Private Equity's Big Bet on Gas-Fired Plants Has Gone Awry

Private Equity's Big Bet on Cheap Gas-Fired Plants Has Gone Awry

(Bloomberg) -- Private equity shops thought they saw a sure-fire way to make a buck: build or buy dozens of power plants fueled by cheap Appalachian natural gas to replace old coal-fired units.

It hasn’t quite turned out that way, at least not yet. Many of the plants aren’t kicking off as much cash as the buyout firms had expected, according to bankers. There’s not enough demand to support the huge amount of additional new capacity, driving down electricity prices. And with President Donald Trump as a booster, shutdowns of coal haven’t come as quickly as anticipated while states are acting to keep nuclear plants open.

Few, if any, of the plants appear in danger of default, analysts said. But several plant owners are now using most of the extra cash they are generating to pay down debt.

Moreover, low prices and the results of a closely watched regional power-price auction scheduled for Wednesday could force many of the gas-fired plants to refinance their debt. At least one new U.S. plant, owned in part by an arm of private equity firm Ares Management LP, recently did so.

“There was an over-eagerness to accept aggressively optimistic revenue forecasts,” said William Nelson, a New York-based analyst at Bloomberg New Energy Finance.

The power-plant boom was spurred by an array of private equity firms including ArcLight Capital Partners, Ares Management and Panda Power Funds. About three dozen new natural gas-fired plants from the Northeast to the Midwest obtained at least $20 billion in debt, according to Ralph Cho, co-head of power in the Americas at South African bank Investec Plc.

Spokespeople for the private equity firms declined to comment or didn’t return messages seeking comment.

Luckily for plant owners, lenders and institutional investors are flush with cash and considering offering lifelines to ease the squeeze even some of the most efficient plants are experiencing.

“There’s a lot of eager money out there that’s overlooking low power prices and weak demand,” said Toby Shea, a New York-based analyst at Moody’s Investors Service.

New Refinancing

A 700-megawatt Indiana power plant completed a refinancing just after operations began in April. It’s owned by an Ares unit and Toyota Tsusho, the trading company within the Toyota Group, which is led by Japan’s largest company, Toyota Motor Corp.

The initial financing required owners to send excess cash (money left over after debt payments and capital expenditures) to lenders if revenue from an annual power auction came in much lower than expected. But under the refinancing, which was twice oversubscribed, owners will get a piece of the excess cash regardless of those auction prices, said Ravina Advani, a New York-based director at BNP Paribas SA, which led both financing deals.

Power-plant owners will take notice, said Mike Pepe, New York-based managing partner of broker-dealer GrandView Capital Markets LLC. “Most owners are already expecting less cash out of these plants than a couple of years ago.”

Toyota Tsusho has no specific plan to refinance its other two assets in the market operated by PJM Interconnection LLC, a company spokeswoman said in an email. She declined to specify a reason for the Indiana plant’s refinancing.

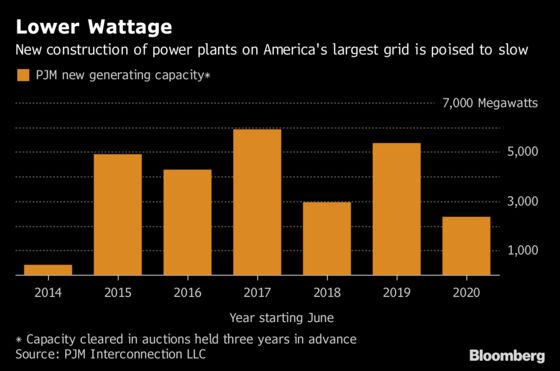

A critical factor will be the results released Wednesday of the annual power auction run by the nation’s biggest electricity grid, the PJM market. It will determine the size of short-term payouts to selected plants to meet demand on the hottest and coldest days for the year starting June 2021. It’s an even more important source of revenue for owners, with spot wholesale electricity prices dropping by more than half since 2008 to average $34.33 per megawatt-hour last year.

The pain is felt by gas-fired power plants across eastern U.S. grids, but especially so in the PJM market, which stretches from Washington to Chicago and serves about a sixth of the U.S. population.

The outlook isn’t great for the owners. PJM in December cut its long-term peak demand outlook to rise just 0.4 percent annually over the next decade, thanks in part to the growth of rooftop-solar. This summer, the grid will have 28 percent more supply than the peak demand forecast.

In last year’s auction, prices dropped to $76 a megawatt-day across the grid from $100 a year earlier, a four-year low.

Some analysts see the price rebounding at Wednesday’s auction, in part because fewer plants are getting built or that there may be more shutdowns. A report this week from the Rocky Mountain Institute said 50 percent of thermal power-plant capacity across the U.S. is likely to retire by 2030. But others predict little change in PJM, about $70 to $80 a megawatt-day, said Trevor McManamon, an energy adviser at PA Consulting Group in Denver.

“We sort of did overbuild in some parts of the U.S.,” said Paul Browning, chief executive officer of Mitsubishi Hitachi Power Systems Americas Inc., a seller of gas-fired turbines. “We have to let supply and demand rebalance.”

--With assistance from Chisaki Watanabe and Christopher Martin.

To contact the reporters on this story: Naureen S. Malik in New York at nmalik28@bloomberg.net;Brian Eckhouse in New York at beckhouse@bloomberg.net

To contact the editors responsible for this story: Lynn Doan at ldoan6@bloomberg.net, Joe Ryan, Will Wade

©2018 Bloomberg L.P.