Hidden Shorts Build as London Funds Seek Casualties of Cycle

Hidden Shorts Build as London Funds Seek Casualties of Cycle

(Bloomberg) -- Investors are accused of careening into a potential downturn unprepared.

The critique may prove undeserved.

Behind the scenes, they’re finding all manner of strategies to short the credit cycle, as they brace for a wave of maturing debt just as cracks emerge in the synchronized growth story.

A faltering euro, an ascendant dollar and fears U.S. protectionism will sink global output have prompted a rethink for BlueBay Asset Management’s Geraud Charpin in London’s Mayfair district. The money manager at the $60 billion firm is lavishing ever-more capital shorting companies squeezed by tightening financial conditions, while he eases up on allocations to new bonds.

"We have seen a number of new developments since the beginning of the year that are all going against our bullish scenario,” Charpin said in an interview. “Our short book is at least twice as big as it was at the beginning of the year and our long book is at least 30 percent smaller than it was."

He’s one of a growing number of investors scrutinizing swelling corporate leverage following a decade of easy-money policies. Heavyweight firms like Guggenheim Partners are pointing the finger at corporate debt burdens as the next culprit to kick off a financial crisis. Whereas consumers sparked the 2008 meltdown, a decade later business balance sheets look more fragile.

“I think the real bubble is in the corporate sector,” said Edmund Shing, global head of equity and derivative strategy at BNP Paribas SA in London. “If leverage is cheap, the temptation for management is to leverage up.”

Strategists at the French bank have made it easy to prepare for an "eventual credit crisis” by creating a basket of 30 European companies with above-average leverage and heightened bankruptcy risk. They encourage investors to short the group with total-return swaps, as a relative-value trade or to hedge a long position in equities.

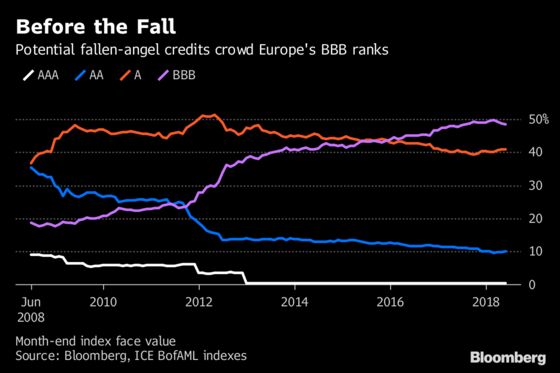

The stocks are screened for liquidity, drawn from the growing ranks of European BBB issuers, the lowest rung on the investment-grade scale, and junk credits. The result is a group tilted towards Italy and Spain, as well as those in the consumer, industrial, telecom and utilities sectors.

The basket has underperformed the Stoxx Europe 600 Index by 14 percent over the past year. Today’s BBBs, for example, could be tomorrow’s fallen angels over the next two years, investment-grade companies whose ratings are cut to junk grade.

“The real problem could occur at the BBB level, where companies are hanging on to investment grade and suddenly they lose it as refinancing gets harder, and the cash flows aren’t coming,” said Shing.

With defaults far lower than the historic average, even short-sellers betting on a mere correction may be stuck with costly insurance policies, for now. Meanwhile, investors remain largely faithful to benchmarks, with positioning in European credit markets only just dipping below neutral in a June survey by Bank of America Corp.

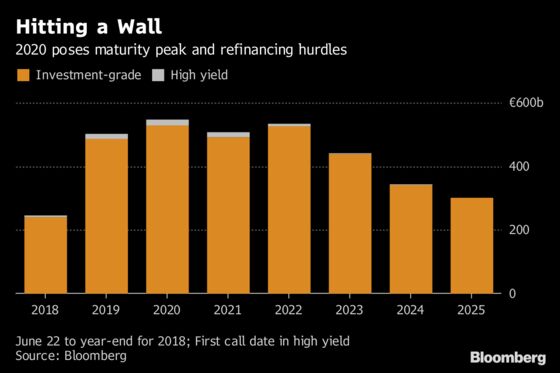

It may just be a matter of patience. A wall of maturing debt peaks in 2020, narrowing refinancing avenues for the neediest borrowers as the competition for capital intensifies.

“2020 is the year when things are really expected to fall off the cliff but it may happen before,” said Antler Capital Partners LLP founder Georges Gedeon.

Gedeon knows a thing or two about falling credit cycles. The former investor at London-based GLG Partners Inc. amassed shorts on overleveraged companies at the peak of the financial crisis, spinning double-digit returns in its wake.

This time around, the European Central Bank’s taper is likely to expose weak companies that had been propped up by stimulus, all while euro-zone growth slows and the U.S.’s threatened trade war looms large, according to Gedeon.

“Europe is much more exposed to a trade-related slowdown and so are emerging markets, so it could have widespread repercussions,” he said. His fund, launched in December, offsets positions in corporate credit, comprising about 70 percent of the fund, with equity puts.

One of Antler’s earliest trades was anticipating the balance-sheet damage to Danish phone company TDC A/S after a takeover. Another target is subordinated hybrid securities sold at the height of the bull market that have no fixed maturity date and allow issuers to postpone coupon payments.

French mall operator Unibail-Rodamco SE issued perpetual hybrids in April to help fund its acquisition of Westfield Corp., including shopping malls in east and west London. The largest portion of the sale, for 1.25 billion euros ($1.5 billion) of securities callable in October 2023, currently yield 2.5 percent. That compares with an average of 3.1 percent offered by global investment-grade corporate bonds, according to Bloomberg Barclays index data. A spokesman for Unibail declined to comment on valuation.

“There’s so much mispriced risk you don’t need a lot to cause a nasty surprise,” Gedeon said.

--With assistance from Tasos Vossos and Thomas Beardsworth.

To contact the reporters on this story: Yakob Peterseil in London at ypeterseil@bloomberg.net;Cecile Gutscher in London at cgutscher@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma, Todd White

©2018 Bloomberg L.P.