Widow-Maker Trade Is Back After Rising Yields Spur Bets in Japan

‘Widow Maker’ Bets in Play as Super-Long Japanese Bonds Decline

(Bloomberg) -- For years, betting against Japanese government bonds was known as a loss-making trade. Now, there could be a window of opportunity.

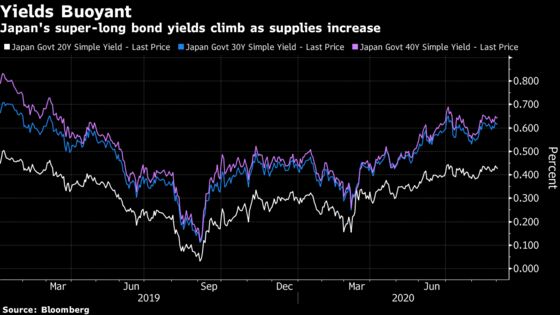

Japan’s long-dated yields are hovering near 16-month highs after the government massively boosted debt supply to fund its stimulus spending. Waning demand from key buyers, who are looking further to U.S. and European markets, plus less central bank support could set the stage for bonds to extend losses.

All this is bringing into play the question of whether the time is ripe to bet against Japanese sovereign debt, a trade famously dubbed “the widow maker” for the losses it inflicted on investors in the past. Prime Minister Shinzo Abe’s resignation jolted markets and with more supply due this two weeks, players are bracing for yields to shoot higher.

“Investors are only keeping a dip-buying stance even as yields rise due to concerns over shrinking demand and increasing supplies,” said Eiichiro Miura, general manager of the fixed-income department at Nissay Asset Management Corp. “Wariness about demand looms as the Government Pension Investment and other public funds are expected to buy less JGBs.”

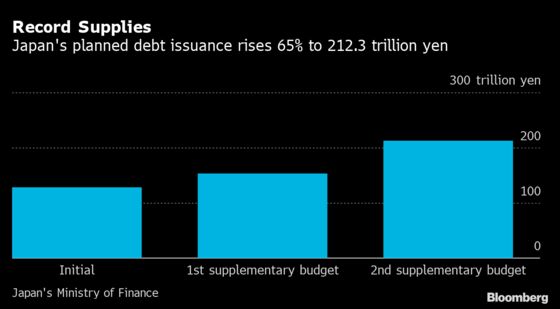

Super-long JGBs have fallen after sovereign debt issuance rose 65% to 212.3 trillion yen ($2 trillion) for the fiscal year ending March 2021. Yields on 30-year JGBs climbed above 0.6% in July for the first time since March last year and are now hovering near that mark.

The Ministry of Finance will be offering 4.6 trillion yen of debt in three maturities over two weeks, with a 30-year sale set for Thursday and a 20-year auction scheduled a week later.

Demand is easing as key buyers shift money to Treasuries, overseas credit and higher-yielding European debt. The Government Pension Investment Fund, Japan’s biggest investment vehicle, is increasing its allocation of foreign bonds by 10 percentage points to 25% while cutting its domestic allocation.

While Treasury yields rose in August after the Federal Reserve’s pivot on inflation led to a selloff, the allure of the world’s biggest debt market means the advance has started to unwind.

Less Support

JGBs may also lack a key pillar of support as the Bank of Japan has refrained from boosting bond purchases at its regular operations. It’s expected to allow the yield curve to steepen after Governor Haruhiko Kuroda said in June that Japan’s super-long yields weren’t high compared with that of other nations.

The Bank of Japan keeps the 10-year bond yield anchored around zero percent, which saps trading at the short-end of the curve.

Market players are also awaiting the appointment of Abe’s successor, with the front-runner Yoshihide Suga pledging Wednesday to maintain the outgoing prime minister’s ultra-easy monetary policies.

“Political factors aren’t likely to alter sentiment toward JGBs as Japan is expected to continue its economic and monetary policy under the leadership of Suga,” said Nissay’s Miura. “Japan’s policy will also stay intact amid the coronavirus crisis irrespective of who becomes the next prime minister.”

Still, some warn that the rise in super-long yields may be nothing more than a temporary phenomenon.

“Supply and demand are slackening due to a slew of super-long debt auctions and activity being slowed by summer holidays,” said Naoya Oshikubo, a senior economist at Sumitomo Mitsui Trust Asset Management. “But by early September, when investors return from holidays and the rush of super-long auctions come to an end, such a steepening will also likely lose momentum.”

Stimulus Risk

The spread between 10- and 30-year JGBs has remained above 50 basis points over the last two months after touching a record low of 25 points in March. It stood at 56 basis points on Wednesday.

“We’ll see a gradual increase in spreads due to concerns about oversupply,” said Akio Kato, general manager of strategic research and investment at Mitsubishi UFJ Kokusai Asset Management Co. “There is always a risk that the government will take an additional fiscal stimulus package, which could lead to increased debt issuances toward the end of the year.”

©2020 Bloomberg L.P.