‘A Boxing Match All Day’: Notes From the Stock Trading Trenches

‘A Boxing Match All Day’: Notes From the Stock Trading Trenches

(Bloomberg) -- Day in, day out, clients call, the market takes another plunge, and Gary Bradshaw looks at his screens in Dallas and can’t figure out why.

“You feel like you leave here you’ve been in a boxing match all day,” said Bradshaw, a portfolio manager at Hodges Capital Management. “We’re kind of dumbfounded by the huge sell-off in the market versus what we’re hearing from companies. It looks to us like a fabulous buying opportunity.”

Pros hate quoting Dow points, but there’s no getting around their visceral pull. This is how many the industrial average has fallen at its lowest point on each of the last six days: 463, 679, 513, 77, 643 and 563. Three months ago, a 500-point drop was 1.8 percent. After a tumble to 22,445, now it’s 2.1 percent.

Waves of selling have lopped $5 trillion off equity values in three months despite nothing to suggest a recession is hence and forecasters saying the economy will grow more than 2 percent. For investment advisers, it’s made for a depressing holiday season.

“Everybody is not leaving the office early and going Christmas shopping or anything like that,” Bradshaw said. “We’re all busting our tails. We’re working harder, by a long measure.”

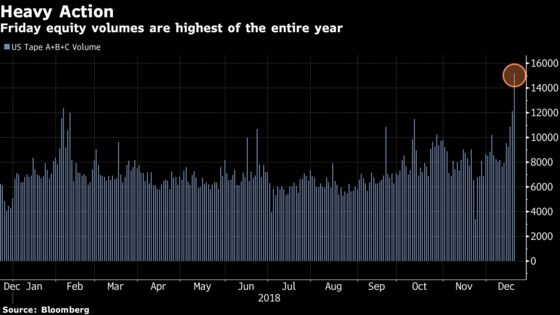

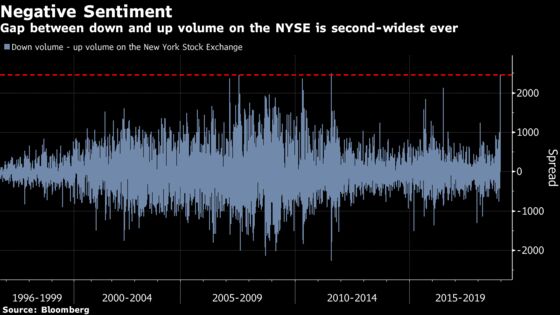

Everywhere you look, it’s a deluge of sells. On Friday, trading volume in New York Stock Exchange shares that were going down exceeded those that were rising by the second highest margin on record.

Up in Springfield, New Jersey, John Petrides, a portfolio manager at Point View Financial Services, is hearing from people worried about stocks they hoped would fund their old age. Petrides is buying -- he used the sell-off to add tech and bank stocks and cash in utilities.

“Most of the clients in retirement accounts are very nervous. The past sell-offs haven’t lasted more than a month, now you have three months of this going on,” he said. Part of it’s the Fed, part of it is the trade war. Part of it’s President Donald Trump, who seems to have lost his magic touch with markets.

Trump’s trade war with China has investors on edge and Bloomberg News reported late Friday that he has has discussed firing Fed Chairman Jerome Powell following this week’s interest-rate increase, citing people familiar with the matter.

“He had a lot of goodwill for the first two years of his presidency, because the stock market was going up. Between tariffs and uncertainty over growth there is a lot of concern as the stock market is going down,” Petrides said. “Is Trump a wild card? It’s resonated once again.”

For investors willing to take the plunge, stocks are a lot cheaper now, sinking to a 17-month low to cap their worst week since August 2011. Every sector fell as heavy selling in technology shares drove the Nasdaq into a bear market. The S&P 500 isn’t far behind, down 17.5 percent since September and sitting just 72 points above the 20 percent threshold that would end the longest rally ever recorded.

At just 16.4 times earnings in the past year and less than 15 times next year’s estimates, the S&P 500 is trading below levels that marked the end of the last protracted swoon, in February 2016. Prices like that brought out buyers then, but this month have done nothing to break the market’s fall.

“It seems to be more about sentiment and fear and unwinding of positions than it does about, call it, the fundamentals,” said Sameer Samana, senior global market strategist for Wells Fargo Investment Institute. “What you would expect is, all right, maybe equities also should go up maybe a little bit less than they did maybe in the first two-thirds of this year. Right now, this is being driven almost entirely by emotions.”

Some stats on how extreme things have gotten:

- This week’s trading volume was 54 percent above the average of any week before Christmas in the past 10 years.

