Five Charts Show Why European Stocks Are Developed World’s Worst

Investors’ patience with European stocks is wearing thin.

(Bloomberg) -- Investors’ patience with European stocks is wearing thin.

This year was supposed to be the moment when European equities would finally catch up with the U.S. stock market, lifted by a revival in economic growth and corporate earnings while worries over the region’s populist leaders was set to fade. Instead, Europe has been the worst performer among developed countries in the first half of the year.

Unnerved investors, including Schroders Plc, have pulled out of overweight positions on concerns spanning from Italy’s political crisis to the damage from a simmering trade war and the European Central Bank’s dithering on the interest rate outlook. The level of disenchantment has been so strong that the region’s stock valuations have tumbled to near 2016 levels, prompting a number of contrarian asset managers to start shopping for bargains.

Here are five charts that look at key features of European stocks following their roller-coaster rise in the second quarter:

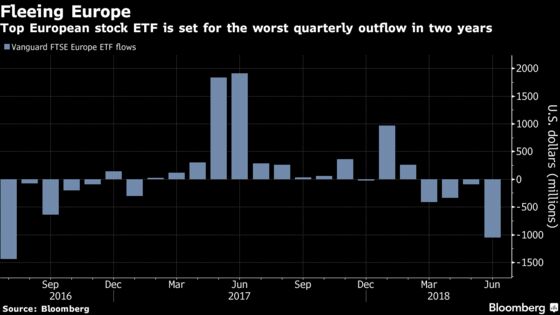

The biggest European equities-focused exchange-traded fund Vanguard FTSE Europe ETF has had a rough time in the past three months, seeing outflows of about $1.5 billion. This is the biggest redemption since the the third quarter of 2016. The region’s equities have been a laggard among global stocks this year in terms of investments, suffering $23 billion in outflows, according to Barclays Plc strategists.

In contrast, global, Japanese and emerging funds have been seeing inflows in 2018, with the U.S. catching up in May thanks to fresh investor contributions. Some investors may have rotated out of European equities and into the U.S. market, spooked by renewed worries over the future of the euro area as Italian populist parties made a deal to form a new government.

While the S&P 500 Index has been advancing steadily since 2009, reaching a record high in January after gains of about 300 percent, the Stoxx 600 Europe Index rose just 130 percent in the same period and has continued to lag, widening its valuation discount over the past month. The Stoxx 600 now trades at a price-to-book ratio that is almost half that of the S&P 500 Index.

Europe-specific concerns, as well as Trump’s tariff threats against the region’s automakers, have been weighing on the sentiment. In contrast, the U.S. stock market has benefited from brisk gains in tech shares, a sector that represents about a quarter of the S&P 500 benchmark.

The plunge in European banking stocks has been a key factor in the region’s underperformance this year, after rallying last year on bets the ECB was getting closer to raising interest rates. Higher rates are expected to boost the profitability of banks, still reeling from the region’s sovereign debt crisis. However, concerns about the financial strength of Italian lenders, Deutsche Bank’s AG struggle to revamp its strategy as well as the ECB’s pledge this month to keep the key rate at zero until at least next summer have turned the sector into the worst performer of 2018.

The concerns are very similar to those seen two years ago, when the market was shaken by jitters over Deutsche Bank’s future and an extended period of low interest rates. As a result, European banking stocks are now trading at the lowest price-to-estimated earnings ratio since August 2016.

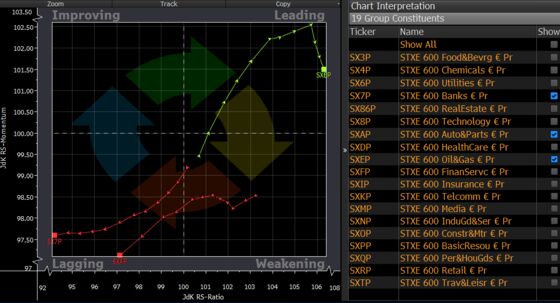

The Relative Rotation Graph shows that the indexes for banking stocks (SX7P) and automakers (SXAP) are moving from the weakening quadrant to the lagging one, a sign that these sectors are losing investors’ favor. Carmakers are also one of the worst performing European industries this year with a loss of 11 percent, hurt by jitters over potential U.S. tariffs on the sector. On the other hand, the oil stocks index (SXEP) has moved from the weakening to the leading quadrant in a bullish sign. Energy shares have been this year’s top performer among sectors, due to a recovery in oil prices amid expectations of global supply disruptions.

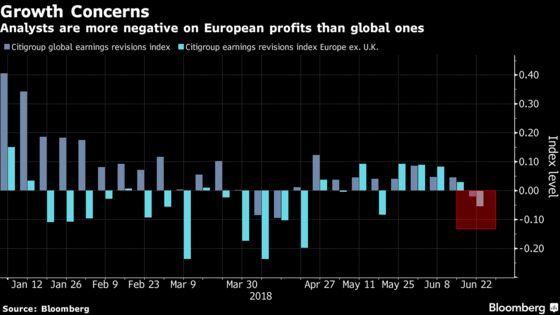

A Citigroup Inc. index tracking earnings revisions in Europe, which in January rose to the highest level in seven months, dropped last week to a two-month low, signaling that the number of analysts who cut profit estimates for the region’s companies outnumbered those who raised them.

To be sure, the relative caution on European equities may offer some upside for the market, just when the much-awaited rebound in euro-area growth momentum may have finally begun after the composite PMI rose in June. However, analysts and investors remain prudent about the impact of the U.S.-China trade spat on global growth.

To contact the reporter on this story: Ksenia Galouchko in Moscow at kgalouchko1@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Monica Houston-Waesch

©2018 Bloomberg L.P.