Emerging-Market Stress Just Begun as Record Debt Wall Looms

Emerging markets face increasing pressure as a record slew of bonds come due.

(Bloomberg) -- Emerging-market companies and governments straining to deal with the rising cost of borrowing in dollars face increasing pressure as a record slew of bonds come due.

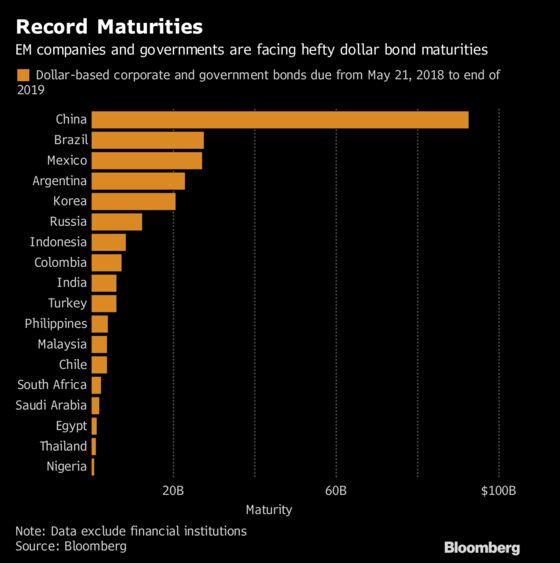

Some $249 billion needs to be repaid or refinanced through next year, according to data compiled by Bloomberg. That’s a legacy of a decade-long debt binge during which emerging markets more than doubled their borrowing in dollars, ignoring the many lessons of history from the 1980s Latin American debt crisis, the 1990s Asian financial crisis and the 2000s Argentine default.

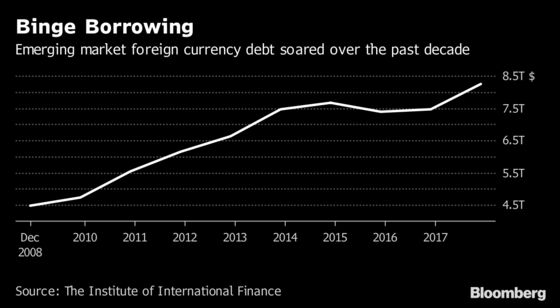

Even since the 2013 taper tantrum, the group’s dollar debt has climbed in excess of $1 trillion -- more than the combined size of the Mexican and Thai economies, Institute of International Finance data show.

Even those that have been effective in building local-currency debt markets aren’t invulnerable from the Federal Reserve-led rollback in global liquidity. That’s because of the significant presence of overseas investors sensitive to shifts in advanced economies.

"We look to be in for a pretty rough patch near term," says Sonja Gibbs, senior director for capital markets in Washington at the IIF, an association of the world’s biggest banks. "The sharper the rise in the dollar and rates, the greater the near-term contagion risk." Rising U.S. rates will have a knock-on effect even in local debt markets, she said.

The following charts showcase some points of stress.

China has far and away the most dollar debt coming due through next year among emerging markets. Though much of the debt is also owned by Chinese investors, strains have become clear in recent weeks, with some companies unable to issue at their preferred amounts and maturities, and others, unusually, marketing floating-rate notes.

Despite having defaulted in the early 2000s, Argentina has issued so much dollar debt that it ranks No. 4 on the list -- a testament in part to the impact that unprecedented U.S., European and Japanese monetary stimulus had in spurring a global hunt for yield since the 2007-09 financial crisis.

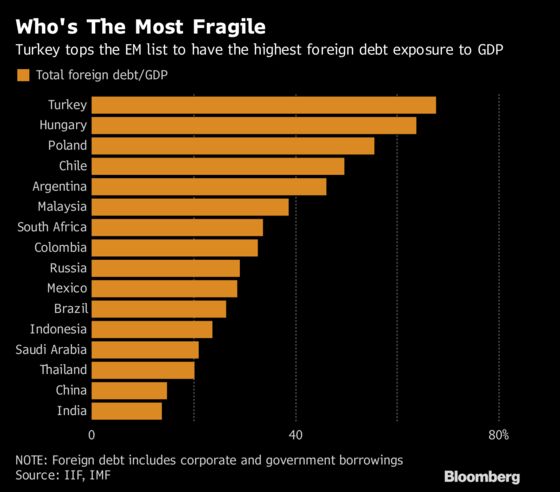

Turkey has the largest foreign debt load relative to gross domestic product, and perhaps not coincidentally has one of the worst-performing currencies against the dollar this year, down about 21 percent. Only Argentina’s peso has done worse among 24 emerging nations tracked by Bloomberg -- another country that ranks high on the debt metric.

