Yield Mania Gives Needed Break to Indebted Emerging Markets

Yield Mania Gives Breathing Space to Indebted Emerging Markets

(Bloomberg) -- Emerging-market countries have relied this year on short-term local-currency debt as the pandemic drove investors to the notes for safety. Now, turbo-charged by Joe Biden’s election and signs of a vaccine breakthrough, bonds with longer maturities are attracting buyers again.

U.S. elections have revived the yield hunt, granting much-needed breathing space to governments in developing economies. They face the equivalent of about $3 trillion in local debt maturing next year after a borrowing binge in short-term bonds that were mostly bought by local banks in the absence of international investors.

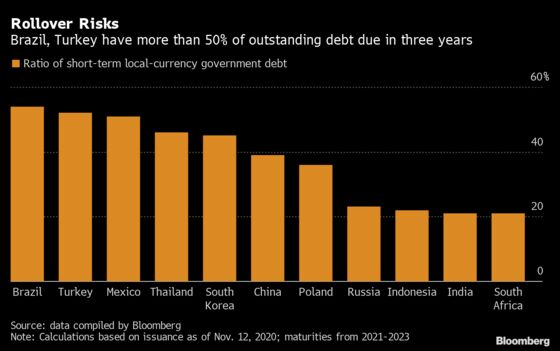

Investor appetite for longer securities would ease the fiscal pain of emerging markets as they pump funds into fighting another wave of infections. Brazil, Turkey and Mexico, which need to redeem more than 50% of their outstanding debt in the next three years, face the biggest debt-refinancing challenge. Higher-rated Asian borrowers may be able to roll debt over more easily, data compiled by Bloomberg show.

“The recent emerging-market currency rally has triggered inflows back into EM local markets and this should increase interest for duration bonds,” said Christian Wietoska, a strategist at Deutsche Bank AG in London. “Investors want high yields and at the moment, curves are still very steep, which makes investments extremely attractive for foreigners in the long-end.”

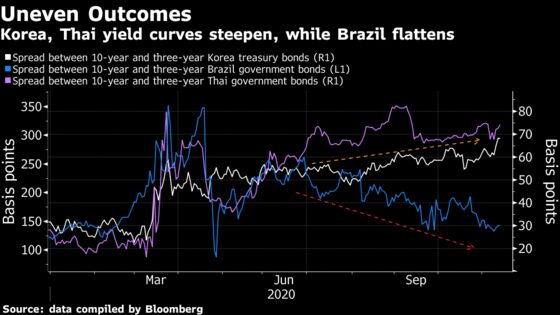

The demand for short-term bonds has resulted in steeper bond yield curves for the highly rated debt of South Korea and Thailand after rate cuts by their central banks. In junk-rated Brazil, the curve has flattened as short-term rates rose faster than the long-end amid a stimulus-spending splurge. The average maturity of local government bonds sold at auction was 2.36 years in August, down from 4.95 years a year earlier in the South American nation.

“Rollover risks would be more of a concern for lower-rated countries like Brazil and Turkey,” said Duncan Tan, a strategist in Singapore at DBS Group Holdings Ltd. “For higher-rated countries with low reliance on external funding, such as South Korea and Thailand, I don’t foresee any difficulties ahead, in terms of rolling over a larger quantum of short-term debt.”

Increasingly, investors appear to favor longer-term, local-currency government bonds on speculation a Biden White House with a split Congress means less fiscal stimulus, lower rates for longer and an extended period of dollar weakness that benefits emerging markets with lower debt-servicing costs.

Those with maturities of one year or less handed investors a loss of 1.4% in dollar terms in the past month, while those due in at least five years have gained about 2%, according to a Bloomberg Barclays index. Local-currency bonds have gained more than 4% in the year so far, nearing the returns seen for dollar-denominated debt in the same period, the indexes show.

“Next year, we may see some terming-out or at least more duration, perhaps in anticipation of a gradual rise in G7 rates,” said Nick Eisinger, co-head of emerging markets active fixed income at Vanguard Asset Management in London. “They need to do duration because otherwise they would end up issuing too much short-term debt and that could produce some rollover problems.”

©2020 Bloomberg L.P.