China Bond Market Becomes Minefield, With Default Surprises

China's Bond Market Becomes Minefield, With Surprising Defaults

(Bloomberg) -- The days when only obscure Chinese companies defaulted on their debt are ending.

Four of the five issuers that have defaulted for the first time in 2018 are companies with public listings, which used to be regarded as assuring better governance and information disclosure. That’s as many by this type of firm as happened in 2014 through 2017, data compiled by Bloomberg show. For investors, the change means it’s dangerous to make assumptions.

“Our first and foremost task now is to avoid stepping on mines,” says Wang Ming, chief operating officer at Shanghai Yaozhi Asset Management LLP, which oversees 12 billion yuan ($1.9 billion) in assets. “It’s increasingly difficult to tell which one will default, which not."

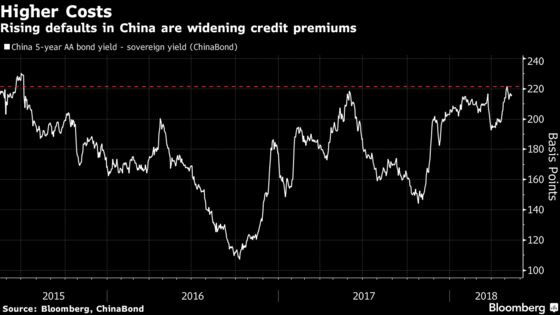

It’s another step in the gradual evolution towards risk-based credit pricing that China’s financial reformers are seeking without triggering a systemic financial blowup.

Without having had the chance to build up credit-research teams with years of experience, fund managers are having to gin up some quick rules of thumb to manage the increase in risks. (China only began allowing defaults back in 2014, as President Xi Jinping’s team began putting more focus on defusing financial risks.)

For Wang, the answer is sticking mainly with bonds sold by the central government, state-directed policy banks and some other state-owned issuers and AAA rated companies. Having the top debt grades may not work for all, though, as China’s domestic credit-rating companies are generally regarded as having less stringent standards than found elsewhere.

It all suggests that a further widening in yield premiums is in store for Chinese credit, making it tougher for weaker companies to refinance maturing debt. Spreads may rise a further 30 to 40 basis points, with the potential for more defaults to catch investors "off guard," Jeffrey Zhang, strategist at Standard Chartered Plc wrote in a note dated Friday.

The additional returns investors demand to hold AA rated five-year debt over government notes this month climbed to the highest since July 2015 -- when Chinese markets were under strain from a bursting stock bubble. Benchmark rates are also on the rise, with 10-year sovereign yields at a five-week high of 3.72 percent as of 2:08 p.m. in Shanghai.

Issuers with AA ratings or below are struggling -- they accounted for little more than one-tenth of the sales from companies rated AAA- and above last month, data compiled by Bloomberg show.

“The impact is already starting to be seen, and the trend will certainly continue,” said Shen Bifan, chief strategist at Shenzhen Spruces Capital Management Co., which has some 4 billion yuan of assets under management. “We avoid anything we’re not familiar with. That’s the best way, and probably the only way, to avoid getting into trouble.”

The consequence of making the wrong picks can be severe. The top five holdings of Double Bonds Plenty Income Bond Fund, sold by Huashang Fund Management Co., were all distressed by the end of the first quarter, and it’s now sitting on a year-to-date loss of 20 percent.

Rising defaults have spurred worries about some funds’ risk controls -- read more here.

Here’s a description of the first-time defaulters so far in 2018, according to data compiled by Bloomberg:

| Date | Company | Listed | Bond ID |

| Jan 29 | Yiyang Group | No | JV8263529 |

| Mar 14 | Shenwu Environmental Technology | Yes | AR7750201 |

| Apr 23 | Fuguiniao | Yes | EK8694540 |

| Apr 30 | China Security & Fire | Yes | JV6566873 |

| May 5 | Kaidi Ecological & Environmental Technology | Yes | EI6553578 |

--With assistance from Ling Zeng.

To contact Bloomberg News staff for this story: Helen Sun in Shanghai at hsun30@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net;Richard Frost at rfrost4@bloomberg.net

©2018 Bloomberg L.P.

With assistance from Editorial Board