‘Extreme’ Market Stress Trashes Havens in a Crisis of Liquidity

‘Extreme’ Market Stress Trashes Havens in a Crisis of Liquidity

(Bloomberg) -- The central bank bazookas have been fired and governments are mobilizing their fiscal response, but for many investors their battle plans are all going wrong.

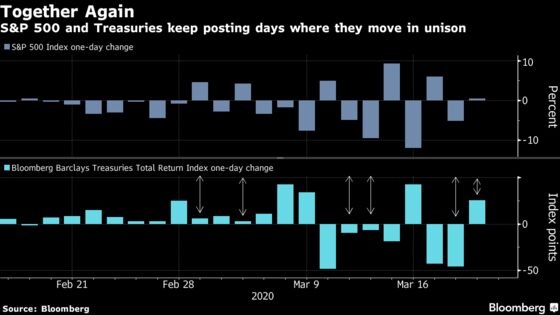

Major assets aren’t behaving as expected. In early trading on Friday, both U.S. equity futures and 10-year Treasuries were rising, a day after they both closed in the green and two days after they dropped together.

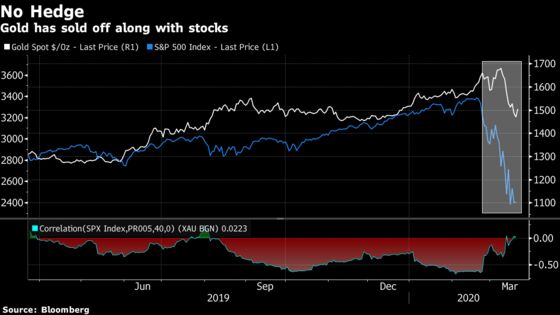

In a week when Wall Street’s fear gauge touched its highest ever, gold prices entered a correction and investors fled bond havens. In the market for exchange-traded funds, higher-quality corporate bond products are faring worse than their junk peers.

All these dislocations are whipsawing defensive investing strategies and creating headaches for those trying to figure out the market bottom.

“We’ve seen something like this in the financial crisis but not to the same extreme,” said Eugene Barbaneagra, a fund manager at SEI Investments Co. in London. “Defensive strategies on average over the last month or so did provide downside protection but on those extreme days their downside protection was disappointing.”

These market behaviors are not supposed to happen. Treasuries normally act as a hedge because they rise when stocks fall. High-grade credit is safer than high-yield. Gold is meant to be a safety play when things are rough.

There are two disconcerting aspects to the unusual moves. The first is what’s driving them -- investor fear rising so far and fast it drives them out of everything except cash. The second is the risk of them becoming self-reinforcing, where confidence in the usual havens crumbles, exacerbating the behavior.

Barbaneagra points to one worrying example. While minimum-volatility stocks outperformed, they did not provide as much refuge as investors might have expected as shares sold-off indiscriminately, he said. The MSCI index for the strategy dropped 24% over the past four weeks, compared with 29% for the overall market.

“The speed of the moves has just been quite insane even for long-term investors like us,” said Stephen Yiu, chief investment officer at Blue Whale Capital LLP, a long-only equities fund in London. Disarray like this means hedge funds are deleveraging or even closing down, which means they’re selling when no one is buying so prices fall even further, he said.

Wednesday’s trading action provided perhaps the most visceral demonstration. Stocks slumped again in high volatility, 10-year Treasuries suffered their biggest two-day yield surge since the 1980s, gold retreated and oil plunged 24% from already low levels.

The only winner, really, was the dollar, which hit the highest on record. And that only tightens international financial conditions. On Friday as a degree of calm returned to markets, the greenback was falling. Yet it remains 3.8% higher than a week ago.

“The risk is that the shortage of dollars has already begun to trigger negative feedback loops in a few countries,” Chester Ntonifor, a foreign-exchange strategist at BCA Research, wrote in a note on Thursday.

Central banks are doing their bit. The European Central Bank on Wednesday night announced a 750 billion euro ($805 billion) quantitative easing program to help the euro zone economy deal with the Covid-19 shock. The Federal Reserve has seemed determined to deliver at least one banner measure a day, the latest being new swap lines with a range of peers.

There are signs this has helped ease some of the pressure that was building in the short-term funding markets. The rate on overnight repurchase agreements on Thursday fell back to within the Fed’s target range for the effective fed funds rate.

But stress remains high, even as stocks attempt a second day of gains and volatility eases. The doubt is whether policy makers have enough ammunition to head off this brewing crisis. Or if fiscal and monetary efforts can fix the damage wrought by a human sickness. Christopher Wood at Jefferies LLC reckons not -- he says investors should be focused on the rate of coronavirus infections above all else.

Meanwhile in some of the disconnects there may be opportunities. Citadel is raising a new relative value hedge fund to capitalize on volatility in fixed income.

At SEI, Barbaneagra also remains overweight on battered value stocks as their discount to the market widened even further. Already on Thursday, a long-short value strategy posted its biggest gain in data going back to 2000 as outsize moves earlier reverse amid a hint of calm over markets.

“Those extremely attractive oversold names will become recognized by the market,” he said. “The old rule of being greedy when everyone is fearful -- it still works.”

©2020 Bloomberg L.P.