Puerto Rico's Sales-Tax Bonds Soar on Optimism About Deal

Puerto Rico Cofina Investors Get Half Sales Tax in Proposed Deal

(Bloomberg) -- Puerto Rico sales-tax-backed bonds rallied after a tentative agreement struck in the island’s bankruptcy promised to steer a large share of that revenue to owners of the securities, leaving them facing smaller losses than investors previously anticipated.

The details of the pact between two court-appointed agents, disclosed in a filing late Thursday, show that owners of the bonds would get just over half of the future sales-tax revenue they’re currently entitled to each year. They would also get all of the $1.2 billion of revenue that’s been frozen in a reserve account until the bankruptcy court decides who has a right to the money.

The deal, if ultimately approved, would resolve a key dispute in the island’s record-setting bankruptcy, where creditors have been fighting over who has the highest claim on the government’s tax collections. The arrangement could leave owners of the most senior sales-tax bonds, known as Cofinas, paid in full. That’s a better settlement than one floated a few weeks ago, according to a person familiar with the matter.

“Seniors are in good shape because they get the money first,” said Daniel Solender, head of municipal investments at Lord Abbett & Co., which manages $20 billion of state and local debt, including Puerto Rico securities. “With more than half the money going to the Cofina side, the seniors may be fully covered.”

Governor Ricardo Rossello declined to comment because he said a final agreement hasn’t been reached and talks are ongoing. "We want the government to continue being part of that negotiation," he told reporters in San Juan. "For the benefit of the people of Puerto Rico, I prefer not to comment on the details of the negotiation."

Spokespeople for a group of general-obligation bondholders and a pool of senior sales-tax investors declined to comment on the details of the tentative settlement.

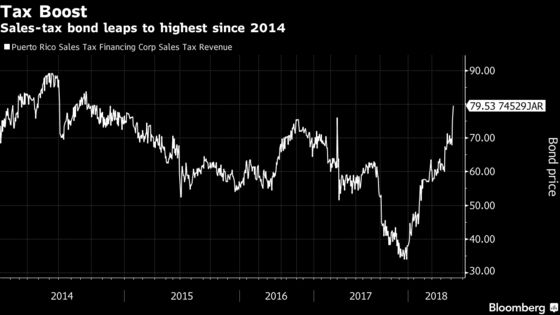

The bonds climbed on the details, pushing up the price of senior sales-tax securities due in 2040 by nearly 10 percent to an average of 83 cents on the dollar. Subordinated debt maturing in 2041 climbed 13 percent to 41.8 cents. The prices of the island’s general-obligation bonds were little changed.

Puerto Rico’s debt payments have been on hold as it works through bankruptcy. There’s about $780 million that’s originally earmarked to repay Cofinas in fiscal 2019. The potential settlement would give Cofina more than half of that amount, with the government receiving the rest to repay commonwealth creditors and cover essential services, according to the court documents.

“On the commonwealth side, it’s not clear what goes to bondholders and what goes to everything else,” Solender said. “Nothing specifically has changed for bondholders on the G.O. side, at this point.”

The agents for Puerto Rico and Cofina, the Puerto Rico government-owned corporation that issued the bonds, have asked U.S. District Court Judge Laura Taylor Swain to hold off on ruling on the issue for 60 days as they work out the final details.

The rally since the tentative agreement was announced Wednesday has delivered large gains to investors who’ve held on to their bonds even as they plummeted in the wake of Hurricane Maria. The price of the subordinate Cofinas Friday is more than five times what they traded for in November, when they touched a record low of 8.2 cents on the dollar.

“It’s better than Internet stocks,” Solender, whose firm holds senior and subordinate Cofinas, general obligations and debt sold by the island’s bankrupt public power utility.

Major Hurdle

Resolving the issue of the sales-tax revenue is a major hurdle in Puerto Rico’s bankruptcy because it’s essential to determining how much Cofina and general-obligation bondholders will recover. Those two classes of securities account for about $35 billion of the more than $70 billion that the commonwealth owes. Swain called the deal announcement “an enormously significant development” during a hearing Wednesday in San Juan.

As part of the settlement, Cofina would receive all of the money held by Bank of New York Mellon Corp., its trustee, as of June 30, 2018. There was nearly $1.2 billion in that account as of May 1, according to disclosure filings posted on Municipal Securities Rulemaking Board’s website.

Starting July 1, Cofina would also get 53.7 percent of the sales-tax receipts that are dedicated to repaying the bonds, growing by 4 percent annually to a maximum of $1.85 billion by 2041. The dedicated revenue totals $783.2 million for fiscal 2019, which starts July 1.

Overdue Payments

While Puerto Rico continues to direct sales-tax revenue to the trustee, Cofina bondholders stopped receiving payments in June 2017. They’re owed about $550 million of principal and interest in fiscal 2018, which ends June 30, according to disclosure filings.

Once Cofina receives its full 53.7 percent allocation of the revenue, Puerto Rico will get the rest. Those monies will be placed in escrow and used to resolve claims against the commonwealth, though the island has the ability to use the cash for essential services after its liquidity is exhausted, according to the court filing. A federal board that oversees Puerto Rico’s finances will determine which services are essential.

--With assistance from Steven Church.

To contact the reporter on this story: Michelle Kaske in New York at mkaske@bloomberg.net

To contact the editors responsible for this story: James Crombie at jcrombie8@bloomberg.net, William Selway, Christopher Maloney

©2018 Bloomberg L.P.