Traders Are Too Certain About the Path for Rates

Traders Are Too Certain About the Path for Rates

(Bloomberg Opinion) -- With quantitative easing in the rearview mirror, the Federal Reserve is delivering its message to the markets much more directly than in the past. Concerns of financial stability have been replaced with inflation concerns. In turn, traders feel more confident about the future path of the Fed’s interest-rate target than ever before. Be concerned.

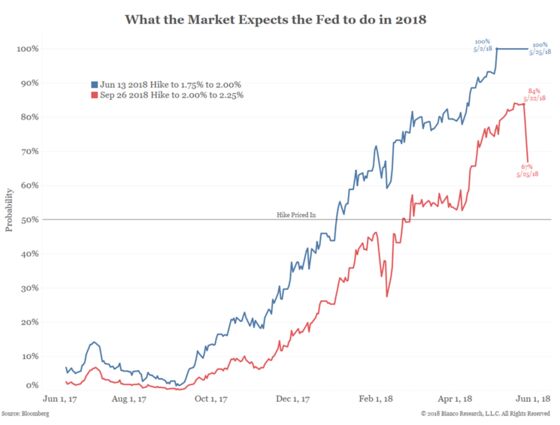

The chart below shows the odds, based on federal funds futures, that the Federal Open Market Committee will hike rates at the three remaining monetary policy meetings this year where Chairman Jerome Powell will hold a press conference. The markets are so certain that they are pricing in extremely high odds well in advance of the meetings. The odds of a boost at the June 13 meeting (blue line) hit 100 percent on May 2, or 41 days before the meeting. The odds of an increase at the Sept. 26 meeting (red) exceeded 80 percent on May 7, or 142 days before the meeting, before easing to a still historically high 67 percent following the release Wednesday of the minutes from the Fed's last policy meeting.

Such certainty so far in advance of meetings has rarely occurred in the modern Fed era. Anytime investors witness such certainty they should be concerned about the presumption that seeing into the future has become clear and predictable. It rarely is.

Of the 26 hikes between 1998 and 2015, the fed funds market typically priced in 100 percent odds just 15.4 days prior to a meeting on average. Clearly, traders feel confident the Fed will hold true to its word that it sees no reason to slow the pace of rate increase if they are willing to extend themselves this definitively more than 40 days prior to a meeting.

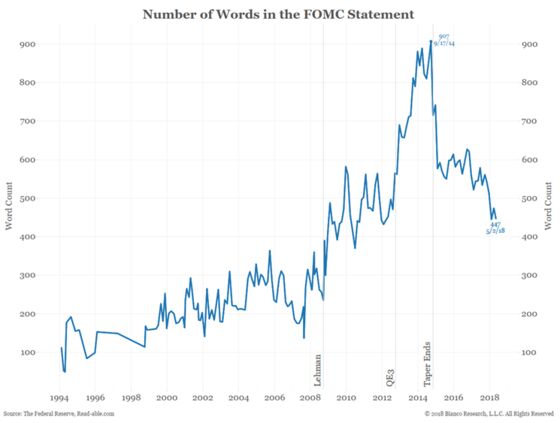

So why are traders so willing to go out on a limb? Part of the answer lies in how the Fed is communicating its message. As the chart below shows, the number of words in the FOMC statement peaked in September 2014 as the tapering of asset purchases came to an end. The most recent statement contained about half the words compared with the September 2014 meeting.

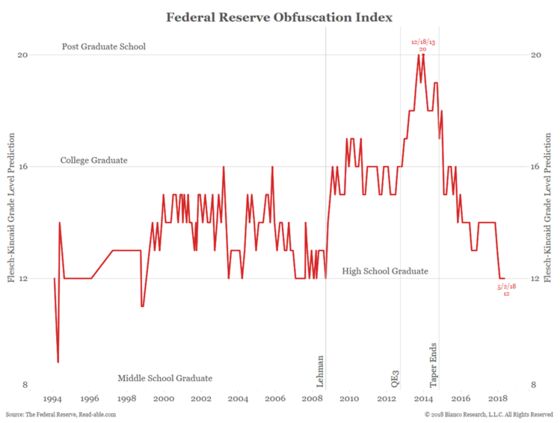

While the message is becoming shorter, it is also becoming easier to understand. The next chart shows the Flesh-Kincaid grade level necessary to understand each FOMC statement. It essentially measures the length of sentences and number of syllables in each word to discern the level of schooling one might need to understand the statement. The September 2013 Fed statement required a PhD in education for proper understanding. The May 2018 statement only required a 12th grade education.

