How Index Funds Can Combat This Hidden Cost

How Index Funds Can Combat This Hidden Cost

(Bloomberg Opinion) -- Friday was a big day in the world of indexes. It was also a costly one for index investors.

I’m referring to the annual reconstitution of the FTSE Russell indexes — the day that the index provider officially updates the components and allocations of its indexes, such as the popular Russell 1000 Index and Russell 2000 Index.

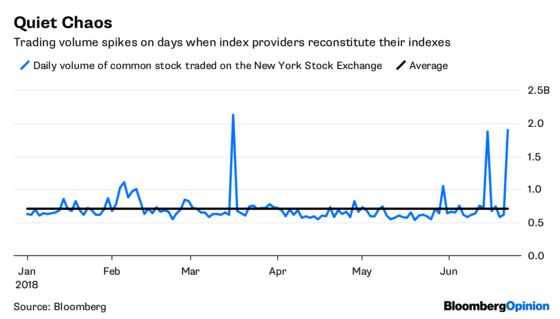

It’s also the day mutual funds and exchange-traded funds that track a FTSE Russell index revamp their portfolios to match it. The result is a torrent of trading. Roughly 1.9 billion shares of common stock traded on the New York Stock Exchange on Friday, according to volume calculated by Bloomberg. It was the second-busiest trading day of the year and nearly triple this year’s average daily volume of 712 million shares.

Investors hardly noticed, which isn’t surprising. Many of them buy index funds so that they don’t have to pay daily attention to markets. Index providers and index funds also take care to keep the chaos quiet. Alec Young, FTSE Russell’s managing director of global markets research, told CNBC on Friday that “if we do our job right, no one’s going to know that much happened.”

To that end, FTSE Russell announces preliminary changes to its indexes two weeks before reconstitution day to minimize surprises. The final list is released on the big day, and changes take effect based on that day’s closing market prices.

There’s just one predictable problem. All the money piling into the same stocks pushes up their prices, making them more expensive, on average, for index funds to buy. Inversely, the money leaving stocks depresses prices, making them more expensive to sell.

This side effect of index reconstitution is well documented. A 2003 study by Jim Quinn and Frank Wang, for example, observed that stocks newly added to several popular indexes — including the Russell 3000 Index — had abnormally high returns between the time that their addition was announced and reconstitution day, and that some of those returns subsequently reversed. The authors call it the “hidden cost” of indexing.

That cost is hard to spot because it’s baked into the index’s return. Remember that changes to the index are based on closing prices on reconstitution day, which means that the impact of buying and selling triggered by those changes is absorbed by the index. Indexes, in other words, are hit with the cost of trading along with the funds that track them.

It’s also tricky to quantify the precise cost to investors. For one thing, it’s hard to isolate the impact of reconstitution from the myriad other variables that move stock prices. In addition, stocks can move from one index to another — from a large-cap to a small-cap index, for example — so a trading cost for one index fund could be a savings to another.

The fact that this trading cost is hidden and difficult to measure probably explains why cost-obsessed index investors haven’t clamored for a fix. Still, to its credit, FTSE Russell has tried to dampen the cost of reconstitution by rebalancing its indexes only once a year, by incorporating “buffer zones” around index rules to reduce turnover and by giving advance notice of changes. It’s not clear what else index providers can do.

But index funds can do one simple thing: They can give fund managers more room to stray from the index. Many funds are required to replicate the index, which means they must hug the index at any cost. Instead, managers should be given several months after reconstitution day to conform to the index. They should also have discretion to ignore changes where the cost of trading would outweigh the expected benefit of the change.

Some managers already have that freedom. Indexes such as the Bloomberg Barclays U.S. Aggregate Bond Index have thousands of components, and it’s often not practical — or even necessary — to own all of them. Rather than replicate the index, some managers have discretion to buy a portion of the index, and they’re still able to match the index’s performance.

Index investing is popular because it’s cheap and transparent. But when it comes to trading costs around reconstitution, it’s neither. It’s time to change that.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

©2018 Bloomberg L.P.