(Bloomberg Opinion) -- Two years ago, Albourne Partners Chairman Simon Ruddick described the fees hedge funds charge as the “elephant in the room.” Disappointing returns and a lack of transparency about levies meant investors were at risk of losing interest in the market, he warned.

So Albourne, which advises about 260 clients with more than $450 billion in alternative assets, suggested the funds ditch their traditional 2-and-20 fee structure, where asset managers charge 2 percent of the assets and keep 20 percent of gains collected.

Working with the Teacher Retirement System of Texas, Albourne proposed an alternatives deal: 1-or-30. A fund outperforming its benchmark would keep 30 percent of the returns. In a bad year, the firm would still collect a 1 percent management fee, but it would be deducted from the following year’s performance payment.

The idea caught on. Albourne, whose clients include the Utah Retirement Systems and the Wellcome Trust, reckons that about 60 hedge-fund managers globally had switched to the structure by the end of last year, up from about 16 in February 2017.

Performance-based fees are something to be welcomed by everyone. Tying fees more closely to returns is a great way of avoiding the “asset gatherer” problem, where managers seek to enrich themselves by increasing in size rather than focusing on performance.

I caught up with Jonathan Koerner, the partner at Albourne who devised the arrangement, by telephone from Norwalk, Connecticut. Following is a lightly edited transcript of our conversation.

MARK GILBERT: Hedge fund fees have been coming down for a while now, with Hedge Fund Research figures showing average management fees dropping to about 1.43 percent this year, while incentive fees are down to about 17 percent. Your proposal for a 1-or-30 structure has gathered pace, with more than 60 hedge funds adopting it by the end of last year. What’s the current tally?

JONATHAN KOERNER: There are 77 that I know about and are confirmed. There are certainly some out there that I don’t know about. We have clients that are actively pursuing 1-or-30 or x-or-y structures across their portfolio but have decided to keep the results private.

MG: In the event of a massive outperformance, it seems like the investor can lose out compared with traditional previous structures?

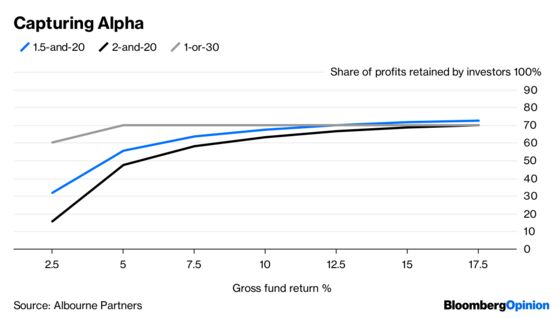

JK: This structure won’t always benefit investors, but it will benefit them when the manager underperforms. In a way, the 1-or-30 is an insurance policy. The premium is paying extra fees when the manager truly outperforms. But that is the only condition under which the investor pays more. The protection the investor buys is avoiding the risk of overpaying for underperformance.

It allows for the fee conversation to evolve from fee cuts and discounts to an improved shape of fees. Every time there’s a period of underperformance in the hedge fund industry, there is downward pressure on fees. When managers truly start to outperform again, and provide the returns investors expect, managers realize that they lowered their fees. They’ll say “I’ve got to close that class and go back to 2-and-20.” There’s a lag on that, and it’s not efficiently priced, whereas the 1-or-30 can survive those cycles and preempt the need for renegotiation.

MG: It’s less environment-dependent?

JK: It’s more that it adjusts in real time to the environment.

One common criticism is the initial reaction to the numbers. The reaction to one percent by managers is “Oh, I’m gonna dismiss that right away. I can’t operate on one, that’s ridiculous. I’m an emerging manager with only $300 million, my break-even is 1.5 percent.” Or, it’s a manager with a very labor-intensive strategy, maybe a bankruptcy or distressed credit specialist that employs 40 attorneys. They dismiss it immediately because of the one. If we didn’t care about the manager’s need for capital and current revenue, this would have been zero-or-30 from the beginning.

MG: Because the fund manager has to be able to afford to keep the lights on and build a business?

JK: It does nobody any favors to strain the manager’s business and inhibit them from being able to generate the returns you expect. They need revenue to retain employees, they need revenue to invest in their business, for technology and various things. It will not be one for most managers. But it should be whatever is sufficient for any given manager.

Going to the y side of the equation, with 2-and-20 or 1.43-and-17, you don’t know what the economic split between the investor and the manager will be at the end of any given year, until the performance is known. And you won’t know what the economic split will be over a multi-year period until you see what path the returns of that fund took. With the “or” structure, you know what it will be.

Some investors react to the 30 with a kind of a sticker shock. I think there’s a lack of understanding. The 30 represents total fees, not performance fees. It will always be reduced by the management fees paid. The effect of that is for the total fees to mirror what would have been paid at zero-and-30 — but guaranteeing the managers revenue to operate their strategy.

MG: What happens if a fund can’t beat its benchmark for three or five years? As an investor, you’ve paid your management fee in advance, and it was going to be reimbursed from future outperformance — but what if there is no outperformance?

JK: If a manager can’t outperform the free beta alternative over a multi-year period, then what are they worth? They will have received a management fee, but has that manager provided any value that is worth a performance fee? I would suggest not. I would suggest too many managers do just that. They charge investors — including pensions providing retirement benefits funded by taxpayer dollars for teachers, firefighters, policeman — and that money is diverted to a manager that’s provided no benefit. The invisible hand is better applied through a fee structure that rewards skill.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2018 Bloomberg L.P.