Indonesian Rate Hike May Slow, Not Stop, Foreign Funds Exit

Indonesian Rate Hike May Slow, Not Stop, Foreign Funds Fleeing

(Bloomberg) -- If the rupiah’s slide is any indication, Bank Indonesia will need to make good its pledge for stronger measures after its first interest-rate hike since 2014 failed to stymie a market selldown.

The rupiah declined as much as 0.8 percent to 14,158 against the dollar, its weakest since October 2015, as markets reopened after Bank Indonesia’s policy decision. The benchmark 10-year bond is set for a fifth weekly loss, with analysts saying that the central bank would probably need to raise rates again.

“This interest rate increase is probably enough to slow the outflow but it’s certainly not enough to reverse the selling pressure,” said John Teja, director at PT Ciptadana Sekuritas. “The central bank and the government really have to restore confidence in the rupiah and the economy,” he said, predicting a 25-basis point hike in the second half.

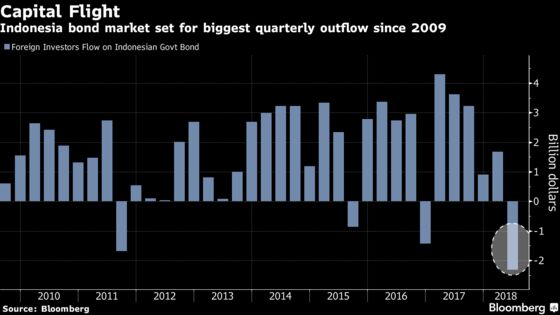

Global funds have dumped a net $2.3 billion of Indonesian sovereign bonds since the end of March, set for the biggest quarterly withdrawal based on data compiled from 2009, and pulled $1.2 billion from the shares amid a rout in emerging markets. Outgoing Governor Agus Martowardojo said that the central bank is ready to add to Thursday’s 25-basis point hike to ensure stability.

“If we need to take stronger measures, we won’t hesitate,” Martowadojo said. The rupiah is getting sold on Friday because investors had priced in the rate increase, he said, adding that higher U.S. yields continue to pressure the currency.

Should Bank Indonesia carry through with its promise, the bond markets may then stabilize, said Vivek Rajpal, a strategist at Nomura Holdings in Singapore. “That said, not all is clear on the external front. U.S. longer end is still rising and making newer highs which is weighing on markets.”

The Federal Reserve is poised to add to its six rate increases since December 2015 as soon as next month, and concerns of a faster tightening pace have propelled the 10-year Treasury yield to more than 3 percent.

Reserves Spent

The rupiah has declined 4 percent this year even as the central bank spent more than $7 billion of reserves since the start of February to halt the slump. The benchmark bond yield is trading near its highest in 14 months, while the stock index has dropped 9 percent in 2018.

Bank Indonesia’s hike “reflects the need for the central bank to strike a balance between the reality in the financial markets and the needs from businesses and consumers,” said Agus Yanuar, chief investment officer at PT Samuel Aset Manajemen. “We are expecting more interest rate increase this year, at least by another 25 basis points.”

Bank Indonesia is caught between the need to ensure that growth doesn’t stutter after first-quarter GDP gain fell short of estimates, while limiting the impact of further capital outflows. It isn’t alone in its challenges, with peers in the Philippines and India also tussling with weakness in their markets.

Foreign Holdings

Foreigners own about 38 percent of the sovereign bonds in Indonesia, among the highest of Asian emerging markets, making it susceptible to outflows. To preserve the yield appeal, the central bank may have to tighten again in two to three months, according to Jeffrosenberg Tan, head of investment strategy at PT Sinarmas Sekuritas.

The yield on the benchmark bond has risen 68 basis points this quarter to 7.358 percent, set for the biggest quarterly increase since December 2016. It reached a 14-month high of 7.39 percent on May 9.

To be sure, not all investors are bearish on Indonesia, with JPMorgan Asset Management’s strategist Tai Hui saying that that the dollar will weaken. When that happens, the higher yields offered by emerging markets including Indonesia will lure back funds, Hui said.

Indonesia’s high yields and its reformist agenda are still attractive, said Richard Lawrence, senior vice president for portfolio management at Brandywine Global Investment Management LLC, which holds the nation’s bonds as part of the $76 billion it manages.

“We see them as an attractive, slowly-reforming high real yielder that can spit off a steady stream of income,” Lawrence said in an interview in Singapore. “Once we get through this period of volatility, and we do think we’re going to come out the other side of it, it could be that BI is able to reverse that hike. It’s in the range of possibilities.”

--With assistance from Karlis Salna, Tassia Sipahutar and Lilian Karunungan.

To contact the reporters on this story: Harry Suhartono in Jakarta at hsuhartono@bloomberg.net;Ruth Carson in Sydney at rliew6@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, ;Divya Balji at dbalji1@bloomberg.net, Ravil Shirodkar

©2018 Bloomberg L.P.