Corporate Bonds Sink Fast in One of Worst Tumbles Since 2000

100-day losses comparable to two other slumps in 18 years.

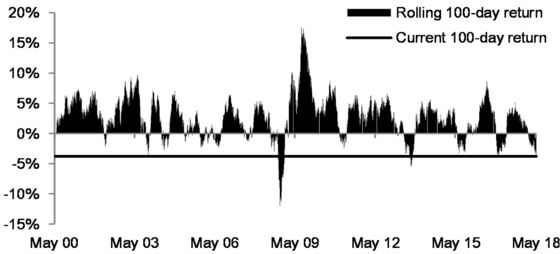

(Bloomberg) -- You need to rifle through 18 years of history to find selloffs that compare to the one corporate bond investors are now enduring.

Debt of American companies just posted their third-worst 100-day returns since 2000, according to a JPMorgan Chase & Co. index, as tighter monetary conditions leave their mark on high-quality bonds with longer maturities.

With negative returns likely to scare off retail investors, the outlook for the asset class looks grim, JPMorgan strategists said in a Friday note. But they find a silver lining: the highest yields in almost five years are likely to discourage new bond supply, which would at least help the technical picture.

The selloff in corporate credit is now on par with the rout in emerging markets. A Bloomberg Barclays index of U.S. investment-grade credit is down 3.9 percent so far this year, while dollar bonds of developing nations have declined at about the same clip.

The two markets are caught up in different problems. In developing economies, it’s a resurgent dollar and concerns over credit quality after a debt binge.

While corporate America’s earnings trajectory looks healthy, rising benchmark rates threaten investment-grade debt with average duration of over seven years. Securities with longer duration typically gain more when rates drop, but suffer stiffer losses when they climb.

“Duration risk is the main culprit,” Greg Venizelos, senior credit strategist at AXA Investment Managers, said in an interview. The firm is holding less investment-grade debt relative to benchmarks as the Federal Reserve ratchets up rates.

Full-year losses are unlikely to be as dire as the past 100 days, according to JPMorgan strategists. They cite strong demand among pension funds and overseas investors for long-dated notes. Bond prices also tend to converge to par the closer to an issue’s maturity, a dynamic known as curve rolldown.

To contact the reporter on this story: Cecile Gutscher in London at cgutscher@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma, Natasha Doff

©2018 Bloomberg L.P.