Semiconductor ETF Gets Lots of Cash, But Not for What You Think

Semiconductor ETF Gets Lots of Cash, But Not for What You Think

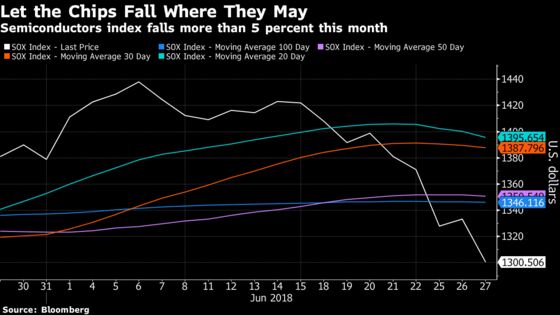

(Bloomberg) -- So much for semiconductor stocks hitting a floor.

A record inflow into an exchange-traded fund tracking chipmakers that looked like a bullish signal for the industry actually may have been another bearish beacon for a group that’s had a rough couple of weeks.

The iShares PHLX Semiconductor ETF, known by its ticker SOXX, saw a record $181 million worth of inflows Tuesday. But the new cash may have been indicative of so-called create-to-lend activity, where shares of a fund are created for traders to borrow and sell short.

Financing costs have increased recently for the more liquid semis fund -- the VanEck Vectors Semiconductor ETF, or SMH -- rising as high as 11.3 percent on June 21, the most in at least the past year, according to data from S3 Partners. Since then, SMH shares as a percent of the float have fallen, the data show.

The popularity of shorting these stocks is easy to understand considering the Philadelphia Stock Exchange Semiconductor Index has dropped more than 7 percent since June 13.

“The SOXX inflow, or creation, could be connected to the lack of shorting supply in the SMH,” according to Josh Lukeman, head of ETF market making for the Americas at Credit Suisse Group AG.

Semiconductor stocks were among the biggest decliners in the selloff in technology shares that started last week and led to a 3 percent loss in the semiconductor index on Monday. The amount of SOXX shares shorted increased to about 31 percent of the float on Wednesday, the highest in over a month, according to data from S3 Partners.

However, the data don’t definitively point to a short sale. The inflows could be showing a “mix trade” as investors try to capture the difference in exposures between SOXX and SMH. For example, unlike SMH, SOXX doesn’t hold NXP Semiconductors NV or Cavium Inc., two companies that are in the process of being acquired.

“Traders certainly could have been put off by the uncertain borrow cost in SMH and rolled from that fund into SOXX,” said Dave Lutz, head of ETFs at JonesTrading Institutional Services. “Or it could be wrapped in a stronger dollar trade, with 92 percent of SOXX domiciled in U.S.A., versus 82 percent in SMH.”

--With assistance from Sarah Ponczek and Tom Lagerman.

To contact the reporter on this story: Carolina Wilson in New York City at cwilson166@bloomberg.net

To contact the editors responsible for this story: Courtney Dentch at cdentch1@bloomberg.net, Eric J. Weiner, Andrew Dunn

©2018 Bloomberg L.P.