Better to Round Up Than Down

Better to Round Up Than Down

(Bloomberg Opinion) -- Four is the loneliest number.

If a company has one million shares outstanding and makes $1,014,900 of net income in a quarter, it has earnings per share of $1.0149, which rounds—in the normal procedure of rounding EPS to the nearest penny—to $1.01. If instead it makes $1,015,100 of net income, it has earnings per share of $1.0151, which rounds to $1.02. A difference of $200—0.02 percent—in net income leads to a difference of $0.01—0.99 percent—in earnings per share. That $200 is 50 times more powerful in EPS than it is in income.

On the other hand, if it has net income of $1,013,900, it has earnings per share of $1.0139, which rounds to $1.01. If instead it makes $1,013,700, it has earnings per share of $1.0137, which rounds to $1.01. Or if it makes $1,010,000, for that matter, still $1.01. The difference of $200, or $3,900, in net income has no effect on earnings per share.

There is some room for judgment in allocating revenues and expenses between quarters. If your printer is running low on toner on June 29, you can buy more on June 30, or on July 1. If the company has $1,013,900 of net income one quarter, and $1,014,900 of net income the next quarter, arguably an opportunity has been missed. That’s $1.01 of EPS each quarter. It’s so much better to have $1,013,700 and then $1,015,100: That’s $1.01 of EPS one quarter and $1.02 the next.

Well, I mean, “so much better.” It’s one penny of EPS better. It will not cure cancer. But if you are the type of chief financial officer who cares a lot about pennies of EPS, at the type of company that lets you exercise your creativity, you might care a lot about getting that $1.02 of EPS, even if it means waiting a bit too long to refill your toner.

But the Securities and Exchange Commission is onto your tricks:

Federal regulators are investigating the case of the missing “4,” exploring the numeral’s conspicuous absence in quarterly reports that could mean companies have improperly rounded up their earnings per share to the next highest cent, according to people familiar with the matter.

Enforcement officials at the Securities and Exchange Commission have sent queries to at least 10 companies, asking the firms to provide information about accounting adjustments that could push their reported earnings per share higher, one person familiar with the matter said.

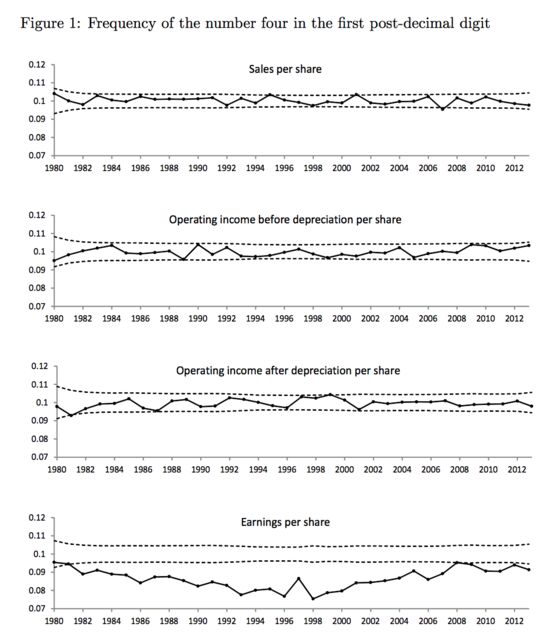

The investigation comes out of this delightful paper from Nadya Malenko and Joseph Grundfest titled “Quadrophobia: Strategic Rounding of EPS Data,” which found that $1.014 is a less likely earnings-per-share result than $1.013 or $1.015: Four is the first digit after the decimal point in only 7.9 percent of earnings-per-share results for companies covered by research analysts. And this isn’t true of other per-share results that aren’t as closely watched (and managed) as EPS:

If you are managing the tenths-of-a-penny digit of earnings per share, the effect of that on operating income before depreciation per share will be pretty much random. There are lots of other suspicious facts. “The incidence of quadrophobia increases (declines) when firms gain (lose) analyst coverage and is more pronounced in pro forma earnings in a manner consistent with capital market pressure causing strategic rounding”: The more people are paying attention to earnings per share, the more tempting it is to round them up.

