Quantitative Tightening Is Roiling Markets

On the QT, Markets are Being Roiled by Quantitative Tightening

(Bloomberg) -- That whooshing sound you hear is the draining of $1.4 trillion worth of global liquidity.

Quantitative tightening, or the unwinding of central banks’ extraordinary stimulus, has been the primary driver of asset-class performance this year, Bank of America Merrill Lynch analysts say. The march higher in U.S. interest rates and tighter financial conditions mean securities that did well during quantitative easing, such as corporate bonds and emerging-market debt, are now underperforming, while “QE losers” have become stars.

The year marks a shift in a tide of global liquidity that helped push up asset prices, according to Merrill Lynch’s analysis. Securities purchases from the Fed, European Central Bank and Bank of Japan are just $125 billion year-to-date, well below the $1.5 trillion run-rate of 2017, they estimate. That suggests markets are missing an injection of some $1.38 trillion thanks to policy makers changing tack.

Liquidity will see an outright contraction in six to eight months, the strategists estimated -- one reason they’re bearish on global markets even after recent declines. The following is a look at what’s changing in global markets.

Short-Term Rates

Treasury bills have been among the securities that reacted fastest to monetary-stimulus withdrawal. Yields steadily rose as traders responded to the potential for more aggressive tightening from the Fed, as well as increased bill supply to fund fiscal deficits.

Investors are taking advantage. ETFs that invest in ultra short-term debt have attracted almost $18 billion so far this year, accounting for about 35 percent of their assets under management, according to data compiled by Bloomberg.

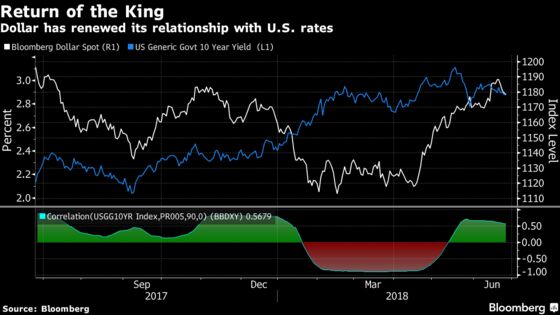

King Dollar

The dollar has renewed its relationship with the rates market, moving higher in sync with benchmark rates. The increasing yield premium over peers finally brought an end to a five-quarter slump in the Bloomberg Dollar Index. It reached a one-year high last week.

“The dollar’s doing a stalwart job of re-coupling with yields, and in real effective terms it’s not a million miles from getting back to its January 2017 peak,” Societe Generale SA strategist Kit Juckes said in a note last week. Since both real and nominal yields are higher than January 2017 and the “global economy overall is facing political dangers,” the dollar could return to its cycle peak soon enough, he said.

Emerging Markets

The combination of higher U.S. yields and a stronger greenback has rippled through developing markets, as investors fret over the ability of developing nations to pay off dollar-denominated debt. A fifth of emerging markets and middle-income countries have debt levels above 70 percent of GDP, according to the IMF, and developing economies’ dollar borrowings grew 10 percent in 2017.

“This rolling EM meltdown is another expression of the ‘QE to QT’ reality, as the easy carry environment of the post-global financial crisis period is now coming home to roost,” said Charlie McElligott, a strategist at Nomura Holdings Inc. Investors sold a record $6 billion from dedicated global EM funds last week, according to Sanford C. Bernstein & Co.

The house view of Goldman Sachs Group Inc. that the emerging-market selloff should bottom by July has been met with “significant opposition from macro investors, who argue that the reign of ‘easy money’ is shifting and EM is likely to see large outflows going forward,” analysts Caesar Maasry and Ron Gray said in a June 27 note.

In an effort to explore a worst-case scenario, the pair outline a “severe bear case” in which some $130 billion of EM outflows send assets back to mid-2015 levels. That would imply a 14 percent sell-off in EM equities, a 175 basis-point widening of credit spreads and 44 basis point increase in local rates, the analysts said.

Credit Divergence

Longer-duration investment-grade bonds -- or those most exposed to moves in rates -- have underperformed their shorter-duration high-yield counterparts. The Bloomberg Barclays U.S. Corporate Investment Grade Index is down over 3 percent this year, while the high-yield equivalent is up about 0.5 percent.

The moves have also triggered an unusual divergence between equity and credit markets. While stock investors have been avoiding leverage, preferring the shares of companies with stronger balance sheets, credit traders have gone the other way, seeking out those with the riskiest debt.

The equity-credit gap “confirms investors remain in a barbell of ‘uber growth’ in equities and ‘uber yield’ in credit, which has been the dominant themes during the QE-era,” said Tommy Ricketts, investment strategist at Bank of America. “That trade is getting narrower and narrower now though.”

Volatility

Volatility has also sprung to life in 2018, with the Cboe’s Volatility Index averaging 16.31 this year, compared with 11.09 in 2017. Even so, for Unicredit SpA strategist Elia Lattuga, volatility had appeared “a tad too detached” from recent developments across the globe.

“As unprecedented measures are reined in, financial conditions will tighten and global asset prices will have to adjust to the new regime,” Lattuga wrote in a recent note to clients. “We think that credit-spreads and equity valuations are set to become increasingly sensitive to changes in market sentiment and macro developments.”

--With assistance from Sid Verma.

To contact the reporters on this story: Cormac Mullen in Tokyo at cmullen9@bloomberg.net;Eric Lam in Hong Kong at elam87@bloomberg.net

To contact the editors responsible for this story: Tracy Alloway at talloway@bloomberg.net;Christopher Anstey at canstey@bloomberg.net

©2018 Bloomberg L.P.