We Never Learned From Lehman

(The Bloomberg View) -- Bloomberg Opinion marks the 10th anniversary of Lehman’s bankruptcy with a collection of columns from around the world. Read more.

Ten years ago, amid a worsening subprime mortgage crisis, the U.S. government did what few have dared: It allowed a major global investment bank, Lehman Brothers Holdings Inc., to file for bankruptcy. Within days, the shock waves crippled the nation’s largest insurer, triggered a run on money-market funds, and accelerated a cash crunch that would ultimately destroy millions of jobs. Only by pledging trillions of dollars to prop up the financial system, and spending hundreds of billions more on fiscal stimulus, did the government manage to prevent the worst economic disaster since the Great Depression from becoming the worst ever.

The repercussions of that debacle endure today. In the U.S. alone, an estimated $1.4 trillion in annual economic output will never be recovered — a loss that has weighed most heavily on the poor. The cost of shoring up economies has left advanced-nation governments deeper in debt than at any point since the Second World War, and depleted the financial resources central banks will need to fight the next recession. The populism that has gripped the developed world, and that brought Donald Trump to power, can be traced to the way the crisis — and the spectacle of governments left with no choice but to bail out those responsible — undermined confidence in the establishment.

Given the scale of the damage, the experience should be seared into the memories of politicians everywhere. It’s shocking to see how quickly they’ve forgotten, and how fragile the financial system remains.

The lessons of the 2008 crisis are clear. Banks had too much debt and too little equity, so they couldn’t bear the losses they faced. Government overseers were flying blind: The system was so opaque that they couldn’t see risks building or know who was connected to whom. And even if they had perfect visibility, they couldn’t safely dismantle a large, global financial institution. The Lehman failure demonstrated their awful options: Bail out banks at taxpayer expense, or tempt Armageddon.

After the crisis, legislators and regulators worked to ensure that the system would be better prepared, adopting thousands of pages of laws and rules. In some cases, the changes are unnecessarily burdensome. In general, they have fallen short. Regular stress tests have improved banks’ risk management, but aren’t nearly as stressful as a real crisis. New derivatives rules and risk reporting have shed more light on the financial system, but don’t yet provide the real-time, cross-border picture needed to see dangers and respond accordingly. Some of the world’s largest banks still can’t provide timely, complete and accurate data on their own exposures. Regulators have developed a mechanism that allows them to take over a large, distressed financial institution, but it’s untested and unlikely to work in a system-wide crisis.

All told, the global financial system looks troublingly like it did in 2007. Vast risks are still concentrated in a handful of vulnerable institutions. There’s no shortage of proposals for a more fundamental fix, but political will is lacking. Worse, the world is backsliding.

In Europe, banks have successfully fought back against rules that would have toughened regulatory capital ratios. In the U.S., Congress and the Trump administration have rolled back bits of the 2010 Dodd-Frank financial reform, weakening some safeguards and undermining institutions designed to protect consumers and create a financial early-warning system.

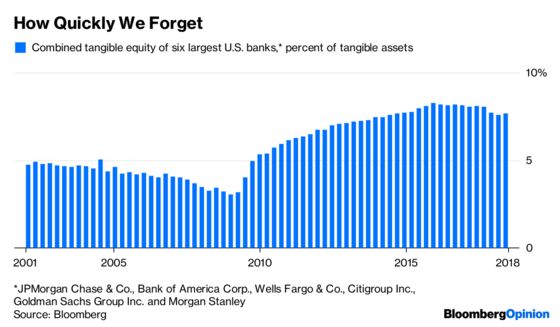

The level of equity capital at the world’s largest banks is probably the single best indicator of where things stand. Contrary to popular belief, it’s not some kind of rainy-day reserve. It’s money that shareholders have committed to the enterprise — money that banks can use for loans and investments. Unlike debt, it has the advantage of absorbing losses automatically, a feature that makes the whole system stronger. Regulators concerned about financial stability typically want more of it. Executives, by contrast, prefer to use less equity and more debt — that is, more leverage — because in good times this boosts widely followed measures of profitability.

Back in the early 1900s, before deposit insurance and other taxpayer backstops, banks typically had about $20 in equity for each $100 in assets — a capital ratio of 20 percent. Today, the weighted average tangible common equity ratio at the six largest U.S. banks is 7.7 percent. That’s more than twice what they had on the eve of the crisis in 2007, but down from 8.3 percent in December 2015, when the post-crisis drive for financial reform started to wane. Here’s how that looks:

By any reasonable measure, this isn’t enough. In the darkest days of the last crisis, forecasts of total losses on U.S. loans and securities reached 10 percent. To present little risk of needing to be bailed out, banks should have maybe twice that amount in equity. That’s roughly what economists at the Federal Reserve Bank of Minneapolis concluded last year. They estimated that under current capital requirements, the chance of a bailout being required in the next 100 years is two in three.

Sooner or later, another crisis will come. Investments deemed safe will prove not to be, and the system’s resilience will be tested again. Adequate capital is the essential foundation of a robust system. There’s no good reason banks can’t comply — and no better time than now. In the U.S., profits are nearing records set in 2007, making it easier to add to equity.

The legacy of the crash should be a safe financial system. It isn’t too late to bring that about.

Editorials are written by the Bloomberg View editorial board.

©2018 Bloomberg L.P.