But what’s especially interesting is that this is not a general feature of the capital markets, a case of all companies uniformly responding to incentives. Instead, there seem to be some companies with cultures of strategic rounding and some without:

We also find that quadrophobia is persistent: companies with a history of rounding behavior are more likely to continue the practice. For example, the probability that a company that has not reported a four in the first post-decimal digit of its EPS for ten years will report a four in any of its next three quarters is only 6.3%. In contrast, a company with a history of reporting at least one four over a ten-year period has a 8.3% chance of reporting a four in its next three quarters, and the difference is statistically significant.

And the companies with cultures of strategic rounding seem to have … related cultural issues:

Companies with high quadrophobia scores are significantly more likely to restate their financial statements, be named as defendants in SEC Accounting and Auditing Enforcement Releases (AAERs), and be involved in class action securities fraud litigation.

I don’t really know what the SEC is looking for in its quest for the missing 4s, or what it will do if it finds them. It is in the nature of sub-penny rounding that the amounts involved are pretty small. (“In 2013, the most recent year in our sample, the mean (median) aggregate amount of earnings over which management would have to exercise discretion in order to move quarterly EPS by a tenth of a cent was $222,000 ($44,000),” report Malenko and Grundfest.) And there is some legitimate discretion in financial accounting. Most of the time, I suspect, moving $44,000 of revenues or expenses from one quarter to another probably isn’t illegal. Fractional-penny optimization of results, mild prettying up of numbers, probably doesn’t quite amounts to fraud.

And yet it is, pleasingly, an identifiable point on a continuum, a purely quantitative way to identify corporate cultures that are, not necessarily fraudulent, but that are at risk of fraud. Some companies pretty up their numbers, some don’t. The ones who do, do it regularly; the ones who don’t, never do it. The ones who do, tend to end up getting in other sorts of accounting trouble; the ones who don’t, tend not to. If you see a company that never reports earnings of 12.4 or 37.4 or 67.4 cents per share, keep an eye on it. The SEC will.

Exit polls.

The basic meta-rule of insider trading is that professional investors are supposed to do research to figure out what will happen and reflect those expectations in asset prices, but they are not supposed to cheat by getting inside information about what will happen. This is not the law, exactly, and we talk endlessly about how the nuances of U.S. insider trading law do not line up with that intuition. But it is a decent enough starting point.

The difficulty, then, is figuring out what sorts of research count as cheating. One obvious one is that if your research consists of calling up the chief executive officer of, say, Apple Inc. and asking “hey how are your iPhone sales this quarter?” and he says “way better than anyone expects,” then that is cheating. (It is not necessarily illegal insider trading under U.S. law, but let us ignore that.) But there are closer questions. What if you call up a big supplier to Apple and say “hey how much screen glass did you sell to Apple this quarter?” Cheating, or legitimate “channel checks”? What if you buy data from a credit-card company and see how many people bought iPhones with their credit cards? Cheating, or legitimate “alternative data”?

In the extreme case, what if you just ask some random people on the street if they bought an iPhone this quarter? It doesn’t seem like cheating. It is not “inside” information. Those people are on the outside. They have no privileged access to sensitive corporate information, no fiduciary duty to anyone to keep their iPhone purchases to themselves. But if you ask enough of them, and pay enough attention to your sampling and questioning techniques, then you might end up with better insight into Apple’s sales than anyone else has. And sure, on the one hand, anyone could do the same. But on the other hand, if you do this right, you are probably mobilizing lots of resources—money, expertise—to do your survey, and it would be hard for the average retail investor to do the same. You might think—I would think—that that is “research,” that it’s using your own resources to add to the information in the market, but others might feel like it’s cheating to have more resources than everyone else.

It seems a bit silly when I say it like that, but in fact paying for access to survey data that no one else has—or before anyone else gets it—is a controversial area of, not necessarily “insider trading” law, but at least of market-unfairness conversation.

Here is an utterly fascinating Bloomberg article on hedge funds’ use of private polling on the U.K.’s Brexit referendum. Basically, while public polls mostly predicted “Remain”—and while the broadcasters who usually publish a joint official exit poll at 10 p.m. on the night of U.K. elections didn’t do that for Brexit, worrying that their model would be too unreliable—several expensive private polls done for hedge funds correctly predicted “Leave,” allowing those funds to make a lot of money with correct bets on the pound. It is not clear to me whether you should care about that basic fact: Doing accurate polling to find out what will happen is probably the sort of informative research that hedge funds ought to be doing. But there is plenty else here—about public figures who went on television to say things that were at odds with private data they had seen, for instance—that might make you more suspicious of the whole thing.

