‘Most Important Thing Is the Dots’: Wall Street Reacts to Rate Hikes

‘Most Important Thing Is the Dots’: Wall Street Reacts to Rate Hikes

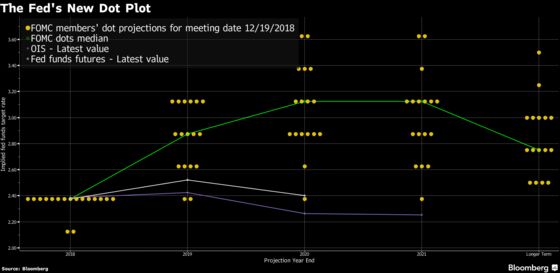

(Bloomberg) -- Stocks pared gains, short-term Treasury yields rose and the dollar trimmed losses in the minutes after the Federal Reserve raised borrowing costs and its “dot plot” showed one fewer interest-rate increase next year. Here’s what traders and strategists were saying:

- Jeffrey Rosenberg, chief fixed income strategist for BlackRock Financial Management, on Bloomberg Television:

“The most important thing is the dots. The dots met market expectations. A little bit of a disappointment in not seeing bigger reduction in terms of further gradual increases, just the introduction of some in there to soften it, there was bigger expectations there, but I think that’s minor relative to the dots. I think you got the dovish hike.”

- Dennis Debusschere, head of portfolio strategy at Evercore ISI:

“10-0 vote on the hike, that sends a strong signal to Trump, potentially. Given we know some doves have been calling for a pause. They signaled two instead of three hikes in 2019 and kept the gradual increase language in, which investors will view as hawkish.”

- Scott Minerd, Guggenheim Partners chief investment officer:

“We’re looking at a world where markets have gotten so spoon-fed for so long that any big change in anything upsets them. The interesting thing is the volatility around financial assets is introducing another element of risk that I don’t think any of us anticipated to happen right now. I think people are scared.”

- Bob Baur, chief economist at Principal Global Investors:

“I think the Fed may be underestimating other factors at play. Trade has been making headlines, but I think a gradual tightening of monetary policy has been the driving force behind recent market volatility. With corporate borrowing and spending still high, and the Fed continuing to reduce its balance sheet, I’d expect volatility to remain if this tightening continues.”

- Mike Loewengart, vice president of investment strategy for E*Trade Financial Corp.:

“This hike is a vote of confidence in our economy for 2018, but essentially that’s a wrap, and we’re now in some uncharted territory as 2019 comes into focus. To be honest this bull run has been pretty long in the tooth and the pullback should not have been too much of a surprise. But moving forward we’re seeing a fair amount of pitfalls that could turn the economy south: Slowing global growth, a ballooning deficit, faltering bond market punctuated by higher borrowing costs, trade disputes, and a fragile housing market just to name a few.”

- Max Gokhman, the head of asset allocation for Pacific Life Fund Advisors.

“It’s exactly what we expected. We thought the dot plot would be revised to two hikes and the statement language would be softened. We did think that ‘data dependency’ would emerge in some form, but instead the statement left its forward guidance as implying that there’s room for further increases. That’s about the only thing that could have made this the most dovish hike of 2018. Also, in my opinion there was ample rationale for the Fed to skip December’s hike and resume in March -- but ironically the President pressuring the Fed so publicly took that option out.”

- Zhiwei Ren, Penn Mutual Asset Management portfolio manager:

The market is pricing a much more dovish Fed than the dot plot is. It’s showing two more hikes next year -- that’s different. The market is billions of dollars of capital being allocated. The dot plot is just several Fed governors, their personal opinion, with no money on the line. Talk is easy, money is worth more, in my opinion. In the past several years, that’s what happened -- the dot plot converged to market pricing.

- Frances Donald, head of macro strategy at Manulife Asset Management:

The Fed is staying with the same issues that it’s been with for years: what’s the inflation outlook, what’s the growth outlook, what’s the jobs outlook? Financial market turbulence, pressures from other policy makers -- those aren’t necessary to acknowledge that the inflation outlook is deteriorating. The growth outlook is deteriorating for 2020 and the global growth and inflationary pressure are also subsiding. Those are enough for the Fed to turn dovish.

To contact the reporters on this story: Sarah Ponczek in New York at sponczek2@bloomberg.net;Vildana Hajric in New York at vhajric1@bloomberg.net;Lu Wang in New York at lwang8@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2018 Bloomberg L.P.