If Trump’s Problem Is OPEC, His Solution Is Iran

(Bloomberg Opinion) -- President Donald Trump has once again taken to Twitter to slam OPEC for driving up oil prices. The group is a useful scapegoat on which to pin the blame for rising gasoline prices at home, but getting it to pump more crude won’t bring them down for long. The way to really lower prices is for him to change his policy on Iran.

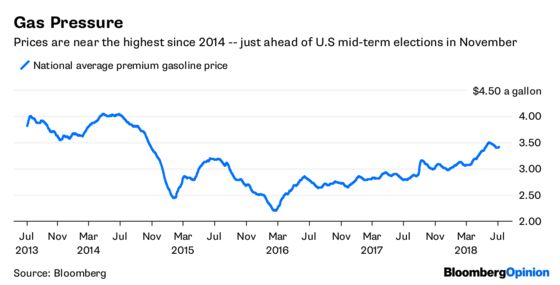

Unfortunately, that’s not likely to happen, so oil prices could well keep rising. Oil prices have climbed by more than 50 percent in a year, and very nearly touched $80 a barrel last week as traders anticipated that the world’s margin of spare production capacity available to offset supply disruptions is set to seriously shrink.

They know something that the president either can’t or won’t understand: When sanctions on Iran come into force in November, producers don’t have the scope to make up for its lost output. If Trump succeeds in halting all of Iran’s oil exports, they will have to replace 2.7 million barrels a day of Iranian supply. That’s a big hole to fill.

And if they can’t do it, the cost will be steep. According to Bank of America Merrill Lynch, a complete shutdown of Iranian sales could push oil prices above $120 a barrel if Saudi Arabia can’t keep up.

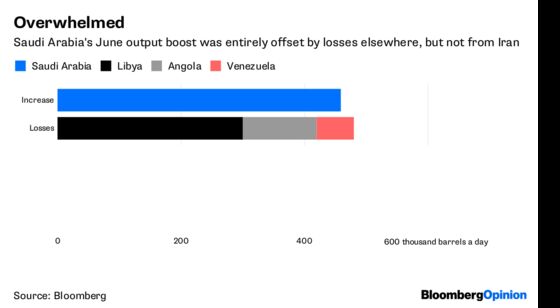

In Trump’s world, the gasoline prices he focuses on should already be headed down. On Wednesday Saudi Arabia said it pumped about 10.5 million barrels of crude a day last month, preempting the deal reached among the OPEC+ group of countries in Vienna. That’s an increase of about 500,000 barrels a day from May, making it the biggest month-on-month jump in the kingdom’s output since June 2004.

But there’s a problem. The production jump ought to have shown up as a similar surge in total OPEC output. It didn't. The increase was entirely overwhelmed by declines elsewhere in the group. Add in the loss of 350,000 barrels a day of Canadian supply from an explosion at an oil-sands upgrader in Fort McMurray, and the entire boost from Saudi Arabia is gone.

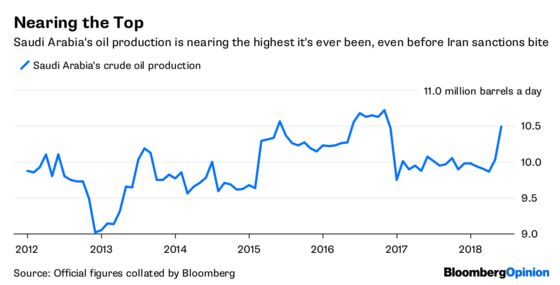

The simple truth is there isn’t enough spare production capacity in the world to replace the complete loss of Iranian exports. Saudi Arabia can boost output to 11.5 million barrels a day immediately and go to 12.5 million in six to nine months, Crown Prince Mohammed bin Salman told Bloomberg in 2016. He’s said nothing since that interview to suggest the figures have changed. Others are less optimistic — the International Energy Agency said at the time that going beyond 11 million would require boosting costly offshore production.

The most that Saudi Arabia has ever pumped on a monthly average basis is 10.72 million barrels a day in November 2016, according to official figures provided to OPEC. Anything beyond that is uncharted territory. That doesn’t mean it’s impossible, just uncertain. All we can say for sure at this point is that it has around 200,000 barrels a day of proven spare capacity immediately available.

There may be a couple of hundred thousand barrels a day in the United Arab Emirates and Kuwait, and as many as 500,000 in the Neutral Zone shared by Saudi Arabia and Kuwait. Fields there have lain idle since 2015 after Saudi Arabia closed them on environmental grounds. There are now suggestions that they could be reopened in the coming months.

The rest of OPEC may hold another hundred thousand barrels of spare capacity and, outside the group, Russia has already begun to boost its production. Russia has never shared an official estimate of how much idle production capacity it could restore. Forecasts vary from 215,000 barrels a day from Renaissance Capital to some 500,000 barrels seen by state-run Gazprom Neft PJSC, the nation’s No. 3 producer.

But that’s about it, around 1.5 million barrels a day of immediately available oil to replace what Iran won’t be pumping. That’s not enough.

Releasing oil from the U.S. Strategic Petroleum Reserve might provide a theoretical short-term answer, but that won’t work. It it is in the wrong place. American refineries are already running nearly flat out, so any additional supply from the SPR would have to be exported and it would take a couple of months to get it to the Asian refineries who would need it.

So when Trump tweets this:

it’s clear that, as energy consultant FGE said in a report last week, “either President Trump’s advisers do not understand the oil market or he simply just does not listen to them.”

There is one way the president could quickly achieve lower prices, and it’s staring at him in the mirror. He could reimpose sanctions on Iran in a much more gradual manner, instead of all at once on Nov. 4. Sure, it would prolong the process, but it would also ease the pressure on oil markets and those all-important gasoline prices. Unfortunately, patience doesn’t seem to rank highly as one of the president’s virtues.

Pumping more crude into the market may seem as if it ought to ease fears of a supply shortage when Trump’s Iran sanctions begin to bite — but any relief will be short-lived. Oil prices will reflect this.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

©2018 Bloomberg L.P.