But I want to talk about a weird legal aspect of the story:

Another potential obstacle to hedge fund exit polls may have been more significant: It is a crime in the U.K. to “publish” any exit poll results prior to 10 p.m. Hedge funds wanted data streamed to them throughout the day so their own data experts could track trends, and so they could make bets while people were still voting. But the law broadly defines “publish” as making any data “available to the public at large, or any section of the public, in whatever form and by whatever means” [emphasis added]. ...

YouGov’s chief financial officer spoke to lawyers and decided that a single hedge fund could not be considered “a section of the public” but that multiple hedge funds getting the same exit poll might cross the line. Other polling companies appear to have interpreted the law differently.

Here is an insider trading line-drawing question that I think about a lot. Let’s say you are a person whose job is to call up insiders—at companies, in governments, wherever—and get them to tell you secret information. Then you write down what they tell you and send it to people, who give you (or your employer) money.

If you send the information to a lot of people, and they each give your employer a few tens or hundreds of dollars a year, then traditionally you are called a “journalist,” and what you are doing is called “reporting,” and what you send them is called an “article,” and it is all very very clearly legal. (Your sources might get in trouble for telling you stuff they’re not supposed to, but what you are doing is, in the U.S., protected by the First Amendment.)

If on the other hand you send the information to only a few people, and they each give your employee a few tens or hundreds of thousands of dollars a year, then traditionally you are called an “analyst” or “expert,” and what you are doing is called “ political intelligence” or “expert network work” or something, and what you send them is called a “research report” or just a “tip,” and it is all very plausibly illegal insider trading.

I don’t know how to draw the line between those two things, and it doesn’t seem to me that U.S. law does much to clarify the question. But I can see why you’d want to draw a line. Informing the public—even about secret things, even if “the public” is limited to paying subscribers to a newspaper—seems good and public-spirited and democratic; sure some subscribers might profit from the information, but that is not the main reason that you publish it. Informing only a few wealthy hedge funds about secret things seems greedy and unfair and motivated solely by profit, not by public interest.

But what’s weird is that U.K. law is the opposite! Informing the public about the results of an important referendum is illegal, but giving those results to a hedge fund so it can profit from them might be legal. The lesson here might be that there is no way to get any of this right, that intuitions about insider trading and market cheating and journalism and democracy are hopelessly conflicting.

Index inclusion.

A criticism that you often hear of indexing is that index funds effectively buy high and sell low: The S&P 500 index, for instance, is a periodically adjusted list of 500 big companies, and the way a stock gets added to the index is basically that it becomes big enough. So the S&P is constantly adding companies after they have had good runs, and dropping companies after they have had a poor runs. And because so much money is indexed, incorrect valuations will persist: Index funds are forced to buy overvalued companies, which makes it harder to correct their overvaluations.

I do not want to evaluate these claims, but I will say that if they are correct you should spend less time wringing your hands about them and more time thinking about how to arbitrage them. So this is pretty neat:

The jockeying was evident last month as traders bid up shares of First United Corp. in an effort to push its market value above the $159.2 million threshold for inclusion in the Russell 2000, a popular index of small companies, Ms. Roberts said.

First United’s market capitalization was $132 million on May 9, two days before the deadline to win a spot in the index. Over the next two days, its share price rocketed up 20%. By the time the closing bell rang on May 11, First United’s market value had risen to $159.37 million, making it one of the smallest new entrants to the index.

“There was a lot of interest there in making sure this company made it in,” Ms. Roberts said.

Investors say First United announced stellar first-quarter results on May 9. But professional traders build models designed to predict who will make the cut on deadline day, and the prospect of getting into the Russell had an “accelerating effect” on First United, Ms. Roberts said.

Does indexing make prices less efficient by forcing investors to buy overvalued stocks? I dunno, but if it does, the obvious move is to buy a stock, make it overvalued, and then sell it to an index investor who is forced to buy it. The only bad news is that First United was down 9.5 percent the next trading day (May 14), and is still below where it was on May 11. The strategy of bidding up the price to get it in the index worked, in a sense, but it didn’t make any money.

Don’t read the comments.

