Loan Managers Sniff a Chance to Buy as Secondary Market Slides

Loan Managers Sniff a Chance to Buy as Secondary Market Slides

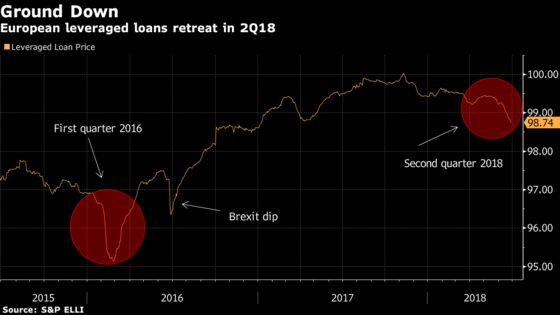

(Bloomberg) -- Leveraged loans are closing out their weakest spell in more than two years after a wave of M&A supply triggered a long-awaited correction in Europe’s overheating market.

This has paved the way for loan managers to hunt for paper in the secondary market that was previously only available above par. Investors have also been busy replacing tightly priced portfolio names with better yielding new issuance as primary spreads widen, while rejecting aggressive documentation.

The secondary market is headed for its biggest quarterly drop since at least the first three months of 2016, losing about half a point off the average mid-level price since the end of March, based on the S&P ELLI.

With the technicals driving the decline unlikely to change soon, loan managers should continue to find opportunities into the third quarter.

Loan issuance has swelled 30 percent over the year, the main driver of the gradually softening secondary market. Arranging banks see the pace of the primary market remaining strong into the second half, which may include some very large deals.

Arrangers Seek Support for Jumbo LBOs as Summer Pipeline Builds

But even if supply does ease off, the credit cycle is moving on. The ECB’s bond buying program will halt by the end of the year, and the high-yield bond market has comprehensively repriced this year as investors look ahead to potential rate rises.

Appetite for paper continues via a long pipeline of CLO deals and other fund formats. But triple A spreads have widened during the second quarter, while some high-yield funds have lightened up their loan exposure in favor of buying bonds. In addition, repayments into loan funds have been scarce this year.

No Snap Back

Back in first quarter of 2016, the secondary market dropped and then snapped back fast. Macro risks had been weighing on the market through late 2015, and when a bout of M&A supply arrived in Europe in January 2016, secondary levels slumped and lenders sold the cheapest names out of their portfolios.

But within weeks, risk appetite for loans roared back and outstripped supply. CLO issuance expanded and a powerful rally took hold, lasting through to late 2017 when the average mid-price briefly nudged over par.

This time, the chances of a swift recovery and another long rally are slim. Instead, investors refer to a “war of attrition”.

On the basis that the loan market recalibrates and stabilizes in the second half of the year, the risk of primary loans trading poorly on the break should diminish and encourage more investors to step off the sidelines. But relative value pressure versus high-yield makes it hard to see single B credits price at 300-325 basis points over the base rate again.

(Ruth McGavin is a leveraged finance strategist who writes for Bloomberg. The observations she makes are her own and not intended as investment advice.)

To contact the reporter on this story: Ruth McGavin in London at rmcgavin1@bloomberg.net

To contact the editors responsible for this story: Tom Freke at tfreke@bloomberg.net, V. Ramakrishnan

©2018 Bloomberg L.P.