Hedge Funds' Best Ideas? Those Are Just Stocks They're Dumping

Hedge Funds' Best Ideas? Those Are Just Stocks They're Dumping

(Bloomberg) -- Ever wonder why hedge fund managers are so willing to get up on a stage and tell the world about their best ideas? A new study suggests an answer: the ideas are getting old, and they need a spot to sell.

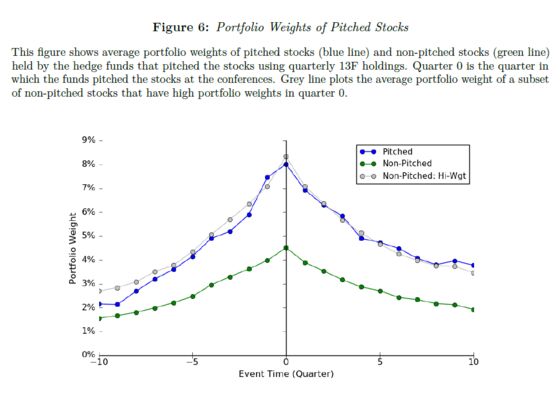

The research pertains to what is by now a familiar ritual. A few times a year, famous investors crowd a conference hall somewhere and publicly discuss the companies they like. What they leave out is that starting roughly then, they’re much more apt to sell the stock than load up on more.

Not that it’s a crime against humanity, exactly. Propelled by the buzz, pitched stocks tend to keep on rising after being mentioned on stage, sometimes for months, according to Patrick Luo, the Harvard doctoral student who published the study. But it does answer a question that has occasionally vexed outsiders: if the ideas are so good, why tell anyone?

“Hedge funds take advantage of the publicity of these conferences and strategically release their book information to drive market demand,” Luo wrote in a new study. “Specifically, hedge funds sell pitched stocks after the conferences to take profit and create room for better investment opportunities.”

On average, a hedge fund manager that pitches a stock at a conference cuts its weighting in his portfolio within the first quarter after praising it. Luo looked at nearly 30 investment conferences from 2008 to 2013, creating a sample of nearly 350 long and 40 short stock pitches.

One thing is clear from the work, the mentions matter. Luo estimated that investors can earn 1 percent in the first two days after a pitch by running with the advice while simultaneously selling the market. It’s testament to just how closely watched these conferences are.

The paper, Talking Your Book: Evidence from Stock Pitches at Investment Conferences, found that pitched stocks outperform the broader market before and after hedge fund managers announce their best ideas, and that hedge funds have no outstretched attachment to the names on average.

“This suggests that the pitched stocks were their ‘best ideas’ but not likely any longer,” Luo wrote. “Returns of pitched stocks diverged from market immediately after the pitches—long pitches spike up and short pitches spike down. These results suggest that these investment conferences are closely followed by other investors and have high market impacts.”

Pitched stocks also tend beat other stocks that hedge funds hold but that don’t get name-checked in an on-stage presentation. Most of the outsized returns occur before the pitches, though, while the post-conference boost is likely driven by copy-cat bets from investors following the ideas, according to Luo.

“The majority of the outperformance occurs before the pitches,” he wrote. “Outperformance after the pitches are likely driven by inflows from other investors that follow these investment conferences.”

To contact the reporter on this story: Sarah Ponczek in New York at sponczek2@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2018 Bloomberg L.P.