Hated by Many, Distressed Debt Brawler Isn't About to Back Down

Hated by Many, Distressed Debt Brawler Isn't About to Back Down

(Bloomberg) -- Mark Brodsky knows the nasty things the haters say about him. Things like he’s a bully. An extortionist. A hedge-fund vulture.

But suggest that he’s litigious, and his eyes widen.

“If anyone calls us litigious, it’s name-calling,” says the lawyer-turned-distressed debt investor, who has spent two decades suing cash-strapped corporations and, on one occasion, an entire country over unpaid debts.

But Wall Street isn’t about sticks and stones. It’s about money.

And in a business with no shortage of sharp elbows, Brodsky has some of the sharpest -- and he’s pretty good with them, too. Using novel legal theories and targeting gray areas in the law, he honed his investing approach in distressed debt working for a master, Elliott Management’s Paul Singer, and then took it to new heights at his own $3.4 billion firm, Aurelius Capital Management.

Critics don’t mince words.

“I started fighting tooth and nail with Mr. Brodsky when that self-absorbed jerk began his career working for Paul Singer,” says William Brandt, who once butted heads with Brodsky as a trustee in a bankruptcy case. Brandt “firmly believes” he’s made his career on intimidation.

Weaponizing Law

The nicest words Brandt can muster: “Many think of Aurelius as a suppository for the distressed industry.”

Brodsky, told of the barb, says he doesn’t know what to make of it.

Others have accused his New York-based firm of trying to “weaponize” bankruptcy law and to “extort value” from its financial positions. During an ugly, drawn-out legal battle against Argentina, Aurelius and Elliott were called financial terrorists by its president. And more recently, in Puerto Rico’s debt crisis, U.S. Senator Bernie Sanders lambasted hedge-fund creditors like Aurelius for being “morally reprehensible.”

“Mark can be a formidable opponent -- I’d rather be in the trenches with him than on the other side,” said Jay Newman, a former money manager at Elliott who brought on Brodsky to work at the firm. “His tenacity is never mindless, it’s based on hard work.”

Love them or hate them, distressed debt investors, who buy up assets of troubled companies, have always helped make the markets go ’round. Brodsky, 64, says operations like Aurelius “do a lot of constructive things” and get a bad rap for pushing borrowers to reorganize and restructure.

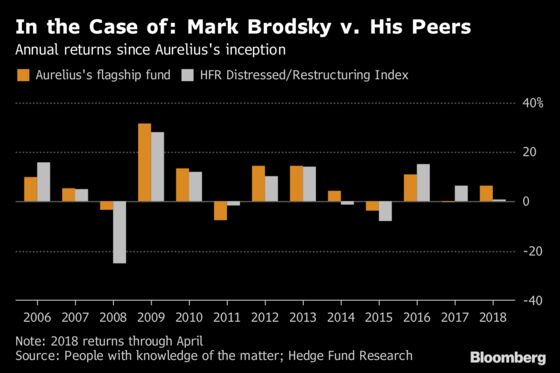

The strategy has generally worked out pretty well for Aurelius’s clients. Since the firm’s inception in 2006, its flagship fund has generated annualized returns of 7.4 percent, versus 4.9 percent for your average distressed debt fund. This year, Aurelius has made 6.5 percent through April, compared with a 1 percent gain for its peers.

Brodsky works hard to avoid the limelight. He refuses to be photographed or discuss his personal life. Search for a picture of him online, and you’ll find instead ones of Sam Zell, the real estate magnate known as the Grave Dancer -- a happenstance Brodsky’s in no particular rush to correct.

Leaning back in his chair in his midtown Manhattan office, Brodsky hardly comes across like a financial brawler.

A trim, bespectacled man with a high forehead and silvery hair, he speaks in lawyerly sub-clauses and methodical play-by-plays. He offers visitors a water glass engraved midway up with a slogan he says explains how debt investors see the world: “Pessimist’s Glass: This glass is now half empty.”

Brodsky wants to get something straight. He scoffs at the idea other hedge funds are afraid to go up against Aurelius, named after his intellectual idol, the Roman philosopher-emperor Marcus Aurelius. A bobble-head doll of the old stoic sits atop his desk.

Fear and Loathing

“I wish we could just show up, wave a flag, and everybody caves!” he says with a rare laugh.

Yet over the years, he’s developed a reputation for being a ruthless and indefatigable opponent who’s willing to make big, bold bets in distressed debt. Brodsky has a formidable track record pursuing “litigation plays,” and taking on the likes of General Motors, Argentina and Puerto Rico in court. And while historically low defaults have led others in the industry, like Singer himself, to branch out, Brodsky has stuck to what he knows best. He says he knows his limits and avoids “boredom trades” that tend to get others into trouble.

Brodsky never intended to become one of the most-feared distressed debt investors on Wall Street. A Harvard-trained lawyer, he says his first stint in finance -- at Dickstein Partners, a distressed debt hedge fund that later shuttered -- left a bad taste in his mouth. The trade-by-the-seat-of-your-pants ethos clashed with his methodical, analytical nature.

Then in 1996, he joined Elliott. Brodsky said he valued the mathematical approach of Singer’s firm, which specialized in a deep-research style of investing. It was also where he made his first profitable trade: in the distressed debt of Southeast Banking Corp., a bankrupt Miami-based bank.

