Run-Up To U.S. Recession Is Good Time For Emerging Markets

Emerging markets’ assets have typically outperformed when U.S. yield curve inverts.

(Bloomberg) -- If the end of easy money, a trade war and myriad geopolitical dangers weren’t enough, a U.S. yield curve poised to invert is adding to the risks for investors. But there’s one asset class that’s less of a worry: emerging markets.

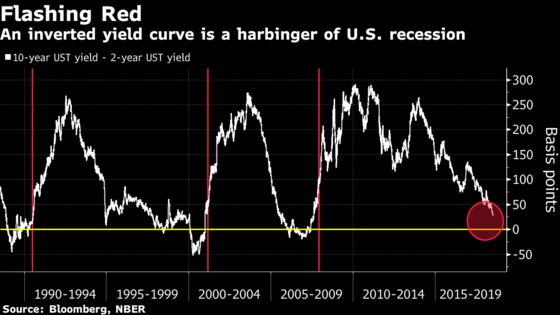

Every time the yield curve has flipped in the past three decades, sending shorter-term interest rates above longer-term ones, the U.S. economy has entered a recession within 12 to 24 months. While that correlation makes the inverted curve a risk-off signal, it’s been a different story with emerging-market assets.

History suggests that the inversion has no influence on emerging markets. At best, it might be a bullish signal.

Read: The U.S. Is Closer To a Recession Than You Think: Macro View

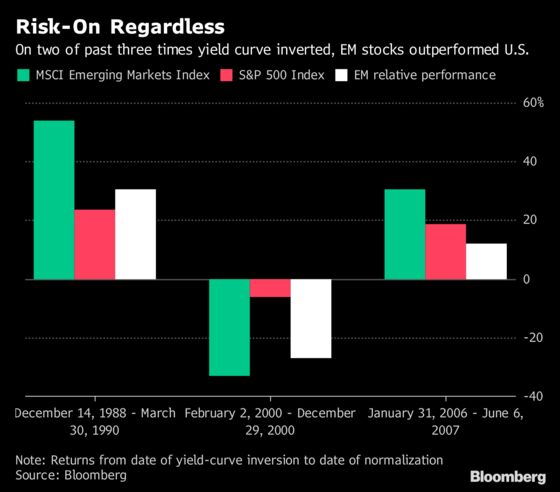

Developing-nation stocks outperformed U.S. equities when the spread between 10-year yields and 2-year yields was negative in the run-up to a recession in 1990 and 2007. They trailed U.S. stocks in 2000, before the economy started contracting the following year, leaving the score at 2-1 in favor of emerging markets.

With bonds and currencies the picture is more clear-cut. Both climbed against U.S. assets in the last two recessions (data before the 1990 recession isn’t available). Investors also cut the risk premium for owning emerging-market sovereign dollar bonds rather than U.S. Treasuries on both occasions.

Developing-nation assets react to many external and idiosyncratic factors, and the yield curve isn’t able to influence their moves compared with those factors, according to William Jackson, an economist at Capital Economics Ltd. in London. But once a U.S. recession gets entrenched, it might affect risk appetite, pushing emerging markets toward underperformance, he said.

The spread between 10-year and 2-year yields is at 27 basis points, the lowest since August 2007. Similar gap between 7-year and 2-year rates is at 24 bps, the narrowest since at least 2009. The 5-year rate is just 17 bps away from the 2-year one. They all continue to fall as growing concern about a recession is pushing investors to buy longer-dated Treasuries, while Federal Reserve rate increases are boosting the yield on shorter-term bonds.

July marks the 109th month of continuous economic expansion in the U.S. after it emerged from the last recession in June 2009, according to the National Bureau of Economic Research. That’s the second-longest phase of growth since 1854, beaten only by a 120-month stretch in the 1990s. The law of averages dictates that it’s a late-stage economy and a recession may be closer than the markets are pricing in.

Read: Bill Gross Warns 1-2 Fed Hikes Max in 12 Months ’or Recession Ahead’

To contact the reporter on this story: Srinivasan Sivabalan in London at ssivabalan@bloomberg.net

To contact the editors responsible for this story: Dana El Baltaji at delbaltaji@bloomberg.net, Alex Nicholson, Robert Brand

©2018 Bloomberg L.P.