‘We Call It Uninvestible’: Market Views After Another Rout

Market participants are largely averse to calling a bottom to the rout in global equities.

(Bloomberg) --

After twice seeing stocks on Wall Street tumble by the most since 1987 in recent days, market participants are largely averse to calling a bottom to the rout in global equities.

Investors are grappling in the dark on earnings estimates as authorities around the world shut down economic activity in an effort to avert a humanitarian disaster caused by the coronavirus. That’s overshadowing moves by economic policy makers to cushion the impact. With volatility expected to remain high, traders are on the lookout for more fiscal stimulus and, most importantly, evidence the outbreak is on the wane.

Here are some of the views of investors and strategists:

Uninvestible

Nadine Terman, chief executive officer of Solstein Capital LLC:

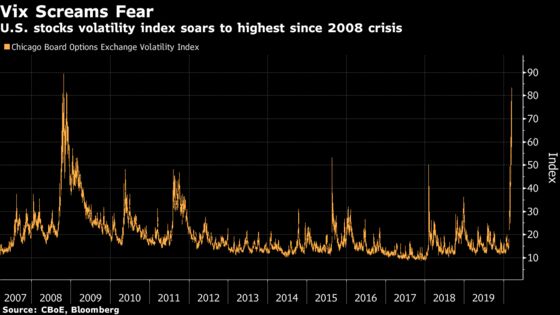

“When VIX is above 31, we call it uninvestible. The issue is that safe havens like gold or Treasuries can go down just with everything else. What you have to do is be very cautious about going into longs.”

Room for De-Rating

JPMorgan Chase & Co. strategists including Mislav Matejka:

“In order for a more lasting market rally, we believe that we need to see either an exceptional policy response, which has not happened yet, or more directly, we would need to become comfortable that the peaking out in the virus outbreak is at hand. This still seems to be quite far away, and things could get a lot worse before they get better.”

On stocks, “we note that markets lost more than half of their initial value during the last two recessions, versus current 20%. In addition, the last three recessions saw P/E multiples of 10.1x, 13.8x, and 10.2x at the low, while current P/E stands at 15.2x, and 14.5x at the recent trough on 12 March. There could be room for more de-rating from here.”

Encouraging Signs

Jean Boivin, Head of BlackRock Investment Institute:

“What will it take to stabilize markets? A decisive, preemptive and coordinated policy response is key, in our view. We see encouraging signs on both sides of the Atlantic that such a monetary and fiscal response is underway. The sharper the containment measures taken and the deeper the economic hit in the near-term, the more confident we should be about the rebound after such measures are lifted. We see the shock as akin to a large-scale natural disaster that severely disrupts activity for one or two quarters, but eventually results in a sharp economic recovery.”

Mind the CP Gap

Ned Rumpeltin, European head of currency strategy, Toronto Dominion:

“The Fed is doing a lot but it has a bit more to do. The dislocations we are seeing in commercial paper markets, for example, is an area that needs to be addressed. That will help ease pressures elsewhere, as we still have plenty of signs of stress, illiquidity, and wide spreads. Beyond the Fed, we are encouraged to see policy responses accumulating. The G7 pledged to cooperate on the virus response while the EU finance ministers are moving clearer in the direction of a stronger fiscal response. There is still some distance to travel, but we are at least on the right track. It may be very difficult to begin pricing in any sort of real recovery until the pace of contagion starts to slow.”

Impossible to Predict

Jon Hill, U.S. rates strategist at BMO Capital Markets:

“That the VIX closed above 80 for only the third time in history is deeply concerning. The other two instances were during the global financial crisis in the fourth quarter of 2008. It’s now apparent that we’re in the depths of the Covid-19 financial crisis of 2020, with much left to be written. What comes next is nearly impossible to predict, but escalating fiscal injections and a commercial paper funding facility look to be the proximate policy steps.”

Government Action

Mark Haefele, chief investment officer at UBS Global Wealth Management:

“Governments have started to announce the sort of targeted fiscal policies that the market is looking for -- aimed at helping viable businesses survive the crisis. But to reassure markets in the absence of better news on the spread of the virus, we may need to see a more open-ended commitment from governments to assist companies and individuals facing cash flow problems arising from the Covid-19 outbreak.”

Still Temporary

Jim Paulsen, chief investment strategist at the Leuthold Group:

“Beginning this week, economic reports will most likely start reflecting the negative impacts of the recent virus-related shutdowns. No doubt, the news will get worse, but at least investors will finally be reconnected with fundamental information flow. The fear of bad data is often worse than its reality.”

“The essential premise widely believed when this crisis began -- that it would be temporary -- still appears to be its most likely outcome. Markets will still be apt to look beyond the current economic hit if a consensus develops that it is indeed temporary, and the economy will recover. And, stock prices and bond yields will not only increase to reflect a pending recovery but will rise because of a reversal of fears.”

Wait it Out

Eleanor Creagh, market strategist at Saxo Capital Markets:

“It is too early to tell whether the health crisis will develop into a more serious and lasting global solvency crisis, or how deep and dark a recession would be. Confidence is frail and the fear of the unknown and prospect of continued aggressive economic shutdowns is enough to keep risk assets under pressure. There will come a time for bargain hunting, but we are inclined to wait it out. Plan for the best and prepare for the worst.”

Correlation Panic

Altaf Kassam, EMEA Head of Investment Strategy & Research at State Street Global Advisors:

“What makes for a panic feel is the speed and broad-based nature of the sell-off, not the absolute levels we have: We’ve seen a higher VIX, a lower oil price, and steeper credit spreads in the recent past, but not all at the same time, and together with the lowest rates ever.”

“The more the coronavirus spreads, the more financial markets will continue to sell off. The question now is what more aggressive, coordinated responses policy makers can offer to further support markets considering the underwhelming response to policy action so far.”

Peak Uncertainty

Manishi Raychaudhuri, head of Asia Pacific equity research at BNP Paribas SA in Hong Kong:

“Investors don’t have a sense of where the earnings are likely to be -- in fact, those are the most basic variables.”

“Possibly we’re living in an environment of peak uncertainty.”

Generational Moves

John Woods, chief Asia-Pacific investment officer at Credit Suisse Group AG:

“For as long as we see concern over the policy reaction, it’s far too soon to call an end to this crisis.” Even so, “increasingly I’m of the view that the worst of the damage is behind us.”

“The volatility that we have seen in the markets over the last week or so happens only once or twice in a generation.”

Confidence Crisis

Olivier d’Assier, head of APAC applied research at analytics firm Qontigo:

“While it is not yet a financial crisis, it is already a crisis of confidence. When confidence goes, everything goes. It does not matter what ‘rational’ monetary or fiscal measures are hastily put in place, investors simply do not have enough confidence to make a forecast of return and therefore only focus on the risk side of the equation.”

No Sign of Bottom

Mark Galasiewski, chief Asia-Pacific analyst at Elliott Wave International:

“Before you see a bottom you want to see markets diverge across asset classes. Right now, everything seems to be correlated, falling uniformly so there’s no sign of a bottom yet.”

©2020 Bloomberg L.P.