China's Equity Market Is About to Score a Rare and Timely Win

China’s domestic stocks are on track for a monthly gain that outpaces those listed offshore.

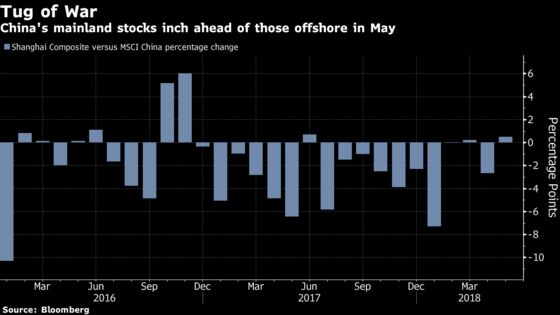

(Bloomberg) -- For only the third time since 2016, China’s domestic stocks are on track for a monthly gain that outpaces those listed offshore.

While the margin’s narrow, it’s a small win for mainland shares that bodes well for their big debut on MSCI Inc.’s global benchmarks this week. The Shanghai Composite Index is up 1.9 percent in May, on track to halt a three-month losing streak, while the MSCI China Index has gained 1.6 percent.

Onshore stocks have been perennial laggards, struggling to recover from a boom and bust that shook investor confidence in the country’s $7.6 trillion equity market three years ago. With international money about to trickle into A shares, the rebound in May stands out at a time when emerging markets all over the world are selling off.

“It comes at a convenient time because of the scrutiny being given to the A share market by international investors," said Howard Wang, who oversees JPMorgan Asset Management’s Greater China fund in Hong Kong. "It caught that tailwind just when it needed it.”

To be sure, gains in Shanghai don’t tend to last. Just last week, what looked like a bullish start for the onshore gauge had unraveled by Wednesday, ending with its first weekly loss in five. The whipsawing shows just how much sentiment onshore is vulnerable to any shift in language on global trade, as well as policy changes elsewhere that can hit an entire sector as huge as oil.

From June 1, MSCI will feature distiller Kweichow Moutai Co., brokerage Guosen Securities Co. and more than 200 other locally listed Chinese companies in its benchmark equity gauges. While the weighting of the shares will initially be tiny relative to the size of the market, the index provider said last week that this will increase faster than expected.

At less than 12 times projected earnings, the Shanghai Composite is about 7 percent cheaper than the MSCI China, data compiled by Bloomberg show. The discount is near its widest since 2014, a gap which Morgan Stanley strategists say will close as China’s capital markets open up, as long as trade concerns subside.

They see a 10 percent gain for A shares by June 2019, based on a 4,200 target for the CSI 300 Index, compared with the 1.9 percent decline they see for the MSCI China, according to a May 13 note.

“If and when investors do see some of their concerns alleviated, A shares’ relative valuation versus the offshore market is reasonable,” Laura Wang, a strategist at Morgan Stanley, said by phone from Hong Kong. “The A-share recovery is a fragile one and trade tensions remain a key risk. It’s still not the end of the situation at this point.”

To contact the reporter on this story: Sofia Horta e Costa in Hong Kong at shortaecosta@bloomberg.net

To contact the editors responsible for this story: Richard Frost at rfrost4@bloomberg.net, David Watkins

©2018 Bloomberg L.P.