$19 Billion of Stock for Sale and Other Theories on the Selloff

Selling by asset allocators may be contributing to weakness.

(Bloomberg) -- From technical selling to technical levels on charts, investors were groping for answers amid the worst equity selloff since early April. Here’s a sampling of responses that were circulating in the market at midday.

Fund Rebalancing

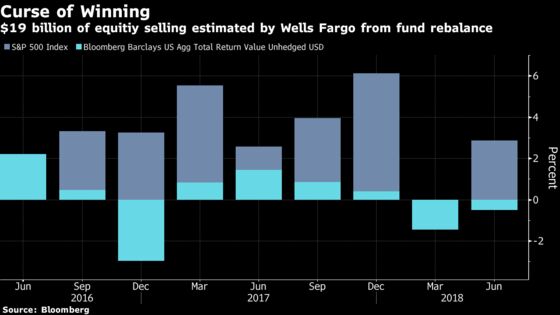

One theory on the weakness is that it reflects end-of-quarter adjustments by institutional investors with large holdings in both stocks and bonds. According to this, big asset allocators use the period to balance out holdings, dumping winners and adding to losers. At the moment, that’s bad for equities.

“One might be surprised to realize that thus far domestic stocks have bested bonds by a wide margin in Q2,” wrote Boris Rjavinski, a strategist at Wells Fargo, in a note. “Consequently, our model is calling for sizable quarter-end asset-allocation rebalancing flows among U.S. defined benefit pensions. The way things stand at the moment, pension bond portfolios may need to pare back $19 billion in equities and add $14 billion in bonds.”

Technical Levels

It’s easy to assign significance to random lines on charts. But Monday’s retreat ticked a lot of boxes for technical analysts. In addition to pushing the S&P 500 beneath its 50-day moving average and the Dow Jones Industrial Average below its 200-day mark, some analysts saw a portent in peaks past. Namely, the failure of the S&P 500 to climb over its highest points of its February and March recovery.

“We’ve seen this before,” said Frank Cappelleri, senior equity trader at Instinet LLC. “The high flyers (tech, included) pulled back after making new highs in March. Back then, those highs were soon lost, and a lot more weakness resulted. Those areas must prove they can do a better job this time around.”

Fed Reaction

Donald Trump’s war of words with China has been going on for months and while Monday arrived with its usual ration of rhetoric, U.S. stocks have stood up to worse. What might be different this time are memories of warnings in last week’s Federal Reserve statement, in which Chairman Jay Powell said changes in trade policy may affect the outlook for the economy.

“A lot of people had been hoping that the optimism over the tax cuts could offset the trade-war angst,” said Matt Maley, an equity strategist at Miller, Tabak & Co. “The markets are now wondering if this is going to happen. They are processing last week’s comments from the Fed’s Jay Powell that trade tensions are creating enough uncertainty that it’s starting to create an impact on business managers.”

Too Much at Once

While the market may have gotten used to trade bluster, that doesn’t mean it’s immune to it. With the Fed raising rates, the margin of safety for investors shrinks.

“The ‘unforced error’ of a trade war along with EM stress would likely lead to a deceleration in global growth that would slow the pace of Fed rate hikes, but for the wrong reasons,” Dennis DeBusschere, head of portfolio strategy at Evercore ISI. “In that scenario, earnings estimates would come under pressure, cyclicals would continue to lag and money would move from stocks to bonds or cash (happening today). As of late last week, investors remain evenly split on trade tensions putting the odds of a U.S./China trade war at 54%. Increased odds of a negative outcome on trade would strengthen the outperformance of Defensives and encourage a rotation out of stocks and into bonds/cash.”

Other Voices

John Stoltzfus, chief investment strategist at Oppenheimer: “Looks to us like most of the declines today are tied to tariff concerns. What had been a collective thought in the market that the trade skirmish would remain bluster and rhetoric has become a thought that a trade skirmish could ensue and stick for some yet unknown period of time.”

Barry Bannister, chief equity strategist at Stifel Nicolaus: “The S&P 500 began to roll over in mid-June when it was just over one multiple point over-valued. Although EPS should fully offset P/E compression this year, investors had to look to full-year earnings to justify a price close to 2,800.”

To contact the reporters on this story: Lu Wang in New York at lwang8@bloomberg.net;Elena Popina in New York at epopina@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2018 Bloomberg L.P.