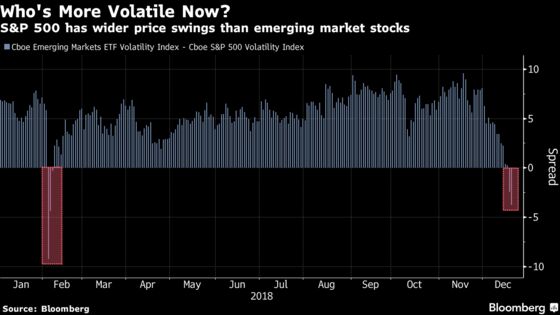

- Emerging markets had the best week relative to the S&P since 2011 as the VIX exceeded volatility in developing equities for the second day in a row and just the fifth day ever. Global stocks ex-U.S. had the best week relative to the S&P since 2009.

- 57 billion shares changed hands on the U.S. exchanges this week, the most since 2011.

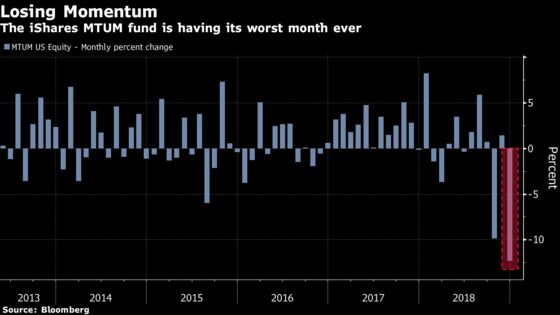

- Momentum ETF had the worst week ever, Nasdaq 100 plunged the most since 2008, small caps the most since 2011.

No single factor can explain the rout that’s put the S&P 500 on track for the worst year since 2008. How did we get here and what would it take for the market bleeding to stop? Analysts and portfolio managers weigh in.

Souring Fundamentals

Peter Mallouk, the co-chief investment officer of Creative Planning, a wealth-management firm with around $36 billion in assets:

“All that’s changed is the idea that in the future fundamentals may deteriorate, but today we still have the core fundamentals that were here a few months ago. Earnings and all those fundamentals are still here from before the market pullback. What’s changed here is the market trying to anticipate that these issues with rates and tariffs and political issues may accelerate us to a recession. It’s the market really guessing and the market guesses wrong over the short-run quite frequently. That’s what’s making this pullback a little different from most pullbacks. But we don’t have any new piece of informational that’s changed what’s going on today. We don’t have a significant new catalyst.”

Powell Put

Chad Morganlander, portfolio manager at Washington Crossing Advisors:

“Leading up to this, return expectations across the globe were quite low and momentum was high and investors were mispricing risk. And any indication of a slowdown would break the momentum trade. On the same front investors woke up to quantitative tightening and realized that for the last decade we’ve been surfing a wave of QE that seems to have turned. It remains to be seen when or if the Federal Reserve will truly blink and reverse course. For the next week or two, due in part by the meeting of the Fed that just happened, they’re willing to allow the markets to try to have price discovery or try to find price discovery in all this volatility. You’ll hit an air pocket in time before you should see some of these uncertainties resolve themselves.”

Growth Concern

Quincy Krosby, chief market strategist at Prudential Financial Inc.:

“What you’re seeing is an unwinding of the gains and consolidation as the market assesses how much growth we’re going to have next year. Going through 2,500 on the S&P 500 opens up a trap door if we don’t see any buyers coming in. What’s clear from all of this is that the Fed, and to use the president’s term, they needed to feel the market. Those who believe the Fed is making a serious mistake are saying the market is moving and telling you the economy can’t handle it. The fear is that when rates are rising this way and they do get two more next year, if they continue at $50 billion a month on the balance sheet, that they can break the economy.”

‘Not As Easy Anymore’

Frank Ingarra, the head trader at NorthCoast Asset Management LLC:

“The retail investors piled in January - there was this fear of missing out. ‘Oh my God, the markets are reaching new highs.’ They piled in, they felt good about their 401Ks. Now, their assets are much lower, and they’re freaking out. We try to stress that it’s not as easy anymore. We came off a couple of prior years where whatever you bought didn’t matter - the market would go up. Not anymore: volatility is involved, more uncertainty is involved with everything going on out there. Retail investors learned it the hard way as they piled in at the wrong time.”

To contact the reporters on this story: Sarah Ponczek in New York at sponczek2@bloomberg.net;Elena Popina in New York at epopina@bloomberg.net;Vildana Hajric in New York at vhajric1@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2018 Bloomberg L.P.