Short-Volatility Bets Boom as Hedge Funds Take Banks' Baton

Short-Volatility Bets Boom as Hedge Funds Take Baton From Banks

(Bloomberg) -- The short-vol trade is dead. Long live the short-vol trade.

Investors are discovering fresh ways to bet volatility across asset classes will tumble anew even as hawkish monetary policy, emerging-market turmoil and February’s vol-mageddon underscore headwinds to the complex trade.

Hedge funds hold the most number of short positions on the Cboe Volatility Index since late January. And they’re now punting on a slew of hot derivatives trades across global equity and debt markets.

An uptick in long volatility premiums is increasing the opportunity to generate yield for fast-money traders taking the other side of the wager, said Mohammad Hassan, analyst at Eurekahedge, a research and data provider. “I don’t think this trade is going away.”

Here’s a tour of the booming world of short-vol strategies, vanilla and exotic.

Pimco Punt

Fast-money traders are harvesting income by betting some of the world’s largest mutual funds will post limited price swings.

High-net-worth individuals are long via structured products they’ve bought from banks that provide one-to-one or leveraged exposure to the likes of Pimco’s $112 billion GIS Income Fund. The capital-guaranteed notes, which banks have sold in droves in recent years, use embedded call options that holders of the notes hope will appreciate as volatility rises.

Banks that have sold the securities are finding buyers, especially hedge funds, to take the other side of the trade, says Jean-Francois Mastrangelo, head of pricing and development in EMEA at Societe Generale SA.

“We mentioned they could sell volatility on those underlyings instead of on the S&P 500 for instance,” Mastrangelo, who helps create and sell derivatives products, said. “They’re interested precisely because they want to diversify their sources of return.”

Swinging Bonds

Money managers are taking advantage of growing nervousness in bond markets to make the contrarian bet that price swings will prove limited. Just as well Wall Street is conjuring up new ways to hedge debt exposures as credit-cycle angst piles up.

It takes two to make a market. Across these products, one party buys the options, making them long volatility. And hedge funds, in exchange for collecting the premium, are often willing to take the other side of the trade.

“For both rates and credit, implied volatility levels are quite low," said Dean Curnutt, CEO of Macro Risk Advisors. "But -- in a similar fashion to the equities side -- the realized levels of volatility are low enough versus the implied to persuade people to come in and sell it," he said.

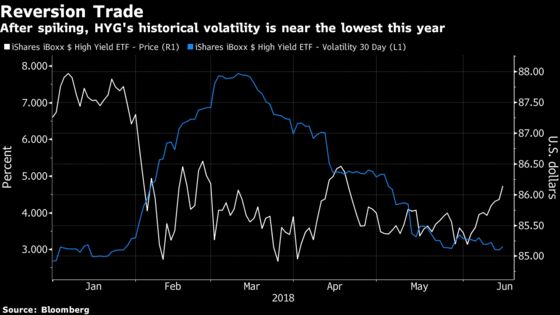

The trade is becoming ever-popular on the $15 billion iShares iBoxx $ High Yield Corporate Bond exchange-traded fund, for example, since its volatility hasn’t moved "too much" in recent years, Curnutt added.

While shorting credit can be profitable, it can backfire in spectacular fashion. The hedge fund set up by former derivatives whizzkid Shahraab Ahmad plunged in the February tumult, Bloomberg reported, after he was said to have sold put options on junk derivatives, leading to a margin call.

Dispersion Dive

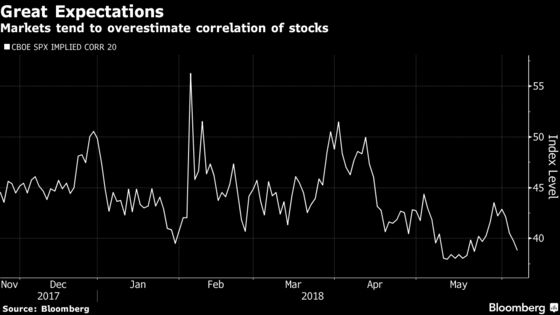

Some hedge funds are also snubbing the vanilla trade of selling S&P 500 volatility in favor of combining their volatility bets with another technical measure: correlation.

By going short correlation, they’re betting stock prices will diverge from each other. For some, it’s a technical play. For others, it may be a bet the stock bull run has legs, with few macro headwinds that would increase correlations.

The strategy, also known as a dispersion trade, works like this: Options are bought or sold on an index, as well as on individual equities within the gauge. The bet is on whether the shares will move together, boosting the volatility of the index, or whether they’ll move apart -- canceling each other out. The latter tends to reduce the movement of the index overall.

In April, hedge fund Capstone Investments Advisors was said to have hired former Pacific Investment Management Co. money manager Jason Goldberg to run a dispersion trading strategy at the $6 billion fund.

Markets tend to overestimate the degree to which shares will move together -- the implied correlation -- which is why shorting the measure can generate profits.

Demand for shorting comes once again from the structured-product market, according to SocGen’s Mastrangelo. Banks sell notes tied to multiple stocks that leave the holders of such securities implicitly long correlation. That gives banks the short leg, which they offer to hedge funds as a source of returns, he said.

“It still has a good return if you know how to pick your stocks,” said Mastrangelo.

--With assistance from Dani Burger.

To contact the reporter on this story: Yakob Peterseil in London at ypeterseil@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma, Natasha Doff

©2018 Bloomberg L.P.