‘WeWork Flu’ Strikes at the Heart of the U.S. Equity Market

‘WeWork Flu’ Strikes at the Heart of the U.S. Equity Market

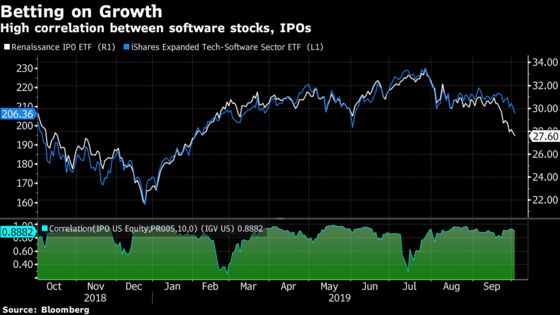

(Bloomberg) -- Software stocks that constitute the biggest part of the U.S. equity market are teetering, and recent struggles by the cohort of tech unicorns looking to go public aren’t helping.

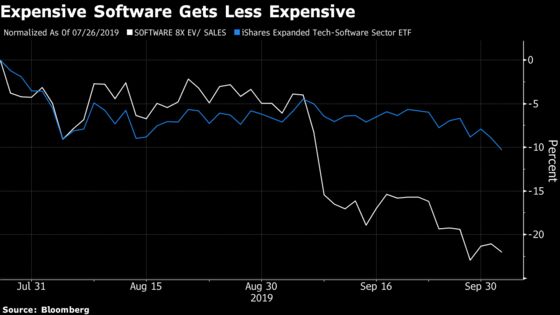

An exchange-traded fund that tracks the likes of Oracle, Intuit and Autodesk has plunged more than 10% since hitting an all-time high in July -- more than double the drop in the S&P 500. It ended Wednesday below its average price for the past 200 days for the first time since January.

The group has something in common with the once high-flying private companies that lined up to go public this year, from Uber to Endeavor, WeWork and Peloton: sky-high valuations. While each is expensive for a different reason -- IPOs are expected to deliver huge profits down the line; software makers have established records of performance -- investors lately have shown an aversion to paying up for growth.

“Arguably, software stocks have a case of the ‘WeWork flu,’ as investors have suddenly become more cautious on stocks with high valuations,’’ said Conor Sen, portfolio manager at New River Investments. “And while investors loved those stocks when they had strong momentum, now their charts look more ominous, perhaps leading fast money to head for the exits.”

Indeed, a Goldman Sachs basket of particularly pricey software stocks has tumbled more than 20% since its July 26 high -- nearly twice the decline suffered by the ETF tracking the industry’s shares.

Lofty Expectations

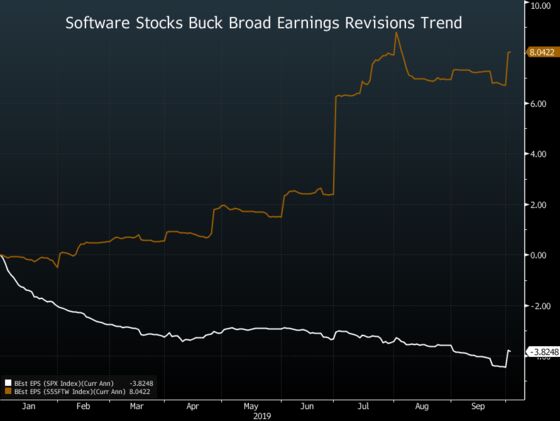

As 2019 earnings estimates for the S&P 500 as a whole have come under consistent pressure this year, bottom-up forecasts for the software and services group have pushed higher. That’s got analysts at JPMorgan warning of elevated volatility the reporting season, and investors cautioning about a further unwind in the space.

“The third quarter earnings cycle for software stands to be a pivotal factor in defining price direction into year-end,’’ write JP Morgan derivatives strategists led by Shawn Quigg, noting that poor results could see valuations come under further pressure.

He links disappointing debuts like Uber and Peloton, along with the failed IPO attempt by WeWork and Endeavour’s subsequent balk at going public, among the problems hitting software stocks that might not have as long a track record as the Microsofts and Oracles of the world.

“A string of disappointing IPOs and IPO attempts, along with the broader pullback in high-growth new-tech stocks, which have also yet to prove themselves through a full business cycle, further exemplify the recent reduction in risk tolerance among investors.’’

This group will be more volatile than normal during this reporting period, according to the analysts. The results of early reporters like Atlassian and ServiceNow, which release results on Oct. 17 and 23, respectively, may also be instrumental if treated as bellwethers for the space. As such, the team recommends buying straddles in Square, Twitter, and Twilio to bet on big moves this earnings season.

De-Crowding

The reversal in sliding bond yields at the start of September set the stage for a cascade of exits from crowded software stocks, according to Dan McMurtrie, founder and portfolio manager at Tyro Capital Management.

The amount of time it would take for many software companies to generate the free cash flow to justify their current valuations stretched so far into the future that they tended to act as pure duration proxies, that is, very sensitive to changes in interest rates.

“Momentum participated, then fundamental moved in, and we’ve ended up in a situation where a lot of different types of styles are putting money into tech and software-as-a-services specifically, and that’s going to end up a problem,’’ he said. “An object in motion remains in motion until the chart breaks, then other risk factors come into play.’’

Self-styled fundamental investors were able to latch on to the high recurring revenues and strong operating cash flows generated by software companies, smitten by the stickiness and cost savings provided by their products. But there’s now career risk involved for portfolio managers who waded into this space based on their perception of strong fundamentals and who are now staring at abrupt declines they may not be able to explain, McMurtrie reckons.

“People were going ‘these fundamentals are so good’ when the space was trading on technicals and duration,’’ he said. “It’s always dangerous for a portfolio manager when what is driving flows and trading is not what they think it is – if this lasts longer than a month, and you don’t have a good answer, there’s no way to defend your agency in picking that stock in the first place.’’

To contact the reporter on this story: Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Rita Nazareth

©2019 Bloomberg L.P.