Forced Stock Sales Haunt China as UBS Sees $68 Billion at Risk

Forced Stock Sales Haunt China as UBS Sees $68 Billion at Risk

(Bloomberg) -- Three years after a wave of forced selling by margin traders fueled a collapse in China’s stock market, a new breed of leveraged shareholders is threatening to trigger another downward spiral.

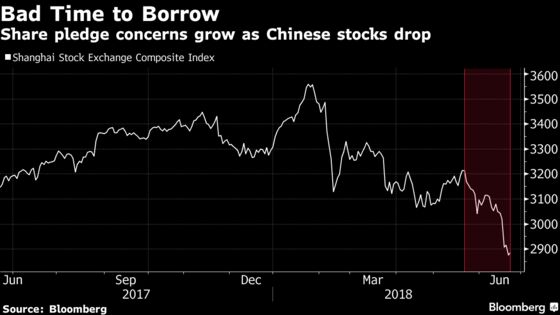

More than 5 trillion yuan ($770 billion) of Chinese shares, or about 12 percent of the country’s market capitalization, have been pledged as collateral for loans, according to data compiled by China Securities Co. and Bloomberg. The pledges, popular among company founders and other major shareholders in need of cash, have become a growing source of concern for analysts and the Chinese government after the Shanghai Composite Index tumbled to within a few points of its first bear market since the aftermath of the 2015 crash.

The worry is that pledged stocks will be liquidated, dragging down prices, if borrowers can’t meet demands for additional collateral. While Chinese regulators told brokerages this week to seek government approval before dumping large chunks of pledged stock, some analysts say the threat of forced sales will continue to hurt the market. UBS Group AG estimates that about $68 billion of shares have dropped to levels below the threshold for liquidation.

“It will remain one of the major overhangs for the stock market in the near term,” Hao Hong, chief strategist at Bocom International Holdings Co., said in an interview from Shanghai.

Few are calling for a 2015-style collapse. But any sign of increased turbulence in China’s $6.7 trillion stock market could unnerve global investors. Their list of worries already includes a trade war, a rout in smaller emerging markets and tighter monetary policy in the U.S. and Europe.

That said, Chinese regulators have plenty of tools to reduce the odds of a cascading selloff. This week’s instructions to brokerages may slow the pace of forced liquidations, while a widely expected cut to banks’ reserve requirements is one of many monetary policy options to boost market sentiment. Authorities have already put caps on the amount of shares that can be pledged in an effort to limit risks.

But that doesn’t mean the market slump won’t get worse. The trade tensions between China and the U.S. are still simmering, and authorities in Beijing have shown little sign of backing down from their campaign to squeeze the $10 trillion shadow banking system. The wealth products offered by shadow lenders have been an important source of funds for both corporate borrowers and the stock market.

Refinacing Risk

In some ways, the share pledges currently worrying analysts can be more problematic during market downturns than the margin debt that roiled shares in 2015.

Most of China’s margin traders take on relatively small debts and are unlikely to face financial ruin if their wagers sour. But shareholders who pledge their stakes for loans tend to do so on a much larger scale, often investing the funds back into their businesses or into other illiquid assets. That can make it difficult to top up collateral when share prices fall, especially for founders who have most of their wealth tied up in their companies. Gaining access to additional sources of financing has grown increasingly tough this year amid the country’s clampdown on shadow banks.

“China’s deleveraging drive will continue to make refinancing harder,” said Sean Hung, a senior analyst at Moody’s Investors Service in Hong Kong. “If a company’s major shareholder has pledged a large amount of shares for funding, it usually suggests the firm’s liquidity conditions are tight and the risks for stock-pledged lending defaults are also higher.”

At least 37 Chinese companies have flagged risks associated with pledging of their shares over the past month, according to stock exchange filings compiled by Bloomberg. Shenzhen Dvision Co., a video communications company, said on Tuesday that pledged stock amounting to 40 percent of its shares outstanding had dropped to a level that may trigger a forced sale. Jiangsu Dewei Advanced Materials Co., which makes materials used in electric cables, said in late May that a 33 percent stake in the company was at risk of liquidation.

Smaller companies are usually the most vulnerable to share pledge-related selloffs because their major stakeholders lack access to ready funding, according to Moody’s.

Changjiang & Jinggong Steel Building (Group) Co., which manufactures agricultural machinery, is among firms that SWS Research Ltd. says face such a risk. The company’s shares -- 37 percent of which were put down as collateral for loans -- have more than halved from their peak last year. Other at-risk companies include Yihua Lifestyle Technology Co., Suning Universal Co. and Sanxiang Impression Co., according to SWS.

Stock Halts

A Yihua Lifestyle official said the company hasn’t been notified of any pledged shares facing liquidation risk, while Sanxiang Impression said it sees no risk of liquidation. The other companies mentioned by SWS didn’t immediately reply to requests for comment.

While Chinese firms have been known to halt trading to buy time with creditors, such suspensions have been subdued during the latest selloff. Halted stocks amounted to about 7 percent of the nation’s listed companies on June 22, versus 6 percent at the end of last year. Nearly half of the market was suspended at one point during the 2015 crash, triggering rebukes from index compiler MSCI Inc. and many international investors.

While it’s anyone’s guess where China’s market heads from here, some analysts have attempted to assess the potential damage from an unwinding of share pledges should stocks continue to fall. Another 10 percent market slump would push about 306 billion yuan of shares below the liquidation threshold, with the figure rising to more than 1 trillion yuan after a 30 percent drop, Essence Securities Co. analysts wrote in a June 18 report.

“There are many latent credit risks if a certain company pledges too many of its shares for loans,” Everbright Securities Co. analysts led by Zhang Xu wrote in a June 20 note. “When the market becomes more volatile, such risks will be exposed at a faster pace.”

To contact Bloomberg News staff for this story: Tian Chen in Hong Kong at tchen259@bloomberg.net;April Ma in Beijing at ama112@bloomberg.net;Amanda Wang in Shanghai at twang234@bloomberg.net;Steven Yang in Beijing at kyang74@bloomberg.net

To contact the editors responsible for this story: Richard Frost at rfrost4@bloomberg.net, Michael Patterson

©2018 Bloomberg L.P.

With assistance from Editorial Board