‘Pulp Fiction’ Stock Spectacle Gets Less Scary as It Goes Along

Just another crazy December day on Wall Street.

(Bloomberg) -- On Thursday, U.S. stocks plunged to a loss that would’ve dwarfed any bad day in 2017, pivoted, then surged to pull off their first back-to-back gain in a month.

Just another crazy December day on Wall Street.

“Investors are becoming desensitized,” said Bryce Doty, senior vice president at Sit Investment Associates. “It’s like watching ‘Pulp Fiction.’ Halfway through, the violence doesn’t even bother you anymore.”

The latest Dow swing was only slightly bigger than the average up-and-down move last week, though back then equities were tumbling in the direction of a bear market. Strategists are starting to ask: if days like these are now normal, is there a context in which the whole three-month rout starts to feel routine?

A few research shops say yes, particularly if it ends -- as they believe it may -- right around here. Market turmoil that happens when the economy is holding up reminds Jim Kelleher, the director of research at Argus Research, of past stock declines that ended gently, he said in a note Thursday.

Unless evidence emerges of deep global growth erosion, what’s going on now “will prove to be shorter and more shallow than the declines experienced in ‘classic’ bear markets.”

Brutal days in the market are happening at a time gross domestic product is rising, interest rates are still low and earnings are solid. That could make this plunge a “check on valuation” rather than “the start of a long decline,” Kelleher wrote, acknowledging that investors have been more likely to focus on the negatives of the economy and market.

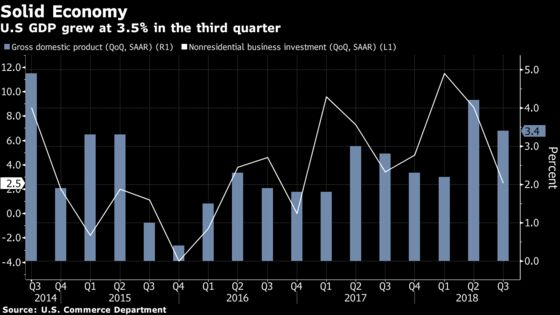

The U.S. economy expanded at 3.5 percent in the third quarter, and is expected to grow next year, though at a slower pace. Companies are posting record-breaking holiday sales, and consumption, which accounts for around 70 percent of the economy, rose more than forecast in November. The Institute for Supply Management index, a gauge of U.S. manufacturing, rose last month, with new orders picking up and companies adding workers.

“Investors are wondering if this will be a crash,” said Dave Campbell, a principal at San Francisco-based BOS, which manages around $4.2 billion. “The risks are there, but they’re always there. They’re more heightened but it’s not the most likely outcome. The economy continues to grow -- maybe a little more slowly -- but next year markets will have hit their lows and we’ll be on the rebound.”

Twenty percent declines in shares hardly assure a recession. In fact, only half of the 14 bear markets that took place since World War II occurred during a prolonged economic contraction, data compiled by LPL Research show. Sell-offs when the economy contracts are bad, with the S&P falling 37 percent on average. The ones that come when growth is positive level off at 24 percent.

LPL’s senior market strategist, Ryan Detrick, is betting on the latter. He expects the U.S. economy to rise as much as 2.75 percent in 2019.

“In the end, the largest market corrections take place during recessions. Will we have a recession in 2019? We don’t think so,” Detrick said in a note to clients. “The bottom line is that you can have bear markets without a recession.”

Bear markets that go way past 20 percent tend to be associated with “secular transitions,” things like the excessive valuations of the dot.com bubble. Near-bear markets, however, are more common around technology transitions or one-time disruptions, according to Argus. The one going on now is occurring next to high consumer and small business confidence, solid industrial activity and low interest rate and energy inputs.

The bad kind of bear market lasts an average of 556 days and is much worse than 20 percent, according to Argus’ analysis. The mean peak-to-trough decline during recent bear markets has been around 35 percent. And if stocks can reverse their recent downtrend, the current "bearish duration" would be uncommonly short, at less than 90 days, he said.

To contact the reporters on this story: Vildana Hajric in New York at vhajric1@bloomberg.net;Elena Popina in New York at epopina@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2018 Bloomberg L.P.