‘Follow the Fed’ Rally May Soon Fizzle Across Bond Markets

“There has been a slight misunderstanding between the markets and the Fed,” said Sameer Samana, senior global market strategist.

(Bloomberg) -- A breakneck rally across bond markets may slow as traders come to grips with the notion that the Federal Reserve’s support isn’t unconditional.

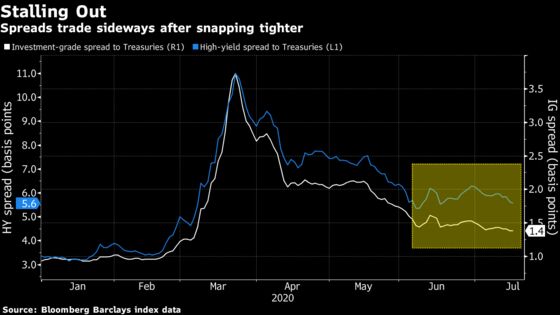

After a torrid rally sparked by the Fed’s announcement in March that it would begin buying corporate debt, investment-grade bonds have stalled near record levels. A similar pattern holds true for high-yield markets, where spreads are broadly trading sideways after the asset class’s best returns in a decade brought them close to pre-pandemic levels. And the central bank’s oft-repeated commitment to keeping interest rates low have locked benchmark Treasury yields into an unrelenting range close to historic lows.

The degree to which bond markets have rebounded after a trading freeze during March’s turmoil is largely the reason why they’re stalling out now. A parade of policy makers have hinted in recent weeks that the central bank won’t have to expand its balance sheet and buy bonds as aggressively as anticipated, with liquidity restored and primary markets buzzing. While bets the Fed isn’t going to be blindly buying bonds has capped gains for now, prospects that it might start again has cushioned any downside, according to Wells Fargo Investment Institute.

“There has been a slight misunderstanding between the markets and the Fed,” said Sameer Samana, Wells Fargo Investment’s senior global market strategist. “What the Fed has basically said is: ‘Our goal is to make sure we have orderly and liquid markets.’ The market has taken that to mean, ‘Okay, we’re going to buy like there’s no tomorrow.’ If the market’s able to trade efficiently, the Fed is starting to see their job as mission accomplished.”

After soaring 150 basis points in March, high-grade spreads tightened by 70 basis points in April and have dropped about 14 basis points so far in July through Friday. Junk-bond spreads have tightened 70 basis points this month, after a 380 basis-point surge amid March’s turmoil.

Weekly figures published Thursday showed that the Fed’s balance sheet edged higher over the past week -- after falling for roughly a month -- but remained below $7 trillion. It exploded by $3 trillion from early March to mid-June as the central bank pumped liquidity into the financial system to keep credit flowing via short-term loans and bond buying.

To be sure, there’s a reason ‘don’t fight the Fed’ is one of the most commonly deployed refrains in financial markets. The central bank has nearly unlimited firepower at its disposal to support the U.S. economy, the sheer magnitude of which was on display after the Fed slashed rates to near-zero and pumped trillions worth of liquidity into markets. Among the tools yet to be tapped are yield-curve control, an option that Federal Reserve Bank of New York President John Williams didn’t rule out in an interview Thursday.

Now, markets are largely back to normal and policy makers see the balance sheet’s decline as a healthy sign. But that’s after the Fed’s late-March pledge to buy corporate debt set of a wave of front-running flows, with credit ETFs and mutual funds absorbing record amounts of cash. As analysts downsize their forecasts for the central bank’s balance-sheet growth, investors are assessing whether that was overkill.

“People got a little bit carried away, were probably a little bit too positioned, and we forget that bonds often are kind of boring and we’re getting to that stage. If you want quick returns, it’s hard to see how you get them with some of these yields where they are,” said Peter Tchir, head of macro strategy at Academy Securities. “With investment grade and high-yield, you’re back to hoping you can clip a coupon rather than any big price appreciation.”

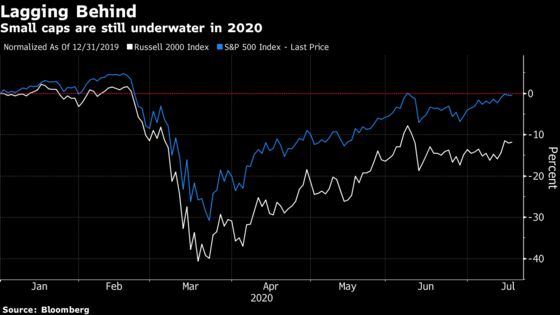

The slimming-down of the balance sheet also helps explain why the equity market -- outside of the megatech stocks -- have hit a wall as well, according to Samana. While the S&P 500 has rebounded about 45% since March’s low to erase this year’s losses, the bulk of those gains came before early June, and are largely thanks to tech heavyweights pushing the index higher. In contrast, the small-cap Russell 2000 Index is still 12% lower year-to-date.

“Equities haven’t really gone anywhere since early June, that dovetails nicely with the slowdown in the balance sheet,” Samana said. “It’s a very small sliver of the equity market that’s making all-time highs and its the part that not only benefits from what the Fed’s done, but also benefits from all the Covid-related things.”

©2020 Bloomberg L.P.