U.S. Yield Curve to Invert in Mid-2019, Morgan Stanley Says

Net U.S. treasury supply seen smaller thanks to Fed’s balance sheet unwinding.

.jpg?auto=format%2Ccompress&w=200)

(Bloomberg) -- The Federal Reserve next March will probably map out an end to the contraction in its balance sheet, helping support longer-dated bond yields, which will drop below those on shorter-dated notes by the middle of 2019, according to Morgan Stanley.

“Investors are underestimating the size of the SOMA portfolio” that will be needed to keep the benchmark overnight interest rate within the range targeted by the Fed, Morgan Stanley strategists including Sam Elprince wrote in a July 12 note. SOMA refers to the System Open Market Account, the Fed’s name for its pool of assets.

- Morgan Stanley cut its forecast for net U.S. government debt issued by the Treasury by $690 billion through 2020

- The bank sees 10-year Treasury yields at 2.75 percent by year-end, and 2.50 percent by mid-2019. It previously forecast them at 2.85 percent for end-2018 and 2.70 percent for the second quarter of 2019.

- The yield curve will invert “by mid-2019,” the analysts said. “We suggest an overweight to U.S. Treasuries.”

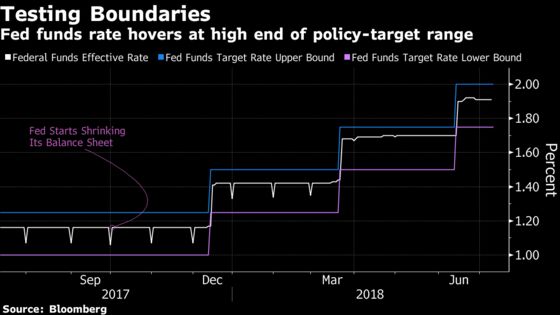

The Fed started shrinking its balance sheet last October, unwinding the unprecedented quantitative easing launched during the financial crisis. The recent phenomenon of the effective federal funds rate trading toward the upper end of the Fed’s target range has been a sign to some observers that liquidity may already be getting tight.

Some Fed officials have called for a discussion about where to take the balance sheet, with the run-off scheduled to increase by $10 billion a month, to $50 billion, next quarter. Morgan Stanley’s team sees the Fed providing a detailed account of exchanges on the issue in minutes of its December 2018 meeting, expected in early January. In March, they predict an announcement on plans to end balance-sheet normalization in September 2019.

The yield curve has been flattening almost continuously since early 2017 as the Fed kept raising rates, pushing up two-year yields, while 10-year yields rose by less. An inversion has preceded U.S. recessions in the past, and some Fed officials have expressed concern about that happening. Ten-year Treasuries now yield just 27 basis points more than two-year notes; both yields gained by about one basis point by 1:17 p.m. in New York on Thursday.

While a larger end-point for the Fed’s balance sheet than previously anticipated should support risky assets, the help won’t arrive until the contraction ends, Morgan Stanley said. On a 12-month horizon, the strategists recommended being underweight corporate credit relative to benchmark indexes.

To contact the reporter on this story: Christopher Anstey in Tokyo at canstey@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Ravil Shirodkar

©2018 Bloomberg L.P.