In a World of Uncertainty, Yield Curves Are Certain

In a World of Uncertainty, Yield Curves Are Certain

(Bloomberg Opinion) -- This week was billed as the most important of the year in terms of the global economy, with the Federal Reserve, European Central Bank and Bank of Japan all meeting to set monetary policy, high level economic data out of the U.S. ranging from inflation to retail sales, the fallout from the disastrous Group of Seven meeting, the U.S.-North Korea summit in Singapore and the looming tariffs on Chinese goods by the Trump administration.

So what did we learn? That despite the back and forth over trade, the obnoxious tweets, the rather kind overtures to North Korea and Russia, and admonitions of our traditional trade partners, the one constant in this sea of uncertainty is the Fed and its overwhelming influence on a flatter yield curve. Without wasting too many words, just know that the Fed delivered another a hawkish mien on Wednesday with Chairman Jerome Powell sounding quite bullish and the central bank basically projecting an interest-rate hike every quarter from now until the 2020 Presidential election.

Although the so-called dot plot was largely irrelevant under Chair Janet Yellen, with her Fed always proving to be overly optimistic about the pace of growth, Powell’s Fed seems more on the mark, especially with the benefit of tax reform and fiscal stimulus, the inflationary pressures from trade policies and an unemployment rate that -- at least optically -- encourages Phillips Curve aficionados.

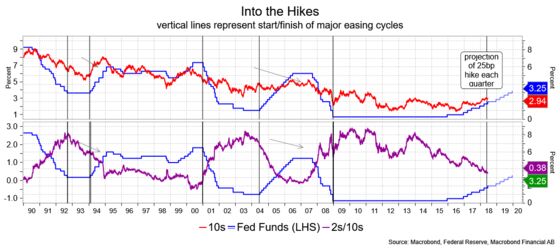

My point is that in a world of grand uncertainties and political volatility, the Fed is reasonably reliable, and its heavy hand in the yield curve provides a high degree of predictable comfort. Tradition has it that a flatter yield curve is a byproduct of what happens when the Fed hikes short-term rates and investors gain confidence that tighter policy will ultimately temper economic growth and contain inflation, making long-term rates relatively attractive. At a recent 37 basis points, the difference between two- and 10-year Treasury note yields is down from 52 basis points at the start of the year and 125 basis points at the start of 2017. The curve is also the narrowest since 2007, which was right after it inverted, with longer-term yields dropping below shorter-term yields just before the financial crisis and recession.

I see no reason why the curve wouldn't be sending a similar message now, in that the Fed’s tightening will ultimately slow the economy and inflation. If, according to the dot plot, the Fed really has 100 basis points of rate hikes in store over the next 12 months, it’s reasonable to expect a perfectly flat curve -- if not a full inversion. Precursor to a recession? Tradition says yes, just in time for the 2020 election.

I am tempted to suggest other markets -- equities? -- are complacent, but I’m not sure that’s accurate. Perhaps investors have become inured to President Donald Trump’s verbosity and invectives and believe they are part of some grand bargaining tactic and should simply be ignored. Or, and I believe this is really the case, investors don’t know how to react and so they look away and carry on. Which is why, with tax breaks in hand, corporate America is doing much more, of the same: stock buybacks and mergers and acquisitions. Perhaps that's why a surge in capital spending and real wage gains remain elusive.

I don’t think it’s easy to dismiss the relentless flattening of the yield curve as a function of dollar illiquidity overseas or differences in rates between the U.S. and elsewhere. Yes, corporate America got its tax break and is using it to keep share prices firm and, with a lack of better capital spending ideas, is buying other firms. Let’s not forget that one reason for acquisitions is the efficiency you get by eliminating redundant roles. This is normal behavior in the latter stages of an economic cycle, and perhaps prudent if there’s a risk that trade policies will prompt retaliation.

This brings me back to the Fed. More rate hikes are a certainty, and with a pace of one every quarter it’s reasonable to see the yield curve at zero if not inverted by this time next year. The direction has been a reliable indicator of things to come and given current circumstances is one of the more secure things to grasp. If we use the term "complacent" in regards to risk markets, we misinterpret the impact of the self-supporting mechanism of buybacks and M&A, enhanced by the tax plan, as being something fundamentally sustaining or bullish for the economy. I think it reflects a lack of better ideas of what to do with the newfound wealth and will run its course. Meanwhile, the curve is the one narrative that I believe most in the market can understand.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

©2018 Bloomberg L.P.