It’s 2007 Again for Commercial Mortgage Bonds, Moody’s Says

Securities are backed by as many interest-only mortgages as they were in late 2006 and early 2007, Moody’s said.

(Bloomberg) -- Commercial mortgage bonds are getting stuffed with the lowest-quality loans since the financial crisis by one measure, according to Moody’s Investors Service, a warning sign that the $517 billion market may be headed for harder times.

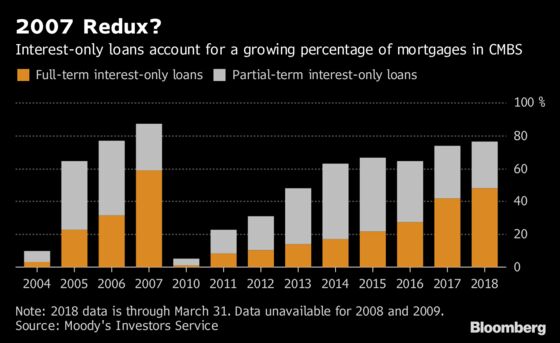

The securities are backed by as many interest-only mortgages as they were in late 2006 and early 2007, Moody’s said. Those loans are riskier because borrowers don’t pay any principal early in the debt’s life. When that period expires, the property owners are on the hook for much higher payments.

The percentage of interest-only loans in a commercial mortgage bond is an "important bellwether" for the industry, according to Moody’s analysts, because the loans are more likely to default and to bring bigger losses to lenders when they do. Underwriters aren’t taking steps to fully offset the rising risks, the ratings firm said.

The riskier debt getting packaged into commercial mortgage bonds mirrors a trend that’s infiltrated many corners of the credit markets, from leveraged loans to residential mortgage securities: As investors have flocked to debt investments that seem safe, underwriters have been emboldened to make the instruments riskier and keep yields relatively high by removing or watering down protections.

Moody’s said fierce competition in lending has allowed "the vast majority" of borrowers with good properties to get the loosest kind of interest-only loans, and even debt tied to "lower-quality properties in secondary markets" now often has the borrower-friendly terms.

The growing percentage of interest-only loans is "a significant negative credit trend, as well as an important warning sign of deteriorating underwriting standards," analysts led by Kevin Fagan wrote in a note this week.

In the first three months of the year, more than 75 percent of loans in commercial mortgage bonds with multiple borrowers were interest-only, the highest share since late 2006. On average, a borrower can wait nearly six years before paying principal, up from 2.2 years four years ago. Almost half of the pools of loans backing bonds included "full-term" interest-only debt, which doesn’t require principal payments until the full loan is due.

Offsetting Risk?

Underwriters usually try to offset the risks posed by interest-only loans by including higher-quality properties, lowering the amount of debt on properties or limiting full-term interest-only debt in securities. But these protections haven’t been enough to cancel out the hazards, the analysts said.

In another worrying sign, loans in commercial mortgage bonds have growing exposures to a single tenant or small group of renters. During an economic downturn, that’s particularly risky because the departure of one tenant can wipe out a borrower’s ability to keep paying required interest and principal.

To compensate for deteriorating loan quality, Moody’s has boosted the amount of investor protections, called credit enhancements, that deals must include to win Aaa and other investment-grade ratings. And analysts expect the loosening standards may continue.

"It adds a substantial amount of risk to our pools," Fagan said in an interview. "We adjust for it and we get noisy about it but it doesn’t necessarily slow the trend down."

To contact the reporter on this story: Claire Boston in New York at cboston6@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Dan Wilchins, Kenneth Pringle

©2018 Bloomberg L.P.