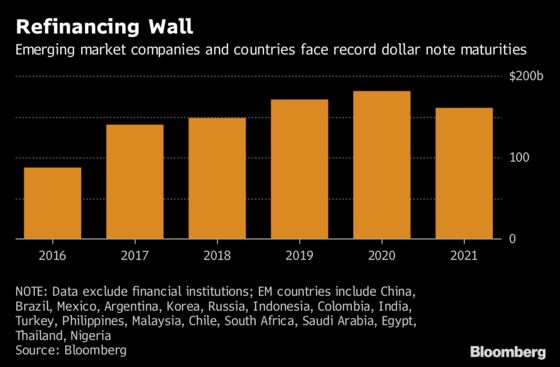

Benchmark 10-year Treasury yields have climbed this month to their highest since 2011, punching through 3 percent, even with the Fed less than half way done in its rate-hiking plans. And Jamie Dimon is warning of 4 percent yields to come. Fed forecasts suggest a peak in the policy rates in 2020 -- also the medium-term crest for developing-market debt maturities, according to data compiled by Bloomberg.

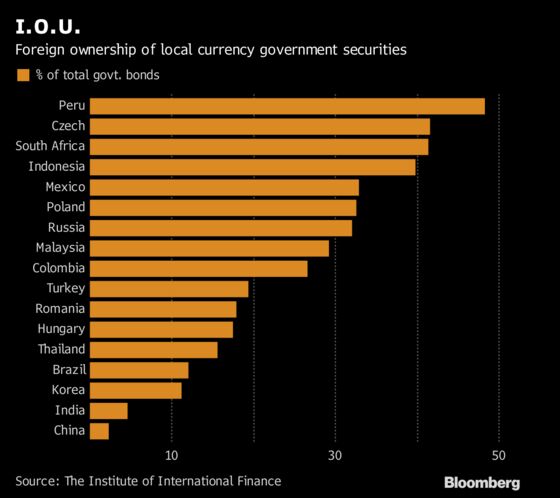

Dollar debt makes up more than three quarters of emerging market foreign-currency debt, which stood at $8.3 trillion at the end of 2017, IIF data show. But local-currency obligations can also be caught in the fray. Countries from Malaysia to Mexico saw an influx of foreign money into their securities amid the global yield grab that could reverse as benchmark developed-nation rates climb. China’s local currency bonds -- until recently largely inaccessible to global buyers -- is more insulated from swings in global investor sentiment.

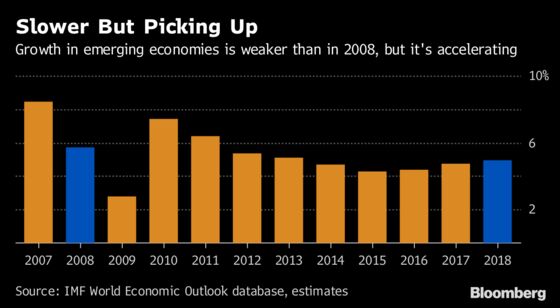

One reason overseas funds flocked to these economies is attractive growth rates, combined with inflation much lower than previous decades. That’s a powerful buffer for headwinds from higher rates. Domestic emerging-market growth "remains resilient," and areas with "early-cycle" stories such as South Africa and Latin America are positioned for a bounce-back in risk appetite in coming months, Goldman Sachs Group Inc. analysts said May 16.

Even so, the rapid build-up in debt over the past decade has alarmed some -- including Harvard economist Carmen Reinhart, who made headlines saying emerging markets are worse off today than during the 2008 crisis and 2013 taper tantrum.

"This is not gloom-and-doom, but there are a lot of internal and external vulnerabilities now that were not there during the taper tantrum," she said last week.

To contact the reporters on this story: Enda Curran in Hong Kong at ecurran8@bloomberg.net;Lianting Tu in Hong Kong at ltu4@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net;Malcolm Scott at mscott23@bloomberg.net;Neha D'silva at ndsilva1@bloomberg.net

©2018 Bloomberg L.P.