‘Is Something Broken?’ Factor Quants Left Reeling By 2019 Strife

‘Is Something Broken?’ Factor Quants Left Reeling By 2019 Strife

(Bloomberg) -- Like many of his peers, Georg Elsaesser is trying to calm down his newbie quant clients as choppy stock moves make life difficult for anyone trading factors, which wire up systematic portfolios on Wall Street.

“Some of them are kind of scared,” said the Frankfurt-based fund manager at Invesco. “They’re asking the questions: Is something going wrong? Is something broken?”

For good reason. The rules-based method of dissecting stocks by traits like their apparent cheapness or how much they’ve gained recently is misfiring again this year.

While the broader equity market is basking in relative tranquility after notching some of their best gains in a decade, a slew of long-short styles are in the red. Market-neutral portfolios that typically follow these quant approaches have lost 1% this year, according to a Hedge Fund Research index.

Explaining why a factor portfolio did what it did is never easy, but a few generalizations are possible about 2019. Persistent caution over the growth outlook whipsawed riskier trades like value and small caps, shorts lost money, and among stocks that rose gains may have been too concentrated.

Elsaesser, who’s been crunching quant models for nearly two decades, likes to show worried clients a two-year chart of the MSCI World Index. Until recently, it’s been moving largely sideways with episodic swings that show factors are jumping around. His point is that there’s method in the seeming madness -- shifts in risk appetite are causing all this, and factors are acting as you might expect.

The investor is one of many in the systematic community trying to win back hearts with the pitch that factors are time-tested, designed for the long haul and backed by some of the smartest folk in finance and academia. But as the investing style closes a year to forget, patience is wearing thin among the market-neutral crowd. It’s spurring more managers to smarten up their strategies as billions of dollars flee the industry.

“The experienced investors say it’s normal noise in the long run,” Elsaesser said. “But it certainly means we need to explain more.”

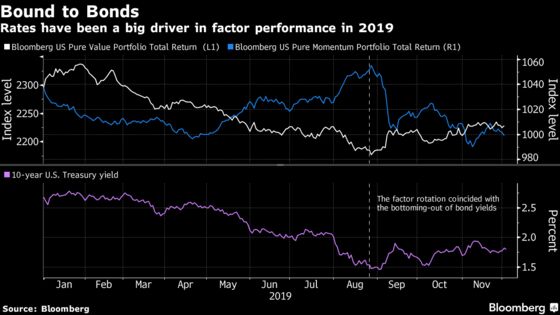

Days like Sep. 9 need explaining. The S&P 500 Index closed flat, equity volatility cruised around its five-year average and commodities were unexciting. Yet factor investors experienced the biggest rotation in a decade after value briefly broke out of its funk at the expense of high-flying momentum stocks.

Quants who failed to diversify into winners like low volatility are in soul-searching mode. Are factors like value structurally broken? Can market-neutral styles roar back to life over the long haul?

“Some of the themes we expected to diversify our returns in a period of underperformance of value haven’t worked as well,” said Ian Heslop, London-based head of global equities at Merian Global Investors.

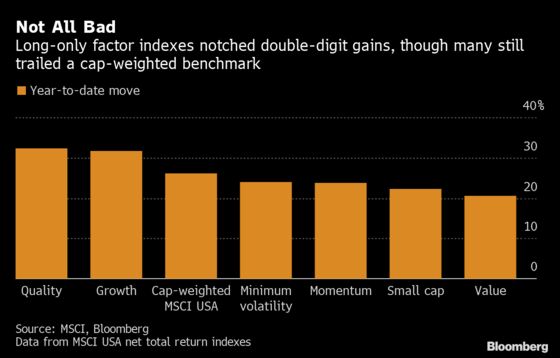

It’s not all gloom. A bunch of long-only factor strategies are posting 20%-plus gains this year. But they’re still lagging cap-weighted indexes. Sanford C. Bernstein estimates systematic long-only managers have lagged their benchmark by 2 percentage points on average.

Market-neutral quants with strategies including factor styles gained 1.2% this year as of Nov. 26 compared with 9.8% for equity long-short funds and 8.7% for discretionary macro funds, according to data on Credit Suisse Group AG’s prime-brokerage platform.

The short legs of factor strategies have been a drag on performance this year, reinforcing recent research by Robeco that argues the value of the investing style mostly comes from the long leg.

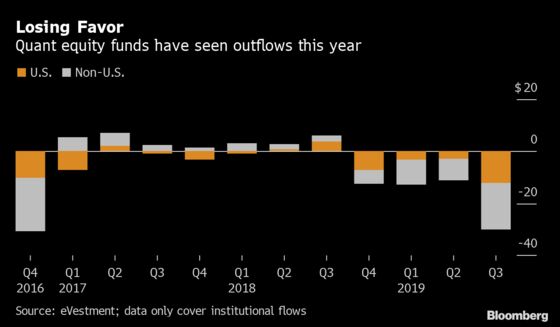

Outflows may have also hit industry performance. Market-neutral equity hedge funds lost nearly $4 billion over the period, according to Eurekahedge. Institutions even redeemed $54 billion from long-only quantitative stock funds in the first three quarters, eVestment data show.

“Whether this has been driven by flow events or not, it is finite, it’s very unusual,” said Heslop. His $4.5 billion Merian Global Equity Absolute Return Fund has seen its assets shrink by more than half this year.

Another culprit may live in the bond market. As interest rates dominated factor returns this year, diversification benefits weakened, strategists led by Joseph Mezrich at Nomura Instinet LLC posited. Factor correlations have risen, especially in Europe where they’re now the highest in a decade, according to Bernstein.

Fund managers steadfast in their conviction that value was poised for a rebound this year have been left disappointed. Since reviving briefly in September, the factor has flatlined since. Its outlook continues to divide quant land between bears citing low yields and weak growth, and bulls touting cheap relative valuations.

For Roberto Croce, the problem is the lack of diversification. Too many equity quants have been exposed to factors that are sensitive to risk appetite like value. The fund manager at BNY Mellon Investment Management touts defensive styles like low volatility which stems from behavioral anomalies. The strategy is booming as investors pay up for havens to hedge recession risk.

“It’s important to have a portfolio that is balanced across the underlying macro drivers of risk,” Croce said.

Perfect Storm

Some quants are duly revamping strategies. At Merian, Heslop’s team this year tweaked models to penalize exposure to highly correlated factors and to make allocations more defensive against downside risks. It’s now on the hunt for smarter definitions of value.

Naturally some funds are also deploying alternative data and machine learning in a bid to re-invent now widely known factor strategies.

Newfangled methods are a contentious move for a community that’s netted billions riding established factors back-tested over decades. Invesco’s Elsaesser for one is skeptical.

“It’s like a perfect storm for factors at the moment, but they have done what you would expect them to do,” he said. “We’ve seen these drawdowns; we’ve seen them recover. We know the essence of them is the very strong factor logic.”

To contact the reporter on this story: Justina Lee in London at jlee1489@bloomberg.net

To contact the editors responsible for this story: Sam Potter at spotter33@bloomberg.net, Sid Verma

©2019 Bloomberg L.P.