Magnus Sees Yuan Sliding to 2008 Low as China Policy Shifts

Yuan's Set for 7 as Slide Evokes China 2015 Turmoil, Magnus Says

(Bloomberg) -- China’s yuan will head in time to its weakest since 2008, and the country’s stock slump also has further to go, according to the veteran global economist George Magnus.

The currency’s decline will only deepen as monetary policy on the mainland diverges from that of the Federal Reserve, Magnus said in a telephone interview this week. As for what’s going on right now -- the steepest drop for the yuan since the devaluation almost three years ago, and a bear market in stocks -- it reminds him of the 2015-16 selloff, and it’s hard to tell how officials will respond, he said.

“I’m not anxious about a policy-induced crisis on the currency but the signals really are quite confusing,” Magnus said. Though the People’s Bank of China has repeatedly set the yuan’s reference rate against the dollar this week at stronger levels than analysts and traders had anticipated, other metrics show little sign of action to stem the sharp drop.

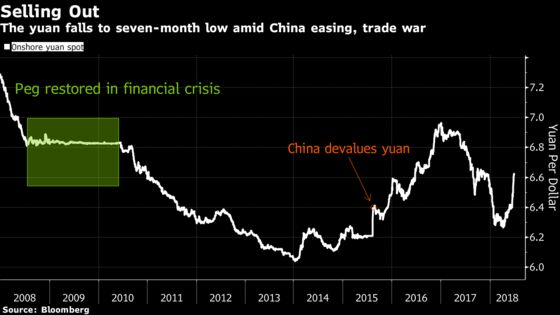

The managed currency has tumbled 3 percent in the past two weeks as tensions with the U.S. over trade restrictions escalated, spurring speculation among some market players that China is effectively depreciating the yuan as a weapon in the dispute. A cheaper currency could make Chinese exports more competitive -- though the devaluation in 2015 also had the effect of spooking stock investors around the world.

“This is a double-edged sword and this is why it becomes uncertain or problematic for investors,” said Magnus, who served as chief international economist at major banks from the 1980s and is now a China Centre associate at the University of Oxford. “We’ve been here before, the situation is very similar to 2015-2016 when the exchange rate was under pressure” and the PBOC had to spend foreign-exchange reserves to prop it up, he said.

The yuan rose onshore for the first time this week, trading at 6.6181 per dollar at 4:49 p.m. in Shanghai, while the offshore rate snapped a record 11-day record losing streak. The Shanghai Composite Index pared its worst monthly decline since January 2016. The equity gauge is down 20 percent from its January high, meeting the description of a bear market.

“My worry is that this 20 percent correction in stocks is no reason why you shouldn’t have half as much again,” said Magnus, who correctly said in July 2015 that Chinese stocks would slump further, and then accurately called the end of the rout in January 2016. “Not that there’s no floor, but we haven’t reached a bottom if the trade situation continues to deteriorate.”

As for the currency, it may depreciate past 7 per dollar over the next year -- a level unseen since before officials pegged it for a time during the global financial crisis -- as China’s monetary policies continue to diverge from those of the Federal Reserve. The PBOC has shifted gears this year from pursuing concerted financial deleveraging to moving to inject liquidity to support credit growth in the so-called real economy.

In the short term, officials may intervene to stabilize the currency and avoid giving President Donald Trump’s administration an excuse to charge Beijing for using the currency as a trade tool, Magnus said.

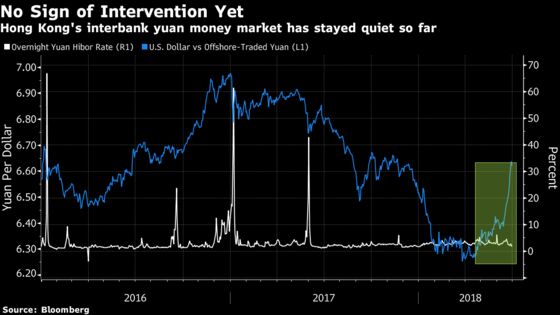

So far there’s been little sign of such intervention. When China sought to stem the yuan’s slide in 2016, one instrument used was squeezing liquidity in the interbank yuan money market in Hong Kong. The Hong Kong Interbank Offered Rate has yet to show any similar move.

“When the PBOC is carefully managing the exchange rate, it opens to investors or speculators and to market participants the opportunity to guess what its policy is going to be,” Magnus said.

Magnus said that though policy makers have eased liquidity recently -- including through a targeted reduction of banks’ required-reserves ratio last weekend -- ultimately they will need to push on with the deleveraging campaign to reduce financial risks. That’s set to weigh on stocks, though the biggest blow would be a forced tightening to halt a disorderly decline in the yuan, according to Magnus.

“China would still be left with the issue about the accumulative impact of domestic credit tightening on the economy and on earnings -- that’s not going to go away whatever happens to the yuan and the trade row,” he said.

The leadership would have to decide “either to stick with the deleveraging campaign, which would be negative for growth, profits and markets, or if they’re going to back away from that and give a temporary relief to the market by kicking the can six, 12 months down the road,” Magnus said.

To contact the reporter on this story: Kana Nishizawa in Hong Kong at knishizawa5@bloomberg.net

To contact the editors responsible for this story: Richard Frost at rfrost4@bloomberg.net, Christopher Anstey, Cormac Mullen

©2018 Bloomberg L.P.