more than 10 times its adjusted earnings before interest, taxes, depreciation and amortization, according to S&P’s estimate. U.S. regulators in 2013 recommended that debt shouldn’t exceed six times earnings, though that benchmark appears to have been dialed back under the administration of President Donald Trump.

“The fact that the loan market would go to these sorts of multiples is shocking to me,” said Hall, the former head of debt capital markets at Credit Agricole. “Leverage on the surface is frighteningly high.”

Billion-Dollar Deals

Tom Davies, a spokesman for Aveanna, both declined to comment on the deal.

Other U.S. transactions involving European banks show similar levels of lending. Barclays and Credit Suisse helped private equity firms Vista Equity Partners and Onex Corp. borrow more than $1 billion to create an educational company known as PowerSchool. The firm’s initial level of debt will be about 15 times’ earnings before dropping to about 10 times a year later, according to S&P.

The same two banks are also helping KKR & Co. buy BMC Software Inc. in a deal that will push the company’s borrowings to almost eight times its earnings. When two U.S. window companies merged earlier this year in a deal led by Clayton, Dubilier & Rice LLC, Credit Agricole, Deutsche Bank and UBS were among banks that arranged a $1.8 billion loan that helped dose the new corporation with debt of more than seven times.

“The European banks seem to be more willing to continue to pursue this market than some of their U.S. peers,” said David Knutson, head of credit research for the Americas at Schroder Investment Management. “But leveraged lending still has pretty meaningful margins in it. I’m not surprised they’ve focused on this part of their business.”

--With assistance from Sonali Basak and Sally Bakewell.

To contact the reporter on this story: Donal Griffin in London at dgriffin10@bloomberg.net

To contact the editors responsible for this story: Ambereen Choudhury at achoudhury@bloomberg.net, Christian Baumgaertel, Geoffrey Smith

©2018 Bloomberg L.P.