Bubble-Like Stock Valuations Miss $3.4 Trillion in Hidden Assets

With its sky-high valuation, Autodesk would appear to be a poster child for froth amid a nine-year bull run.

(Bloomberg) -- On paper, Autodesk Inc. is a bit of a mess. It’s been losing money for almost three years, and its book value -- what’s left if you sell off the assets and repay debt -- is negative. Yet over the past year, the stock has gained 23 percent, almost double the S&P 500.

With its sky-high valuation, the software maker would appear to be a poster child for froth amid a nine-year bull run. But to some, it should be seen in a very different light -- as a company whose fundamentals are made to look a lot worse than they are by old, and increasingly useless, accounting rules.

“You get numbers which are highly inflated for some companies, and are understated for other companies,” says Baruch Lev, the New York University finance professor whose 2017 paper on the topic ignited a debate about valuation. “It doesn’t make any sense.”

That talk rankles the old school, which hears it as an apologia for stock prices that seem to be bubbling over. But lumping it with dot-com-era gimmicks like price-to-eyeballs misses a larger point tied to the growing role of services in developed countries. As the economy changes, proponents say, accounting standards that made sense for shipbuilders and oil drillers are bound to lose relevance.

And it’s not just talk. Practitioners now regularly adjust models to give greater heft to things that were previously thought too abstract to value. By treating specific kinds of intangibles -- those funded internally, that solidify a strategic advantage -- as investments, fund manager Knowledge Leaders Capital LLC says it sees $3.4 trillion extra book value on the balance sheets of the roughly 3,000 stocks it studies, causing the price-to-book ratio to fall by 14 percent.

After the adjustments, Autodesk has $7.8 billion of assets, compared with the $4.2 billion on the books in the same period. Its 2018 losses are 21 percent smaller than reported.

It’s a hallmark of American accounting that the value created by things like advertising or research and development go largely unrecognized when counting up net worth, while eating into earnings.

Here’s how it works. When a company splurges on developing software, accounting treats it like renting office space: you’re spending money to keep the business going, but not acquiring anything with future benefits. If you buy a building, however, that becomes an asset on the balance sheet, its cost spread over a long time.

Not recognizing intangible assets can push down both profits and book value in businesses that depend on research and marketing, which are increasingly important in the global knowledge economy. Just think Tesla Inc., Nike Inc. or Gilead Sciences Inc.

“You’ve got all these assets that don’t show any value in their financial statements that are just becoming more and more valuable in today’s society,” said Travis Fairchild, a fund manager at O’Shaughnessy Asset Management in Stamford, Connecticut. “We’ve moved from an industrial marketplace to much more of a technology and intangible asset industry, and that’s just creating larger and larger distortions.”

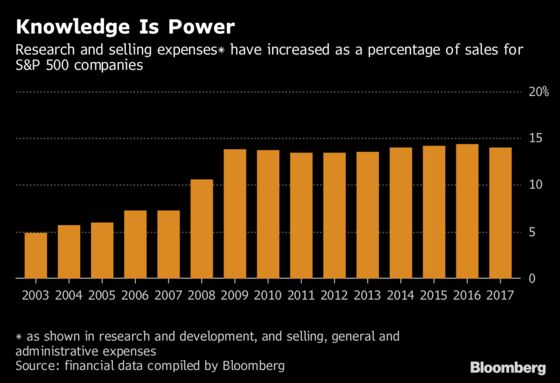

Intangible investments -- everything from employee expertise to customer data -- are on the rise. Spending on research and sales as a percentage of revenue rose to 14 percent in 2017 for S&P 500 stocks, compared with 7 percent a decade ago, data compiled by Bloomberg show.

Yet under accounting rules in place since the 1970s, intangibles are expensed rather than capitalized -- unless they were acquired. There are also minor exceptions, such as costs of developing a software that’s ready to be sold.

This matters for metrics used to determine if a stock is cheap or pricey, such as price-to-book or price-earnings, which are often used to compile indexes tracking investment styles such as value. Fairchild believes unreliable book values mean some companies classified as growth stocks are actually value stocks. For investors, the question is whether it’s worth tweaking the measures at the risk of introducing subjectivity into cold, hard numbers.

Some fund managers are already making the move. OSAM is developing a proprietary book value factor that would take into account intangibles. State Street Global Advisors’ models adjust for them, according to Olivia Engel, chief investment officer of active quantitative equities at the firm.

“In the world of today, we need to customize sector by sector the most useful multiple given the difference in accounting and, of course, the intangible side, which has changed a lot,” said Angelo Meda, Milan-based head of equities at value investor Banor SIM SpA. “What was useful in the past now is a little bit more complicated.”

But with global stocks just a few months off a historic high, there’s the risk that adjusting for intangibles, which are especially hard to value, becomes an excuse to justify buying pricey tech shares. Book values also remain useful for some sectors, such as financials or industrials, Meda added.

“Investors need to be quite conservative not to try to be too cute or too creative in trying to value each individual company in a way that supports their idiosyncratic thinking,” said Vitali Kalesnik, London-based head of equity research at Research Affiliates LLC, which pioneered smart-beta investing.

One of the effects of the rise of intangibles is that companies with negative book value, traditionally a red flag for investors, have become more common. There are now 187 stocks worldwide with negative net assets and a market value of at least half a billion dollars -- with an average return of 27 percent in the past year -- compared with 90 a decade ago, data compiled by Bloomberg show. The list includes McDonald’s Corp., GlaxoSmithKline Plc and Lockheed Martin Corp.

To NYU’s Lev, the rise of intangibles means the focus on earnings is pointless. In his 2017 paper, he argued that predicting earnings don’t produce investment gains because they no longer represent value creation. He points to the example of Kite Pharma Inc., which had posted a loss every quarter since its public debut when Gilead Sciences Inc. bought it for $12 billion last year. What was Gilead after? Kite’s cancer therapies.

“Investors are becoming much smarter -- some, at least -- and they are desperately looking for some information in those intangibles,” he said. “You capitalize, you amortize, and you have an income statement that says something, unlike today.”

--With assistance from Ksenia Galouchko.

To contact the reporter on this story: Justina Lee in London at jlee1489@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Chris Nagi, Jeremy Herron

©2018 Bloomberg L.P.