Hedge Funds Pick the Wrong Time to Go Big on Gold as Prices Drop

Geopolitical risks that previously supported prices are fading after President Donald Trump met with Kim Jong Un.

.jpg?auto=format%2Ccompress&w=200)

(Bloomberg) -- Hedge funds just mistimed their gold bets.

Money managers as of Tuesday pushed their wagers on a bullion rally to the highest in seven weeks. The next day, Federal Reserve policy makers signaled more interest-rate increases this year than earlier projected. Gold ended up posting a weekly loss as the dollar rallied.

Bullion has been stuck in the doldrums for most of this year as the outlook for higher borrowing costs dimmed prospects for the metal, which doesn’t pay interest. Even rising trade tensions between the U.S. and China that sent equities and bond yields tumbling Friday weren’t enough to boost gold’s haven appeal as the metal fell the most in 18 months. Geopolitical risks that previously supported prices are also fading after President Donald Trump met with North Korean leader Kim Jong Un.

“We have been cautious about gold just because we still see a stronger dollar and the Fed raising rates as headwinds,” said Rob Haworth, a Seattle-based senior investment strategist at U.S. Bank Wealth Management, which oversees $154 billion.

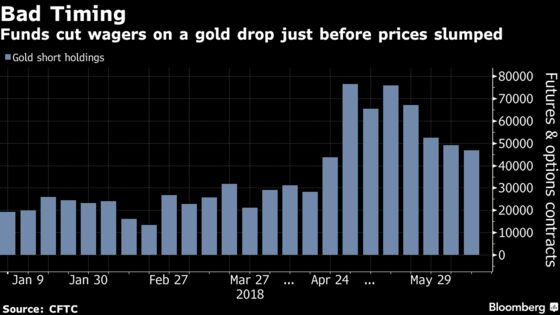

Fund Wagers

In the week ended June 12, money managers boosted their net-long position, or the difference between bets on a price increase and wagers on a decline, by 11 percent to 64,572 futures and options, according to U.S. Commodity Futures Trading Commission data released Friday.

Long-only wagers climbed 3.9 percent. The short holdings fell 4.7 percent in a fourth straight decline, the longest slide since September.

Gold for August delivery slid 1.9 percent in the week ended Friday to $1,278.50 an ounce on the Comex, the second decline in three weeks. Prices rebounded Monday, rising 0.3 percent to $1,282.90 an ounce at 9:55 a.m. in New York.

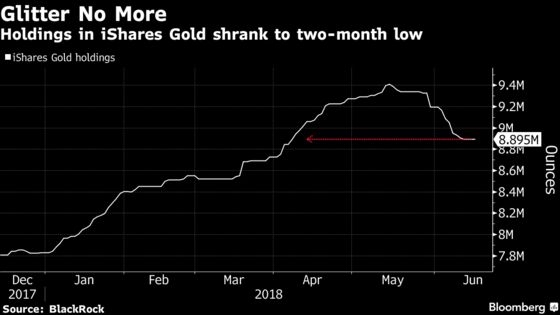

Some of metal’s most loyal investors have been in exchange-traded funds, but there are signs that they’re starting to throw in the towel. Holdings in iShares Gold Trust, the second-largest bullion-backed ETF, shrank by about half a million ounces in the past five weeks. That’s a stark reversal in sentiment seen just a month ago, when assets in the fund climbed a record, even as prices of the metal were tumbling.

Hedge Funds Jump Into Silver Before Tariffs Tarnish Metal: Chart

There are also signs that physical demand is slowing. India’s imports in May shrank by 39 percent from a year earlier to 77.6 metric tons, according to a person familiar with the information. That’s the the fifth month of decline as the world’s second-largest gold buyer enters a seasonally weak period for purchases.

More Inflation

Still, accelerating U.S. inflation is one reason to remain optimistic on the metal’s the outlook, according to Sprott Inc., the Toronto-based money manager that focuses on precious metals. Bullion has been used by some investors as a hedge against rising prices. The consumer price index climbed 2.8 percent in May from a year earlier, the fastest pace in six years, according to a Labor Department report released Tuesday.

A brewing trade war between China and U.S. may eventually mean more gains for inflation, too, said Shree Kargutkar, a portfolio manager at Sprott, which oversees 11 billion Canadian dollars ($8.3 billion).

For gold, “the short-term moves that we’re seeing right now are just a knee-jerk reaction,” Kargutkar said. “What really helps drive gold is when inflation is running hotter than the nominal interest rates environment. Inflation expectations over the longer-term will likely be strengthened.”

To contact the reporter on this story: Luzi Ann Javier in New York at ljavier@bloomberg.net

To contact the editors responsible for this story: James Attwood at jattwood3@bloomberg.net, Millie Munshi, Joe Richter

©2018 Bloomberg L.P.