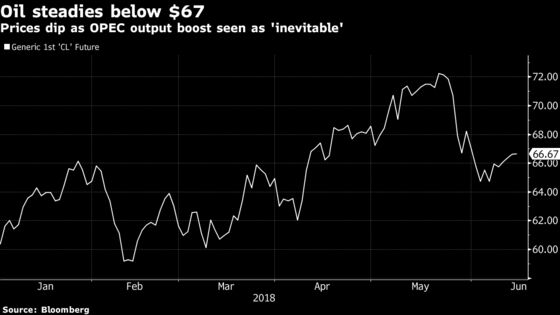

Oil Closes Below $67 as Saudis Predict `Inevitable' Supply Rise

Oil steadied just below $67 a barrel as Saudi Arabia and Russia discuss OPEC pact.

(Bloomberg) -- Crude rose for a fourth consecutive day as a halting of oil loading from two key ports in Libya offset concerns about a phase-out of supply limits by OPEC and allied producers.

Futures settled 0.5 percent higher in New York, after slipping as much as 0.4 percent. Saudi Energy Minister Khalid Al-Falih said an output rise would be “inevitable” but in a way that “satisfies most importantly the market.” His Russian counterpart Alexander Novak said the increase should begin gradually on July 1.

The Organization of Petroleum Exporting Countries and allied producers will meet at the end of next week in Vienna to discuss the fate of historic production constraints that tamed a worldwide glut. The Saudi and Russian plan to relax the limits faces opposition from Iraq, Iran and Venezuela, even as U.S. President Donald Trump chides the cartel for boosting prices.

Between now and the OPEC-led gathering on June 22, “oil will be completely headline driven,” said Bob Yawger, director of futures at Mizuho Securities USA Inc. in New York. “That’s because this is the first meeting we’ve had in two years where the production curbs are in danger of coming undone.”

Meanwhile, two of Libya’s biggest oil ports stopped loading crude after armed forces clashed nearby, disrupting about 240,000 barrels of daily oil shipments.

West Texas Intermediate crude for July delivery rose 25 cents to settle at $66.89 a barrel on the New York Mercantile Exchange. Total volume traded Thursday was about 13 percent below the 100-day average.

Brent futures for August settlement slid 80 cents to $75.94 on the London-based ICE Futures Europe exchange. The global benchmark crude traded at a $9.25 premium to WTI for the same month.

Crude rallied to a three-year high in May, and subsequently lost steam as Saudi and Russian enthusiasm for the supply curbs waned. The International Energy Agency said Iran and Venezuela could lose almost 30 percent of their output by the end of next year due to U.S. sanctions and economic upheaval, requiring extra supplies from OPEC’s Gulf members.

In the U.S., government data showed crude stockpiles declined by 4.14 million barrels last week, steeper than estimated by analysts in a Bloomberg survey. Gasoline and distillates also slid last week, the Energy Information Administration said.

Other oil-market news:

- Gasoline futures dropped 1.6 percent to $2.091 a gallon, after gaining 1.7 percent on Wednesday.

- Stricter maritime fuel regulations may spur a $5- to $10-a-barrel increase in crude prices, according to Sanford C. Bernstein & Co. analysts including David Vernon.

--With assistance from Tsuyoshi Inajima and Heesu Lee.

To contact the reporters on this story: Catherine Ngai in New York at cngai16@bloomberg.net;Grant Smith in London at gsmith52@bloomberg.net

To contact the editors responsible for this story: Reg Gale at rgale5@bloomberg.net, David Marino, Joe Carroll

©2018 Bloomberg L.P.