Iron King Vows to Protect Market From Days of Boom and Bust

Iron King Vows to Protect Market From Days of Boom and Bust

(Bloomberg) -- If the world’s biggest iron-ore producer has its way, the days of boom-and-bust price swings are over.

After a year in the job, Vale SA Chief Executive officer Fabio Schvartsman is pursuing a disciplined approach, keeping tens of millions of tons in the ground each year to prevent another painful glut that took prices below $40 a ton in 2015. But if prices look like they’re heading back toward the $100-plus super-cycle days, he’s also prepared to defend the status quo by unleashing that spare capacity onto the market.

The fact that the 64-year-old feels it’s his responsibility to cultivate a Goldilocks market for the steelmaking ingredient is a big deal: last week Wood Mackenzie identified Vale as the only producer capable of adding significant high-grade supply from new operations in the Brazilian Amazon.

“If and when there is a change in the market that sends prices through the ceiling, Vale will put more product in the market,” Schvartsman said in an interview on Friday at Bloomberg’s headquarters in New York. That would happen if prices are "dangerously approaching $100,” he said.

For now, that scenario seems distant.

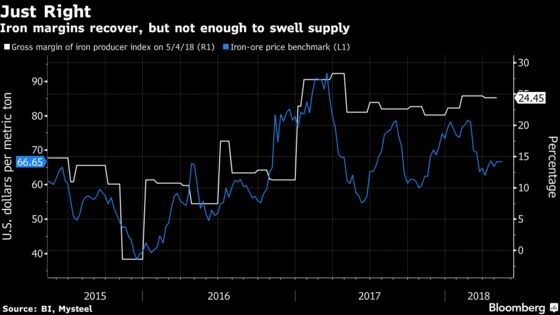

In March, prices slumped into a bear market as investors fretted over weaker-than-expected springtime demand in China, record holdings accumulated in mainland ports and rising trade tensions. While the price has steadied in the past several weeks, at $66.55 it’s still 16 percent below a late-February peak amid lingering concerns over Chinese stockpiles. Singapore futures resumed their slide Monday, losing 2.7 percent, the biggest intraday drop in a month.

The Australian government forecasts the raw material to slump in 2019 as Chinese imports level off and new mines including Vale’s S11D boost supply. Last week, Wood Mackenzie echoed Vale’s comparatively bullish outlook, saying the benchmark will be "comfortably above" $60 over the long term.

For the Rio de Janeiro-based company, ideally prices would stay in the current band of $60 to $80. Apart from Vale’s decision to refrain from operating at full capacity, that $60 floor is supported by high production costs at less efficient operators.

China’s pursuit of a more efficient, cleaner steel industry is creating a more segmented global iron market, with greater premiums paid for higher-quality ore. That windfall has Vale on track for a third straight annual earnings increase and is helping Schvartsman tame what was once the industry’s heaviest debt load.

With Vale’s shares and bonds outperforming and dividends on the rise, it’s easy to see why the CEO is content to produce 390 million to 400 million tons a year for the foreseeable future despite nominal capacity of 450 million tons.

But if it’s needed, it’s there. "We have the ability in three months time to bring up to 50 million tons a year of ore to the market," he said.

With little direct mining experience before taking over at Vale, Schvartsman has developed a taste for the industry, saying he wants to keep going in the role after his current contract expires next year.

To contact the reporter on this story: R.T. Watson in Rio de Janeiro at rwatson71@bloomberg.net

To contact the editors responsible for this story: James Attwood at jattwood3@bloomberg.net, Bob Brennan

©2018 Bloomberg L.P.