‘Buy the Dip’ Is Looking Risky But Wall Street's Doing It Anyway

‘Buy the Dip’ Is Looking Risky But Wall Street's Doing It Anyway

(Bloomberg) -- From near-certainty on interest-rate cuts to signs of a detente in the trade war, investors see the makings of a spirited upswing. And the recipe for its potential downfall.

It’s the latest chapter in 2019’s unloved rally.

For now, plenty of traders see good reason to be bullish as the U.S. tariff reprieve on Mexico boosts global stocks and sends emerging-market shares toward their biggest increase since January. And why not? Dip-buying and front-running monetary stimulus have proved reliable strategies to outperform post crisis.

But it’s also cornering investors into a new quandary. With fierce conviction in markets that a U.S. easing cycle is nigh, the bar for the next Federal Reserve-driven tantrum in risk assets is looking dangerously low.

Add event risks like the G-20 meeting this month and the ever-present threat of fresh White House missives on trade, and even the most bullish money managers are hedging their bets.

“With expectations for cuts already substantial, the risk seems more two-way,” said Robert Tipp, chief investment strategist at PGIM Fixed Income. “Markets could see their ultimate easing as good enough, but there is also a significant risk that they disappoint, driving a risk-off trade such as in December 2018 when the Fed’s behavior was seen as unduly hawkish.”

Expectations of monetary easing were fanned by Friday’s U.S. report that showed hiring and wage gains cooling in May and downward revisions to payrolls. Then came President Donald Trump’s move to call off punitive tariff plans on goods from Mexico, spurring Monday’s global equity rally.

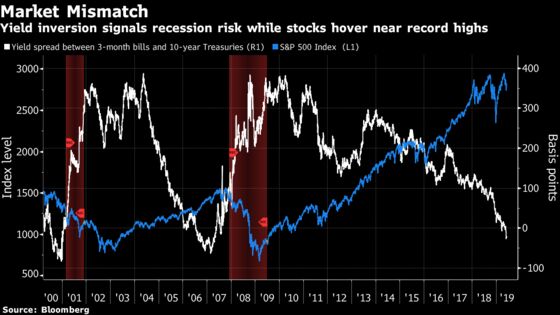

Futures signaled some 70 basis points of rate cuts in 2019 at one point last week. The potential hit to growth from tariffs to Group of Seven economies struggling to muster up inflation has put the fixed-income market on high alert, with key parts of the Treasury curve inverting and 10-year yields near multiyear lows.

“Let’s say the Fed cuts rates in June or July, is that enough if we get increased tariffs, is that enough to save the economy?,” said Constance Hunter, chief economist at KPMG LLP on Bloomberg TV. “I think there is a big question mark around that, I think there’s a strong possibility it’s not enough, and I think that is what is really freaking out the bond market.”

Checkered History

Preemptive cuts have a checkered history, strategists at JPMorgan Chase & Co. point out. Equities respond best when there’s already a strong underpinning to growth, like in 1995 and 1998. Overall, monetary easing has usually had a negative effect on corporate bonds, leading to wider spreads that persisted for an average six months after the first U.S. rate cut.

Only bonds and the dollar were clear winners: Treasuries continued to rally for as long as six months following a rate cut, according to JPMorgan strategists, while the greenback gained for as long as three months after.

Goldman Sachs strategists expect health care and consumer staples stocks would outperform on lower rates and tech to lag. Factors like momentum and low volatility should also be in favor, they wrote in a note Friday.

“This is going to be a grab for yield that is just going to continue, it may even become more intense,” Rick Rieder, BlackRock chief investment officer for global fixed income, told Bloomberg TV Friday. His firm likes call options to take advantage of an upswing in the S&P 500 and securities unloaded by forced sellers including high-yield bond ETFs.

Tweet Threat

Anastasia Amoroso, global investment strategist at JPMorgan Private Bank in New York, is treading carefully but sees no reason sit out the brewing risk rally.

“People just don’t know which way to turn because we don’t know what the next tweet is going to be,” she told Bloomberg TV. “It’s hard to make a call on this for the next 12 months but I think we can be positioning for a short-term upside here and a reversal in some of the sectors hit the hardest.”

Amoroso likes beaten-up emerging markets, credit and semiconductor stocks.

Thomas Thygesen, head of cross-asset strategy at SEB AB, warns the ebullient mood can quickly shift. If “it turns out in June they say in fact we’re not going to cut rates after all that will leave us with a negative shock still intact.”

Moreover, the underlying problems of weak growth can’t be solved with a quick-fix rate cut, he said.

“If the Fed deals with the trade war shock but they don’t do anything else that still leaves us with the same underlying story as beforehand,” said Thygesen. “And that story was global growth seems to be too weak to support expectations of an earnings rebound in the second half of the year which is what most estimates currently suggest.”

--With assistance from Jonathan Ferro, Alix Steel, David Westin, Justina Lee and Lu Wang.

To contact the reporter on this story: Cecile Gutscher in London at cgutscher@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma, Yakob Peterseil

©2019 Bloomberg L.P.