Big Days Are All Bad Ones as Stocks Punish Optimists Again

One message the market keeps sending: don’t get comfortable, because around the corner is pain.

(Bloomberg) -- None of the narratives floating around the market make any sense. Bond yields are too high, and too low. Politics don’t matter, then they do. There’s excessive inflation, or not enough.

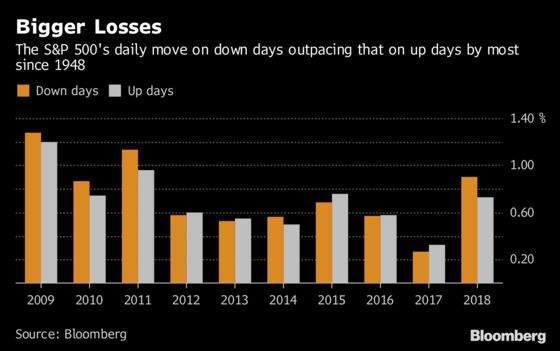

But one message the market keeps sending: don’t get comfortable, because around the corner is pain. Stock traders have been chained to their screens in a year when the average down day is 24 percent bigger than the average up one, the biggest gap since 1948.

It played out again Tuesday as investors were treated to a session of price swings that would have ranked with the worst of the preceding two years -- but in 2018 doesn’t crack the top 20. Phrased differently: the biggest decline in the S&P 500 last year, a 1.8 percent drop on May 17, would rank as the eighth largest since January. And it’s only May.

“What you don’t want to do as an investor is become too comfortable: it can be expensive,” said Donald Selkin, New York-based chief market strategist at Newbridge Securities Corp. “The optimism about coordinated global growth was the main mantra of market bulls just a few weeks ago. Where are they now?”

Only one thing has been constant in 2018, that every few weeks equities get hammered. U.S. companies are in the midst of one of the biggest earnings expansions ever, everything from buybacks to capital spending is surging and forward valuations are cheap. But it’s proving little barrier to intermittent wipe-outs.

It often seems as if good news is right on the verge of drowning out the bad. Like last week. Moods in the market brightened. The VIX eased. Data from Investors Intelligence showed newsletter writers classified as bulls reached the highest in almost two months. Statistics from Ned Davis Research Inc. reflected a similar trend. Everyone’s favorite stocks, the Faang block, vaulted to records just last week.

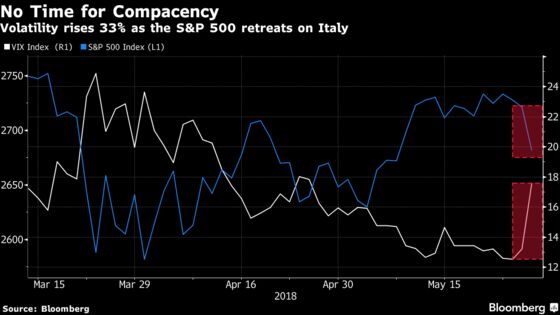

Then political uncertainty in Italy flared up, sending ripples across Europe. And the S&P 500, which had swung an average of 0.3 percent the previous 10 sessions, fell four times that on Tuesday. The Cboe Volatility Index spiked 29 percent, the most since March, to 17.02.

Ten-year yields dropped by the most since at least November 2016 to 2.78 percent. Half a month ago, when yields were at 3.1 percent, such a decline would probably have sparked an equity rally. Not Tuesday.

A one-day dent to sentiment amid political uncertainty in Italy is nothing to lose sleep over, according to John Stoltzfus, chief investment strategist at Oppenheimer. Futures on the S&P 500 were down about a point at 8:12 a.m. in New York Wednesday.

“For all the talk about increased market volatility, it’s worth noting that a read of the VIX” showed “a level of 13.22 at last Friday’s close,” Stoltzfus said in a note. “That’s a drop of over 64 percent from when it spiked in February to a level of 37.3. Investors are now less worried about near-term prospects for the market than they were in late January and early February.”

Tell that to all the hedge funds who took the other side of the trade. Speculators turned net short the VIX futures this month, a bet that pays off when markets stay peaceful, data from the U.S. Commodity Futures Trading Commission show, after being long since late January.

Investors in volatility exchange-traded funds did a little better. They put $265 million into the iPath S&P 500 VIX Short-Term Futures ETN in the past four weeks, after withdrawing from the product for five straight months. The VelocityShares Daily 2x VIX Short Term ETN posted four weeks of inflows in a row, the pattern unseen since October.

“Markets like to fret over the worst case scenarios which, unsurprisingly, almost never happens,” said Michael Antonelli, an institutional equity sales trader and managing director at Robert W. Baird & Co. “Honestly, we’ve all had our hand too close to the flame (2011 European crisis) so when something there flares up we all recoil in horror.”

To contact the reporters on this story: Lu Wang in New York at lwang8@bloomberg.net;Elena Popina in New York at epopina@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2018 Bloomberg L.P.