‘Land of Confusion’ as Junk Defies Wall Street Recession Signal

‘Land of Confusion’ as Junk Defies Wall Street Recession Signal

(Bloomberg) -- Ride the great credit rally or get out before it falls apart?

Edward Park is unequivocal. The deputy CIO at Brooks Macdonald Asset Management has offloaded about a third of the firm’s credit exposure in favor of short-dated sovereign obligations since December on signs sputtering global growth mean the business cycle has entered its winter.

And he’s just getting started. The London-based manager of about $15.5 billion of assets overall now plans to sell a “large portion” of its corporate positions over the first half of the year.

“Debt costs are likely to rise as credit spreads expand to price in the higher default risk as we move to the end of the economic cycle,” Park said. “If flows were to reverse liquidity could become squeezed quite rapidly.”

Even if many of his peers are yet to vote with their feet just yet, the angst is widespread. The number of investors demanding companies reduce leverage climbed to a decade-high this month, according to a Bank of America Merrill Lynch survey, while two-thirds expect slower growth in the next 12 months.

This week, fresh warnings from Citigroup Inc., HSBC Holdings Plc and Morgan Stanley resonated as a growing pack of investors fretted the staying power of the party in balance-sheet risk.

According to Marty Fridson, one of Wall Street’s first high-yield bond analysts, the market hasn’t been so out of whack with economists’ forecasts of a U.S. recession since the financial crisis. Junk spreads indicate a 10 percent chance of recession versus 25 percent for a recession probability model. Premiums would have to widen about 250 basis points to bring them in line with the forecast, according to the chief investment officer at Lehmann Livian Fridson Advisors LLC.

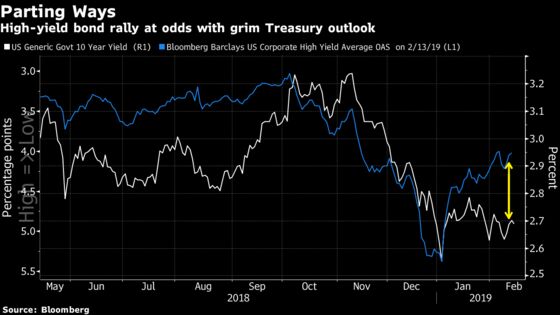

Yet credit bulls are rampaging like there’s no tomorrow, powering the best start to the year for U.S. junk since 2009. Traders have channeled a net $11.5 billion into exchange-traded products tracking corporate bonds this year, dwarfing inflows into the sovereign market. Premiums on U.S. speculative-grade debt have narrowed by over 130 basis points since early January, effectively erasing the December sell-off.

Great Divergence

Unlike in typical risk-on scenarios, where traders would skirt safe havens in government bonds as they pursue higher credit yields, demand for Treasuries remains intense.

It’s “the land of confusion,” Joseph Kalish, chief global macro strategist at Ned Davis Research Group, wrote in a note. While corporate bond prices suggest Goldilocks, Treasuries flash growth fears. One explanation for the “unusual behavior” could be that both corporate and government bonds are drawing support from muted inflation expectations, according to Kalish.

That sovereign-credit disconnect may be a signal for a correction in credit, particularly once the market awakens to the full force of quantitative tightening, Steven Major, global head of fixed income research at HSBC, argued in a report published this week.

On the QT

Even after signalling greater flexibility at the January meeting about its plan to remove stimulus, the Fed is still bidding to scale down its $4 trillion balance sheet.

Whether that will materially reduce liquidity, spur risk aversion and ramp up corporate borrowing costs are famously open questions for investors of all stripes. But they’re ones bullish money managers are choosing to ignore, warns Colin Purdie, CIO of credit at Aviva Investors.

“There’s still the big question of central-bank buying and the absence of the central banks in the bond market, and that does cause us some concern,” he said in an interview on Bloomberg TV.

Another way of thinking about it: Junk investors are betting there’s more liquidity coming, according to HSBC. “At best, there might be an end to the U.S. QT ahead of what may previously have been expected,” Major wrote. “At worst, the credit markets may have got it completely wrong.”

Over at Citigroup, renowned bear Matt King is growling -- the era of monetary distortion in risk markets is now receding, he said.

“As central banks back away, we come back to fundamentals,” according to the credit-products strategist. “What we are finding though is that fundamentals are not some nice fixed anchor. Everyone is actually downgrading their GDP forecasts, downgrading their earnings forecasts.”

--With assistance from Nejra Cehic, Yakob Peterseil and Sebastian Boyd.

To contact the reporters on this story: Cecile Gutscher in London at cgutscher@bloomberg.net;Ksenia Galouchko in London at kgalouchko1@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma

©2019 Bloomberg L.P.