History Lesson

To hear Brodsky tell it, he combed through reams of documents from a Freedom of Information Act request (made in the days before it was an easy, routine thing on the Internet) and discovered the bank was actually solvent.

The problem was the trustee -- the aforementioned William Brandt -- who was just “sitting on the cash.” When Brandt refused to distribute it to creditors, Brodsky successfully had the court replace him and the money disbursed.

“The trustee didn’t like me,” he said.

Brandt recalls it differently. He says he subpoenaed Brodsky for the documents and asked the court to sanction him for failing to produce them. Brandt believes Brodsky pursued his own interests at the expense of other creditors. Whatever the case, Elliott got what it wanted, and Brodsky would end up spending almost a decade there working under Singer.

“Having someone as capable as Paul above you -- there was a real safety net in that,” Brodsky said, “It was arguably insane to leave.”

Intellectual Idol

In 2006, he decided to set off on his own. Brodsky scraped together $330 million for his firm and settled on the Aurelius name after spotting a new translation of the stoic’s “Meditations” at a local bookstore. He says he was struck by how the all-powerful emperor believed that “no matter who you are, you have to act honorably.”

“It was a splendid metaphor for how I wanted to be seen on Wall Street.”

But ask his critics, and they’ll say those high-minded ideals didn’t always necessarily extend to those in his crosshairs. In Argentina, one of Brodsky’s biggest wins, Aurelius drew the ire of an entire nation. The decade-long legal battle got ugly at times, with holdout creditors going so far as to seize an Argentine naval ship in Ghana to pressure the country into paying what it owed. The government in turn created video games and cartoons to teach children about the dangers of vulture investors.

Of course, Singer got most of the press, but Brodsky made his mark as an astute and resourceful operator among Wall Street insiders. Back-of-the-envelope math puts Brodsky’s returns on the investment, which people familiar with the matter say he built between 2007 and 2010, at about 700 percent, based on the bonds’ average price over that period.

Awkward Conversations

“Mark is never just along for the ride,” said Newman, who was Elliott’s point man on Argentina and retired shortly after the country settled with the hedge funds in 2016. “He always thinks things through, does his own homework.”

Jon Harari, an Aurelius alum, says Brodsky’s intensely cerebral nature made conversations less than easy. Harari recalls “spending hours thinking of how to say a certain thing” because Brodsky wanted people to quickly boil things down to their most salient points, regardless of how complex. Brodsky, it seemed, was always 10 steps ahead anyway.

That’s not to suggest Brodsky is afraid to speak his mind. Over the years, he’s developed a penchant for firing off cutting and sarcastic missives, excoriating those who don’t see it his way.

Hardball Tactics

In 2015, Brodsky compared Axel Kicillof, Argentina’s economy minister at the time, to Nero fiddling while Rome burned. A year later, he wrote to an administrator of Brazilian phone carrier Oi SA, “Respectfully, we believe you are utterly failing to discharge your most fundamental responsibilities...you have come up with one bewildering excuse after another to procrastinate.”

He’s shown a talent for playing hardball at the negotiating table, too.

During talks with GM, lawyers for its Canada unit claimed the subsidiary had little value and threatened to file for bankruptcy, leaving hedge-fund creditors with nothing. Brodsky called their bluff, brazenly throwing his wallet on the table and offering to buy the unit for whatever was in the wallet, according to court testimony. Then, by leveraging an obscure provision in Nova Scotia law, the hedge-fund group ultimately walked away with a settlement worth almost twice the returns of other creditors.

Bruce Zirinsky, a lawyer who represented Aurelius in GM and other cases, calls Brodsky “one of the brightest and nicest people in the business.” Others, he says, are just “lemmings.”

Standing His Ground

Nevertheless, as Aurelius’s profile has grown, so has scrutiny of its tactics.

In 2016, a judge said demands made by a group of creditors in Sabine Oil & Gas, which included Aurelius, had taken an “enormous toll,” citing a long trial over a claim that was eventually shown to be fruitless. Oi’s bankruptcy judge ruled that Aurelius tried to “weaponize” the law. (The judge ultimately said the firm hadn’t “demonstrated bad faith.”)

Brodsky, who counts pension funds and foundations among his firm’s investors, stands by his positions, however unpopular. It’s a matter of doing your homework and picking the right battles.

Brodsky sympathizes with the local population -- to a point. He believes the lasting effects of the hurricane will be “modest.” Bondholders, rather than being the problem, are part of the solution to Puerto Rico’s financial mess. If anything, Aurelius’s interests are more aligned with the territory’s people than other involved parties -- like the government and local officials, he said.

Asked if he thinks his legal claims on the U.S. territory’s debt are worth fighting for when it pits him against people struggling to get back on their feet, Brodsky says the thought hasn’t occurred to him.

“I’m paid to make money for my investors,” he says, “not lose it.”

To contact the reporters on this story: Tiffany Kary in New York at tkary@bloomberg.net;Katia Porzecanski in New York at kporzecansk1@bloomberg.net;Sridhar Natarajan in New York at snatarajan15@bloomberg.net

To contact the editors responsible for this story: David Gillen at dgillen3@bloomberg.net, Michael Tsang, Nikolaj Gammeltoft

©2018 Bloomberg L.P.