‘Mindless’ Bond Market Rally Spreads Fresh Fear and Loathing

‘Mindless’ Bond Market Rally Spreads Fresh Fear and Loathing

(Bloomberg) -- To Chris Rupkey, global markets have handed the keys to a wild driver -- one that keeps veering the bulls in risk assets off course.

“It’s just a mindless bond market rally -- once it gets going, it gets going,” the chief financial economist at MUFG Union Bank said in a recent interview with Bloomberg TV. “I don’t know who’s trading these markets. It doesn’t feel like its trading completely logically here.”

It’s a counterpoint to the Wall Street adage that the smart money in bonds makes it the leading indicator for global markets. And right now, fixed-income traders screaming warnings on growth have the ears of risk markets.

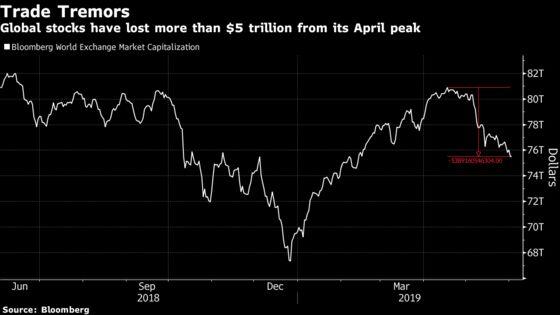

As U.S. stocks recover, equities around the world extended May’s $4 trillion mayhem into June as the trade war opens on multiple fronts. Treasury yields are falling at the fastest pace since the global financial crisis. The yield curve is inverted in key pockets, credit fears are rising and Wall Street strategists are tearing up their rate forecasts.

A ‘thousand year’-like bond rally and sliding inflation expectations shows markets are pricing-in monetary action and modest output over the long haul -- and it’s the only thing that matters for risk assets right now.

It’s a far cry from the bubbling melt-up earlier this year when stocks and bonds rallied in concert thanks to a Goldilocks-lite economy. JPMorgan Chase & Co. has slashed 10-year Treasury yields to 1.75 percent by year-end, as Morgan Stanley advises clients tensions in global commerce could eventually spur a recession.

Investors face all manner of investment conundrums, from how to hedge the G-20 meeting in options markets, to the near-record premiums for defensive stock trades, to the allure of risky credit in a $11 trillion world of negative-yielding debt.

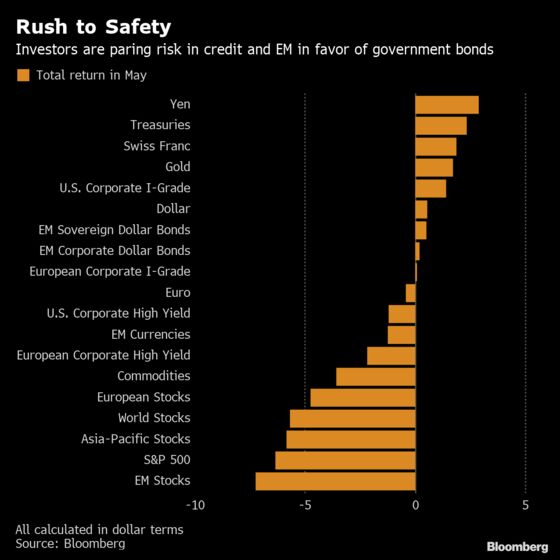

AXA Investment Managers and Manulife Asset Management are betting that the the outlook for inflation and growth is darkening. Like many of their peers, they’re paring risk in credit and emerging markets in favor of government bonds, especially those with longer maturities even at fierce valuations.

“Yields have seen a big move but we do think its possible that they could move lower from here,” said Chris Chapman, a portfolio manager at Manulife. Portfolio duration, a measure of sensitivity to interest-rate moves, has risen and Chapman is paring emerging-market currencies at the center of tensions. “It shapes our investment strategy in that we become more defensive.”

Pessimism that central banks can nudge inflation to long-term targets means bonds can keep rising and locking in rates now may pay off, according to Chris Iggo, chief investment officer for fixed income at AXA Investment. Put another way, far from a crazed Treasury rally, you can see it as a logical continuation of the bull market.

He’s sticking to higher-quality credit and long-dated government debt.

Slower growth would weigh on the companies with the most leveraged balance sheets. If 10-year yields sink below 2%, junk bonds are likely in trouble, according to Citigroup strategists. Cue alarm bells from some of the biggest investors over the debt binge by corporate America over the past decade.

As for stocks, dip buyers have been punished in May’s rout. Global-growth stocks are trading at the highest premium to value stocks on a forward price-to-earnings basis since 2001. Bulls may find solace in cheaper valuations, a potential trough in sentiment and the earnings trajectory aside from trade-sensitive sectors.

“The overall market reaction of equities down and yield curves flatter shows a broad re-pricing lower of global growth expectations,’’ Goldman Sachs Group Inc. strategist Ron Gray wrote in a report. “Macro data have not been very supportive and the 2018 narrative of slowing global growth has re-emerged.’’

JPMorgan said the probability of a U.S. recession in the second half of this year has risen to 40% from 25% a month ago. Goldman Sachs lowered its U.S. second half growth forecast by about half a percentage point to 2%.

“Reasons to spread fear and loathing” abound, Iggo said.

--With assistance from Ksenia Galouchko and Justina Lee.

To contact the reporters on this story: Cecile Gutscher in London at cgutscher@bloomberg.net;Anchalee Worrachate in London at aworrachate@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma, Natasha Doff

©2019 Bloomberg L.P.