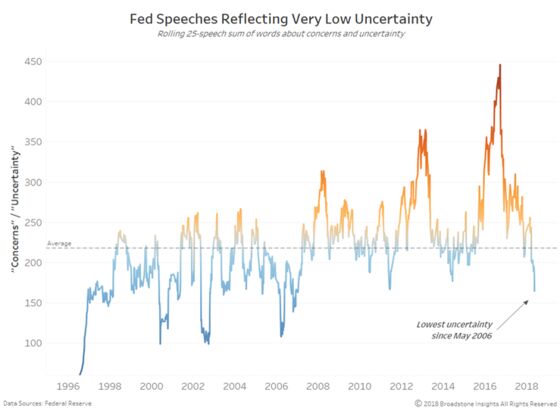

Along with more succinct statements, the Fed also gained traders’ confidence by appearing more confident itself. The next series of charts are culled from a database of every speech and testimony by a Fed official. They use rolling 25-speech counts (roughly six months) to remove noise from the larger trend. Most importantly, these are not brute force word counts like those in the charts above but the results of a natural language processing program that counts the words -- similar words -- and ensures that they are in the context of discussing monetary policy.

The chart below shows the Fed’s use of words pertaining to “concern” and “uncertainty” recently plunged to a new post-crisis low.

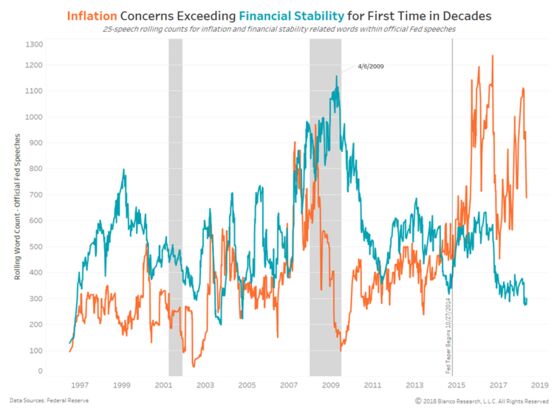

The next chart shows financial stability concerns plunged to a 14-year low while inflation concerns rose.

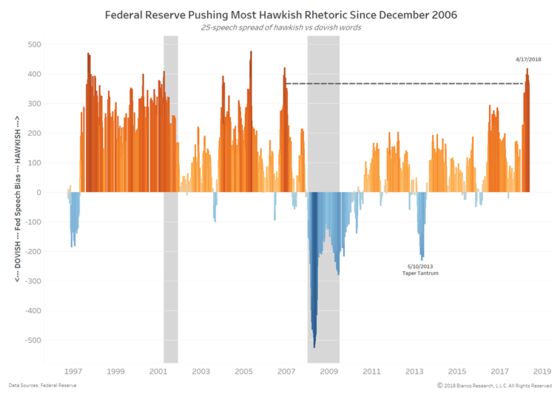

This has led to a Fed that is more hawkish in its tone than any other time in the post-crisis period.

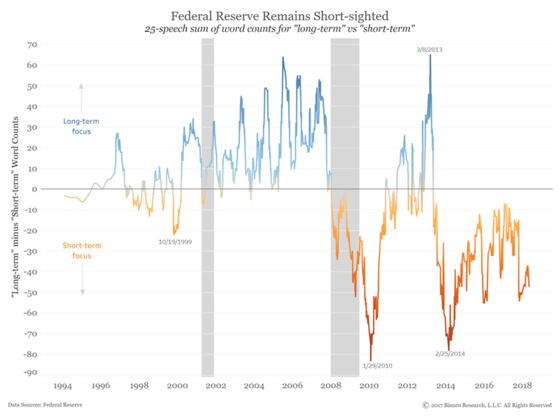

This more hawkish tone has coincided with a more short-term focus. Rather than giving vague goals about long-term policy, the Fed is being a bit more active in managing expectations for upcoming meetings.

All these factors have resulted in a near certainty among traders about FOMC policy. This is likely the Fed’s intention, but their desire to raise rates is predicated on the return of inflation. While economic surveys continue to point to its imminent return, actual inflation has yet to materialize in a meaningful way. In our last Bloomberg Opinion column we pointed out that these surveys have lost much of their predictive ability.

When corralling traders toward a particular position, you best be correct in your view. If inflation does not return at some point soon, the markets will eventually start to question the Fed’s confidence.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

©2018 Bloomberg L.P.