Last year we talked a little bit about a comment letter that little Danny Mulson sent to the Securities and Exchange Commission in 2015. “I am a future stock investor, currently in the 8th grade at Aberdeen Middle School in Wetlawn Oregon,” wrote Danny, before praising IEX’s “speed bump” in terms that suggested that he might not in fact be the eighth-grader he purported to be. (Also suggestive: Wetlawn, Ore., does not seem to exist.) In fact it seemed to me that he might be a grown-up with strong views about market structure. A great many regulatory comments are fictitious, but Danny—like his classmate Emma Hibernia, who also had some views on IEX’s application to be a stock exchange—was perhaps an unusually fully developed fictional character for an SEC comment letter. You can just write your comment and sign a fake name to it. You don’t need to give the fake name a back story.

But now Danny is back, older and wiser, with another comment letter to the SEC about the transaction-fee pilot program:

Let me start by apologizing for my tardy response, to your request for comments. My dad has routinely tried to impress upon me the need to meet deadlines. In my defence I have been busy with mid term exams, at Aberdeen High, and only became concerned about this debate in recent days.

Our grade 10 economics teacher, Mr Canton, mentioned your proposed pilot some weeks ago, but it was only when my dad showed me a letter the New York Stock Exchange had sent him - as CFO of a NYSE listed issuer - that I became alarmed about the state of this debate. As a shareholder in that company - my dad recently gave me shares for my 16th birthday - I felt I had to respond.

The letter in question, and the BLOG piece it was linked to, contained a number of assertions that the NYSE knows, or ought to have known, were false. While I am a fan or rigorous two sides debate - and hope to join the Aberdeen Debate Society next year - I am not a fan of obfuscation, dishonesty or other logically trickery to win an argument. Debate should be honest, and engage in with an open mind, aimed at finding the greater truth. Instead the NYSE appears to be presenting indefensible numbers in an attempt to fear monger and protect ill gotten gains. Shame on them.

It goes on in fairly technical terms. For instance:

It assumes that only rebate driven liquidity providers set the quote. But in reality the quote is almost always set by natural investors, who have a view of fair price, that is informed by both fundamental and quantitative research as well as the likely impact of their own short term trading intentions. While some HFT are able to consistently gain top of book, they do so by modeling micro term order book dynamics and predicting quote changes. Removing rebates will not disrupt the desire of natural investors to post liquidity and tighten spreads.

Et cetera. “Things move too fast in this world and we need to slow it down in every way we can,” Danny told the SEC back in eighth grade, but with two years of high-school market-structure education behind him, he is now a lot more sophisticated.

Anyway the NYSE responded to Danny last week. Their response is … surprisingly less technical? But there is this:

Reading your letter, and in light of your commendable interest, we would like to extend an invitation to Mr. Canton’s economics class to visit the NYSE in order to see our institution at work.

What you would witness is a vibrant and prosperous-free enterprise in action, occurring in the open for the world to see.

Let me emphasize this: The New York Stock Exchange has invited an evidently fictional high-school economics class to visit the NYSE floor. (Or, more relevantly, its data center in Mahwah maybe?) This must happen. The thing that I want most in life right now is for a bunch of middle-aged market-structure noodges to show up at NYSE wearing shorts and T-shirts and backpacks, Juuling and asking extremely technical questions about rebate economics while pretending to be 10th-graders. “How do you do, fellow kids, would both sides of the quote really widen by the full 10 mills of rebate reduction?” I will be happy to play “Mr. Canton.” Who is with me? Let’s figure out a date and then I will write back to NYSE, in character, to accept.

Things happen.

Brokerages that do more private placements also have more troubled brokers. Amazon-Berkshire-JPMorgan Health Venture Takes Aim at Middlemen. Commerzbank sets AI to work writing analyst reports. How the Last Commodity Funds Will Survive the Algo Age: ‘Adapt or Die.’ The Biggest Digital Heist in History Isn’t Over Yet. Inside a Heist of American Chip Designs, as China Bids for Tech Power. U.S. Plans Curbs on Chinese Investment, Citing Security Risk. What Would Happen if China Started Selling Off Its Treasury Portfolio? Bank Liquidity Provision and Basel Liquidity Regulations. When Silicon Valley Disrupts the Chicken Coop. Short of Workers, Fast-Food Restaurants Turn to Robots. The World’s First Robot-Made Burger Is About to Hit the Bay Area. Toilet racing. Rat Chews Up Nearly $18,000 and Dies in ATM.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

©2018 Bloomberg L.P.